Introduction

Picture this: your crew finishes a commercial panel upgrade on a Friday afternoon. Monday morning, you get a call — a connection failed, sparked a fire, and the building owner is filing a $400,000 property damage claim. Or worse, one of your guys takes a bad fall from a ladder and is now threatening to sue.

Without the right insurance in place, that scenario becomes a business-ending event.

Texas electrical contractors face a layered set of requirements that most other states don't have: a unique workers' compensation opt-out rule, a state licensing body with documented insurance minimums, and major cities that each run their own registration and permit systems.

Knowing which coverage applies where isn't optional. It determines whether you can pull permits, win commercial bids, or survive a single large claim.

This guide covers:

- How Texas licensing ties to insurance requirements

- The specific coverage types electrical contractors need

- Texas's workers' comp opt-out rules and what they mean for you

- Coverage limits and certificate requirements

- What drives your premiums

- How contractors are structuring protection beyond standard policies

TL;DR

- TDLR requires documented general liability insurance ($300K per occurrence / $600K aggregate) to obtain and renew your electrical contractor license

- Workers' comp is optional for private employers in Texas — but mandatory for government and public school contracts, and opting out removes key legal protections

- Commercial clients expect higher limits ($1M/$2M) than what TDLR requires, plus endorsements like additional insured status and waiver of subrogation

- Major Texas cities (Dallas, San Antonio, Austin, Houston) each have their own contractor registration tied to permit access

- A warranty reinsurance structure lets electrical contractors capture underwriting profits from labor warranties instead of paying them to third-party providers

How Texas Licensing and Insurance Requirements Are Connected

The Texas Department of Licensing and Regulation (TDLR) is the state authority for electrical contractor licensing. Before your business can legally perform electrical contracting work in Texas, TDLR requires a business-level Electrical Contractor License — and that license requires documented proof of general liability insurance.

Individual Licenses vs. Business Licenses

Texas separates individual electrician credentials from the business license. Apprentice, journeyman, and master electrician licenses are individual credentials. The Electrical Contractor License is held by the business entity — and insurance requirements attach to that business license, not to the individual.

One key connection: the business applicant must employ a licensed master electrician or be one. But even if the owner holds a master license personally, the insurance obligation falls on the contractor business.

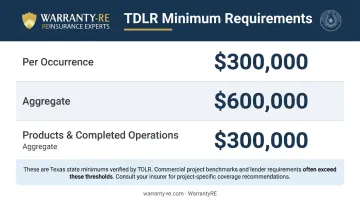

What TDLR Actually Requires

According to the TDLR Electrical Contractor Certificate of Insurance, the verified minimum general liability requirements are:

| Coverage | Minimum Required |

|---|---|

| Per Occurrence | $300,000 |

| Aggregate | $600,000 |

| Products & Completed Operations | $300,000 aggregate |

A Certificate of Insurance (COI) demonstrating these limits is required at both initial application and renewal. TDLR's official electrical contractor documentation does not list a statewide surety bond requirement.

Beyond TDLR, general contractors, commercial clients, and municipalities will independently verify your coverage before awarding work. The state minimum gets you licensed, but it won't necessarily get you on the bid list.

Essential Insurance Types for Texas Electrical Contractors

General Liability Insurance

General liability is the foundation of your coverage. It protects against third-party bodily injury and property damage claims — the kind that arise from active operations, completed work, and jobsite accidents.

Common scenarios GL covers for electrical contractors:

- A client trips over your equipment and breaks an arm

- A wiring error causes a fire after the job is complete

- Your crew damages adjacent property during installation

As noted above, TDLR sets $300K/$600K as the licensing floor. But Insureon and Simply Business data show that the market benchmark for electricians is $1M per occurrence / $2M aggregate — and that's what most general contractors and commercial clients require by contract.

Workers' Compensation Insurance

Texas is the only state where private employers can choose whether to carry workers' compensation coverage. For an electrical contractor, that creates a decision with major financial consequences.

When workers' comp IS required:

- Government contracts (Texas Labor Code Section 406.096)

- Public school and school district projects (Labor Code Chapter 504)

- Any contract where the client mandates coverage

When workers' comp is optional:

- Private residential jobs

- Private commercial projects (unless the contract requires it)

The risk of opting out is real. Under Texas Labor Code Section 406.033, non-subscribing employers lose common-law defenses including contributory negligence, assumption of risk, and fellow-employee negligence. An injured employee can sue you directly, with your legal defenses largely stripped away.

The injury data makes this decision even clearer: BLS reported 130 fatal injuries from exposure to electricity in 2024, and during 2016–2020, 76.1% of electrician fatalities were caused by electrical exposure. Electrical work is genuinely dangerous. The claims aren't hypothetical.

Additional Coverage Types to Carry

Beyond GL and workers' comp, most Texas electrical contractors need three additional policies:

- Commercial Auto: Required for any vehicle used in business operations. Personal auto policies exclude business use, and Texas law treats them as separate coverage categories. This applies to service trucks, tool vans, and any crew vehicle.

- Tools and Equipment (Inland Marine): Covers electrical testing equipment, panel components, wire, and specialty tools against theft, loss, or damage at jobsites and in transit — gaps GL doesn't fill.

- Commercial Umbrella: Extends your liability limits above the base GL and auto thresholds. Hospitals, data centers, and government contracts routinely specify total limit amounts that base policies alone can't meet.

Coverage Limits, Certificates, and Municipal Requirements

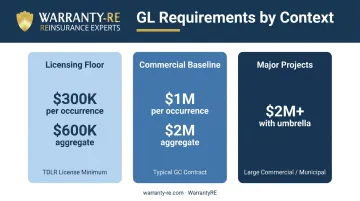

State Minimum vs. Commercial Benchmark

The gap between what TDLR requires and what commercial clients expect is wider than most contractors expect:

| Context | GL Requirement |

|---|---|

| TDLR license minimum | $300K per occurrence / $600K aggregate |

| Typical GC contract requirement | $1M per occurrence / $2M aggregate |

| Large commercial / municipal projects | Often $2M+ with umbrella |

If you're bidding commercial or industrial work, plan for $1M/$2M as your working baseline — not the state minimum.

Certificate of Insurance Requirements

Carrying the right insurance isn't enough on its own. You need to be able to produce properly worded COIs before permits are pulled and before work begins. General contractors and municipalities commonly require:

- Additional Insured — adds the GC or property owner to your policy

- Primary and Non-Contributory — your coverage pays first, regardless of other policies

- Waiver of Subrogation — prevents your insurer from pursuing the GC to recover paid claims

Have these endorsements ready before you show up to a pre-construction meeting. Projects stall when the COI doesn't match what the contract requires.

City-Level Registration and Insurance Requirements

Each major Texas city runs its own contractor registration system tied to permit access:

- Dallas — Requires electrical contractor registration with GL at minimum $300,000 per occurrence for combined bodily injury and property damage

- San Antonio — All city and state licensed contractors must register with Development Services before permits are issued; registration tiers reflect liability insurance thresholds

- Austin — Contractors must register before obtaining trade permits; municipal project contracts require CGL of $500,000 per occurrence, auto liability of $500,000, additional insured status, and waiver of subrogation

- Houston — Licensed and registered contractors may apply for electrical trade permits; city contracting documents include additional insured and primary coverage requirements

Verify registration requirements directly with the city where you're working — municipal portals update more often than most contractors realize, and a lapsed registration can hold up permits on active jobs.

Texas Workers' Compensation: What Electrical Contractors Must Know

Non-Subscriber Status and What It Costs You

When a Texas private employer opts out of the workers' comp system, they become a "non-subscriber." That status carries direct legal consequences.

Under Labor Code Section 406.033, non-subscribers cannot use these defenses against employee injury lawsuits:

- Contributory negligence of the employee

- Assumption of risk

- Negligence of a fellow employee

And under Labor Code Section 408.001, workers' comp benefits are the exclusive remedy when coverage exists — meaning an employee with coverage generally can't sue the employer for a covered injury. That protection disappears when you opt out.

For an electrical contractor with a crew of five running commercial jobs, a single serious injury lawsuit without workers' comp coverage could exceed any other liability exposure you carry.

When Coverage Becomes Mandatory

That liability exposure matters even more once public work enters the picture. Texas Labor Code Section 406.096 requires contractors performing work on public building or construction contracts with governmental entities to provide workers' compensation for their employees. This applies to:

- City and county projects

- State agency construction

- Public school district work

- Projects where prime contractors must ensure subcontractors carry coverage

If you're bidding public work in Texas, workers' comp isn't optional.

The Practical Recommendation

BLS data shows 397 electrician fatalities during 2016–2020, with 1,668 nonfatal injury cases involving days away from work in 2020 alone. Most established electrical contractors in Texas carry workers' comp regardless of the legal requirement. One lawsuit from an injured employee, without coverage, can eliminate years of profit and put the entire business at risk.

What Affects Electrical Contractor Insurance Costs in Texas

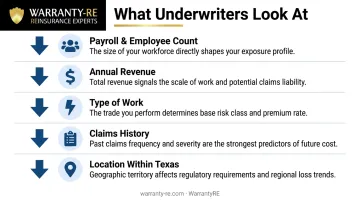

Primary Underwriting Factors

Underwriters look at several variables when pricing your coverage:

- Payroll and employee count — more employees means more exposure

- Annual revenue — higher revenue signals larger projects and greater risk

- Type of work — industrial and high-voltage commercial work costs more to insure than residential service calls

- Claims history — past claims are the strongest predictor of future premiums

- Location within Texas — urban markets sometimes carry different risk profiles

Market Benchmarks (Non-Guaranteed Estimates)

These figures come from national insurance marketplace data and are not Texas-specific guarantees. Your actual premiums will vary based on carrier, scope, and business profile:

| Coverage | Median Monthly Estimate |

|---|---|

| General Liability | $37–$57/month (small operators) |

| Workers' Compensation | $119–$217/month |

A combined GL, workers' comp, and commercial auto package for a small-to-mid-sized Texas electrical contractor could range considerably depending on payroll size and the mix of residential versus commercial work. Always get quotes from multiple carriers — these benchmarks are a starting point, not a ceiling or a floor.

Managing Your Costs

- Bundle policies with one carrier when possible — multi-policy discounts are common

- Classify employees accurately by work type — misclassification triggers audit penalties and can void coverage

- Maintain a clean claims record — it's the single biggest lever for long-term premium management

- Complete safety certifications — some carriers discount premiums for OSHA training and documented safety programs

- Keep payroll reporting accurate — workers' comp audits verify W-2s, 1099s, ledgers, and subcontractor COIs; underreported payroll results in additional premium due at audit

Building Long-Term Business Protection Beyond Insurance

Insurance limits your losses when something goes wrong. But there's a separate financial opportunity built into every job you complete — one most electrical contractors hand off to someone else without realizing it.

Every time you complete a panel upgrade, service installation, or wiring project, there's a labor warranty attached to that work. The moment your electrician makes a connection, the labor responsibility is yours — no equipment manufacturer covers it. Most contractors either absorb those warranty callbacks out of pocket or pay a third-party warranty provider to take on the risk.

WarrantyRE offers a different structure. As a reinsurance partner for home service contractors, WarrantyRE helps electrical contractors establish their own reinsurance company — one they legally own — to capture the warranty profits that would otherwise go to a third party.

Here's how it works in practice:

- A small warranty fee is built into every job price — on an $18,000 service upgrade with a 2-year labor warranty, the fee is already in the bid

- That fee flows into a reinsurance structure the contractor owns — building a pool in your company, not a third party's

- Claims are covered from the pool — callbacks for loose neutrals, tripping breakers, or connection failures are handled through the reinsurance account

- Unused funds stay with the contractor — with contributions that carry meaningful tax advantages at year-end

WarrantyRE handles the administration, compliance, claims adjudication, and tax planning — so your electricians stay focused on billable work rather than warranty logistics.

The full protection picture for an electrical contractor has two sides: the right insurance coverage limits your exposure when something goes wrong, and a warranty reinsurance structure turns completed jobs into retained profit rather than transferred income.

Frequently Asked Questions

What insurance does an electrical contractor need in Texas?

The core coverage types are general liability (required by TDLR for licensing), workers' compensation (required on public/government jobs and strongly advisable on all others), commercial auto, and tools and equipment insurance. Specific requirements depend on the type of work you perform and what your client contracts require.

Can an electrical contractor work without insurance in Texas?

Texas doesn't mandate every coverage type for every private contractor, but working without GL insurance risks your TDLR license eligibility and blocks you from pulling permits in most major cities. In practice, most general contractors and commercial clients require proof of insurance before work begins — being uninsured means losing access to most jobs.

Is workers' compensation required for electrical contractors in Texas?

Not for most private-sector work — Texas is the only state where workers' comp is optional for private employers. It is legally required under Texas Labor Code Section 406.096 for government contracts, and opting out removes your exclusive remedy defense, exposing you to direct employee lawsuits.

What is a surety bond, and do Texas electrical contractors need one?

A surety bond protects clients if a contractor fails to complete work or pay subcontractors. There is no statewide TDLR surety bond requirement for electrical contractors, though individual cities and clients may require one — confirm before bidding.

How much does electrical contractor insurance cost in Texas?

General liability typically runs $37–$57/month and workers' comp $119–$217/month for smaller operations, though commercial and industrial contractors usually pay more. Final costs depend on payroll, work type, employee count, and claims history — get quotes from multiple carriers for an accurate figure.

What happens if an electrical contractor in Texas operates without required insurance?

Without the required COI on file, TDLR can deny license applications or renewals. You also lose the ability to pull permits in Dallas, San Antonio, Austin, and Houston, which require contractor registration tied to valid insurance. For workers' comp specifically, non-subscribers lose statutory legal defenses if an employee is injured and files suit.