The claim gets denied.

This scenario plays out across the trades constantly. Standard GL insurance is built to cover third-party liability — accidental bodily injury or property damage caused to others. It was never designed to cover the cost of fixing or redoing the contractor's own work. Most contractors don't learn that distinction until a claim is already on the table.

This post breaks down the most important warranty-related exclusions found in contractor GL policies, explains what they mean in plain language, and outlines what contractors can do to close these gaps.

TL;DR — Key Takeaways

- GL insurance is not a warranty — it covers third-party liability, not your own workmanship obligations

- The "your work" exclusion is standard in most contractor GL policies and eliminates coverage for completed work

- The CG 2294 endorsement removes the subcontractor exception, closing a critical coverage gap GCs often assume exists

- Classification limitations and prior work exclusions create additional blind spots most contractors don't anticipate

- Purpose-built warranty programs are the right structure for backing workmanship commitments — GL policies are not

Why Contractor Insurance Doesn't Cover Warranty Claims

The Policy Was Never Designed for This

ISO CG 00 01, the standard commercial general liability form, applies Coverage A only to bodily injury or property damage caused by an occurrence — defined as an accident, including continuous or repeated exposure to substantially the same harmful conditions. IRMI confirms that if faulty work doesn't meet the threshold of an "occurrence," the CGL won't respond at all.

The practical implication: GL is designed to respond when a contractor accidentally harms someone else — not to reimburse the cost of correcting the contractor's own work.

Here's where the line falls:

- An HVAC contractor installs a system. Refrigerant leaks and damages the homeowner's ceiling — the ceiling damage may be covered under GL

- The cost to replace or redo the faulty installation itself — not covered

The contractor absorbs that second cost entirely.

Why Insurers Draw This Line

IRMI's defective construction guidance states directly that a CGL policy is not intended to pay for "warranty work." Including workmanship guarantee coverage would transform a liability product into a performance bond — a different risk type that requires different underwriting and pricing entirely.

The gap catches contractors off guard because carrying insurance feels like being protected. But the policy has a specific, narrow purpose. Manufacturers like Carrier, Trane, or Lennox cover the parts — but the moment a technician puts hands on that system, the labor cost is on the contractor. No one covers that except the contractor's own pocket.

That exposure is what warranty exclusions in the policy language are formalizing. How those exclusions are written varies — based on the insurer, whether the policy sits in the admitted or E&S market, and which endorsements are attached.

The Most Common Warranty-Related Exclusions in Contractor GL Policies

Contractor GL policies — particularly those placed in the E&S (excess and surplus) market, which reported $81 billion in stamping-office premium for 2024, up 12.1% over 2023 — often carry a range of endorsements that narrow coverage significantly. Knowing these by name puts contractors in a better position when reviewing their policies.

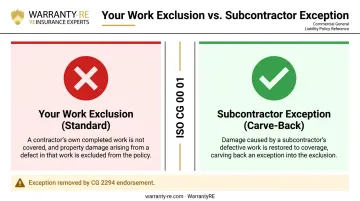

The "Your Work" Exclusion

Exclusion l in ISO CG 00 01 eliminates coverage for property damage to "your work" arising out of it and included in the products-completed operations hazard. In plain terms: once a project is complete and a defect surfaces, the cost to fix that work isn't covered.

The standard ISO form does include one important carve-back — the subcontractor exception. If the damaged work, or the work that caused the damage, was performed by a subcontractor on the insured's behalf, coverage is restored. ISO added this exception in 1986 to account for general contractors whose projects involve multiple subcontractors.

That exception matters enormously — and it's frequently eliminated by endorsement.

The CG 2294 Endorsement

ISO CG 22 94 is titled "Exclusion – Damage To Work Performed By Subcontractors On Your Behalf." It removes the subcontractor carve-back from the "your work" exclusion entirely.

For a general contractor or home service contractor who relies on subcontractors for overflow work, specialty tasks, or seasonal demand, this endorsement can wipe out completed operations coverage for property damage caused by subcontractor work.

The practical consequence:

- A subcontractor performs roofing work that leads to water intrusion discovered six months after project completion

- The GC's policy has CG 2294 attached

- The claim is denied — there is no coverage for the subcontractor's completed work

Insurance Journal noted as early as 2009 that CG 22 94 appears in contractor GL policies, particularly in the E&S marketplace, and can be especially damaging for GCs who depend on subs.

CG 2139 — Contractual Liability Limitation

ISO CG 21 39 replaces the standard definition of "insured contract" with a much narrower list. Gone is the broad category covering tort liability assumed under many business contracts. What remains is limited to:

- Sidetrack agreements

- Elevator maintenance contracts

- Certain easements or license agreements

- Leases of premises

Many contractors rely on their GL policy to back up indemnification provisions in construction contracts or subcontract agreements. CG 2139 removes that support — a contractor who has agreed to indemnify a client or GC may find their policy won't respond when that obligation is triggered. This endorsement is common in E&S markets and often appears under varying names, making careful policy review essential.

Classification and Prior Work Exclusions

Two additional exclusions create less visible but equally real gaps:

Classification limitation endorsements restrict GL coverage to only the operations specifically described and rated on the policy declarations. IRMI defines this as a nonstandard exclusion that eliminates coverage for business operations without a listed class code. An HVAC contractor who also performs some plumbing or electrical work — but whose policy only lists HVAC as a rated operation — may find those other activities unprotected.

Prior work exclusions eliminate coverage for occurrences arising from work completed before the policy's inception date. Insurance Journal explains that these provisions target past exposures, which becomes critical when a contractor switches carriers or lets coverage lapse — and a completed-operations claim surfaces later.

How Subcontractor Warranty Endorsements Create Additional Gaps

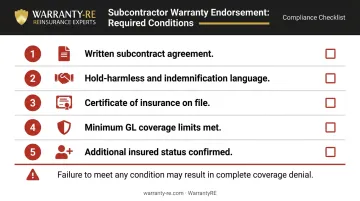

Beyond CG 2294, many contractor GL policies include subcontractor warranty endorsements — also called independent contractor limitation endorsements. These don't just exclude coverage outright; they condition coverage on the contractor having met specific requirements with every subcontractor used.

Common requirements include:

- Written subcontract agreements in place before work begins

- Hold-harmless and indemnification language within the contract

- Certificates of insurance on file

- Minimum coverage limits for the subcontractor's own GL policy

- Additional insured status on the subcontractor's policy

Failure to satisfy any one of these conditions can result in a complete coverage denial for that subcontractor's work.

The Hammer Clause Problem

Some endorsements go further with what's known as a hammer clause: a provision that nullifies all coverage related to the subcontractor's work if the required conditions aren't met. No partial coverage, no reduced limits — just a flat denial.

Other endorsements apply higher deductibles or reduced limits instead, but the hammer clause is the most punitive structure. It should be identified and negotiated when your policy is being placed or renewed.

The Reality for Home Service Contractors

HVAC, roofing, and plumbing contractors regularly bring in subcontractors for overflow work, specialty tasks, or peak season demand. Many of those arrangements are informal — and missing the exact documentation the endorsement requires:

- No written subcontract agreement

- No certificate of insurance on file

- No additional insured endorsement

That's the exact circumstance where subcontractor warranty endorsements eliminate coverage precisely when it's most needed. The endorsement makes no allowance for arrangements that seemed routine — it only checks whether the paperwork was in place.

What These Exclusions Mean for Home Service Contractors

Large commercial GCs often have dedicated risk management staff whose job includes reviewing policy endorsements at every renewal. Most HVAC, roofing, plumbing, and electrical contractors do not. A policy certificate gets filed, renewals get processed, and the endorsements attached to the policy never get a second look.

The compounding risk is real:

- A contractor who offers verbal workmanship guarantees to win jobs has created an obligation their GL policy almost certainly won't fulfill

- A contractor using subcontractors without written agreements may have no completed-operations coverage at all under CG 2294

- A contractor who switched carriers without checking prior work exclusions may have a gap in coverage for anything installed before the new policy took effect

When an uncovered warranty claim lands, the costs fall entirely on the business: equipment reinstallation, material replacement, labor, and potentially legal defense if a customer escalates the dispute. For home service contractors operating on tight margins, a single significant uncovered claim can do lasting financial damage.

The WarrantyRE team sees this pattern consistently: contractors absorbing callback costs on refrigerant leaks, flashing failures, bad plumbing joints, and loose electrical connections entirely on their own — costs that add up faster than most owners realize until a bad quarter forces a hard look at the books.

How to Address Warranty Coverage Gaps

Start With Your Existing Policy

Before assuming coverage exists, request a full copy of the policy — not just the certificate of insurance. Look specifically for:

- CG 2294 — Is the subcontractor exception to the "your work" exclusion removed?

- CG 2139 — Is contractual liability coverage narrowed?

- Subcontractor warranty endorsements — What conditions must be met for subcontractor work to be covered?

- Classification limitations — Are all your trade activities listed and rated?

- Prior work exclusions — Is there a gap tied to when your current policy started?

If any of these are present and unclear, ask your broker directly: what is and is not covered for completed operations and subcontractor work? Get the answer in writing.

Build a Separate Foundation for Warranty Obligations

GL insurance was never designed to function as a warranty. Contractors who want to make genuine workmanship commitments — and stand behind them financially — need a purpose-built structure that's separate from their liability coverage.

This is where contractor-owned warranty reinsurance programs like those structured through WarrantyRE offer a purpose-built alternative. Rather than paying a third-party warranty company that retains all the underwriting profit, contractors can establish their own reinsurance structure that:

- Funds warranty obligations from customer-paid fees built into job pricing

- Covers labor warranty callbacks — refrigerant leaks, roofing failures, plumbing callbacks, electrical rework — from a dedicated pool rather than from operating cash

- Retains unused warranty funds with the contractor, not a third party

- Is backed by A-rated insurers through an admin obligor structure, limiting the contractor's liability to formation costs plus accumulated earnings

WarrantyRE handles full claims administration, legal filings, tax returns, performance reporting, and compliance, so contractors stay focused on installations and service calls rather than program administration.

The Mindset Shift That Matters

Understanding warranty exclusions isn't only about finding holes in an insurance policy. A warranty is a business commitment, and business commitments need a financial foundation built specifically for them.

Contractors who build that foundation stop eating warranty costs out of operating cash — and start treating workmanship guarantees as a structured, fundable part of their business model.

Frequently Asked Questions

Does general liability insurance cover warranty claims for contractors?

Standard GL insurance does not cover warranty claims. It covers third-party bodily injury and property damage caused by an occurrence — not the cost of repairing or redoing the contractor's own completed work. This limitation is structural and reinforced by specific policy exclusions, including the "your work" exclusion in ISO CG 00 01.

What is a contractor limitation exclusion?

A contractor limitation exclusion — often called a classification limitation endorsement — restricts GL coverage to only the operations listed and rated on the policy declarations. Any work performed outside those categories carries no liability coverage, a significant exposure for multi-trade home service contractors.

What are the common exclusions in an E&O policy?

E&O policies for contractors typically exclude intentional acts, bodily injury and property damage (covered by GL), work performed outside the defined scope of services, and claims arising from prior known circumstances or undisclosed incidents at the time of policy application.

What is a CG 2294 endorsement?

CG 2294 is an ISO endorsement that removes the subcontractor exception to the "your work" exclusion in a CGL policy. Without that exception, property damage caused by a subcontractor's completed work is no longer covered — a significant gap for any contractor who relies on subs for part of their labor.

How can HVAC and home service contractors protect themselves from warranty-related coverage gaps?

Review every endorsement on your GL policy — not just the declarations page — and document subcontractor agreements before work begins. For workmanship commitments to customers, WarrantyRE structures contractor-owned reinsurance programs to fund and manage those obligations outside of standard liability coverage.