The financial exposure is real. So are the customer disputes, the reputational damage, and the out-of-pocket costs for rework that no policy will reimburse.

This article covers the four things every contractor needs to understand before a claim arrives:

- The three warranty layers that apply simultaneously to any installation project

- How CGL and professional liability insurance actually respond to installation defects

- The specific policy exclusions most likely to leave you exposed

- Practical steps to build a stronger warranty and documentation strategy

TL;DR

- Three separate warranty layers apply to every installation: manufacturer, workmanship, and program-backed — each with different owners and claim paths

- CGL does not cover the cost to redo your own faulty work — only damage to surrounding third-party property

- Professional liability exclusions — faulty workmanship, warranty, product liability — can deny claims contractors assume are covered

- Non-conforming installation can void manufacturer warranties, shifting the full cost to the contractor

- Contractors can own their warranty program through a reinsurance structure — keeping profits instead of paying them to third parties

The Three Warranty Layers That Apply to Every Installation

In any roofing, HVAC, plumbing, or electrical project, three distinct warranty types exist simultaneously. Each has a different owner, duration, and enforcement path. None of them covers everything on its own.

Manufacturer (Material) Warranty

Manufacturer warranties cover defects in the product itself, not installation errors. A failed seal, improper refrigerant charge, or incorrect duct connection falls outside this coverage entirely — that's on the installer.

Major manufacturers also tie their enhanced warranty tiers to specific eligibility conditions:

| Manufacturer | Registration Window | Credential Requirement |

|---|---|---|

| GAF (roofing) | 45 days post-install | Certified or Master Elite contractor |

| Carrier (HVAC) | 90 days post-install | Consumer Choice program participation |

| Trane (HVAC) | 60 days post-install | Registration required |

| Lennox (HVAC) | 60 days post-install | Licensed HVAC installer required |

Miss the registration window and the enhanced tier is gone, even if the underlying materials are sound. GAF defaults to a base warranty. Carrier drops to a standard 5-year parts-only limited warranty. Trane reverts to its Base Limited Warranty. These aren't edge cases — they're the default outcome when registration falls through the cracks.

Contractor Workmanship Warranty

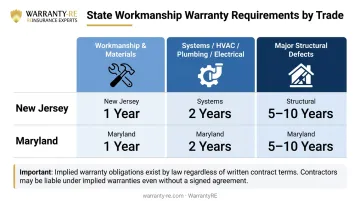

The workmanship warranty covers installation quality, labor errors, and construction defects. Duration varies by trade and state:

| State | Workmanship & Materials | Systems (HVAC, Plumbing, Electrical) | Major Structural Defects |

|---|---|---|---|

| New Jersey | 1 year | 2 years | 10 years |

| Maryland | 1 year | 2 years | 5 years |

One point contractors often miss: most states recognize an implied warranty of workmanlike performance regardless of what the written contract says. As California's CACI No. 4510 states, the duty to perform in a competent manner is implied by law — it doesn't need to appear in the agreement. Silence in your service contract doesn't eliminate your workmanship exposure.

Insurer-Backed or Program Warranty

Some direct repair programs and preferred vendor networks have the insurer back the contractor's workmanship for a fixed term. In this structure, the homeowner's contractual recourse runs through the insurer rather than directly to the contractor. In practice, that means the insurer controls claim approvals, repair timelines, and contractor selection — not you.

What Insurance Covers — and Doesn't — When Installations Go Wrong

Most contractors carry a commercial general liability policy and assume it protects them against installation-related complaints. The reality is more nuanced, and the gaps are where the expensive surprises live.

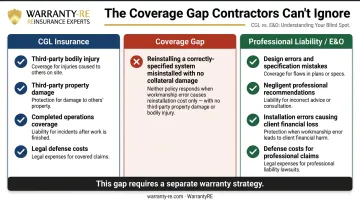

What CGL Insurance Covers

CGL responds to bodily injury or property damage caused in the course of work. The classic example: a faulty HVAC installation causes a fire that damages drywall and structural framing beyond the unit itself. CGL covers the cost to repair that surrounding property damage, plus related medical and legal costs.

CGL policies are typically occurrence-based, meaning the triggering event must occur during the policy period — even if the claim is filed later. An improperly sealed roof flashing that caused moisture damage during the policy term can still trigger coverage.

The key condition: the damage must have occurred while the policy was active, regardless of when it's discovered.

What CGL will not cover: the cost to redo or repair the contractor's own work. IRMI's analysis of faulty work and the CGL confirms the own-work exclusion removes coverage for repairing the insured's own installation. If the HVAC unit simply needs to be reinstalled correctly and no surrounding property was damaged, that cost is out of pocket.

What Professional Liability Insurance Adds

Contractors professional liability — also called errors and omissions (E&O) — fills some CGL gaps by covering errors made during the design, engineering, or installation of systems. For HVAC, plumbing, and electrical contractors, this is where installation defect claims most often land.

Professional liability does carry its own exclusions, though — and that's where the remaining exposure lives.

What Neither Policy Covers

When faulty work causes no damage beyond the installation itself, neither CGL nor professional liability responds. The contractor absorbs the full cost of redoing the work. Here's what that gap looks like in practice:

- CGL: Covers third-party property damage and injury — not the contractor's own work

- Professional liability (E&O): Covers design and installation errors — but excludes pure redo costs with no collateral damage

- Neither policy: Covers pulling and reinstalling a misinstalled HVAC system when nothing else was damaged

That exposure sits entirely outside the insurance envelope, which is why contractors need a separate strategy for managing labor warranty risk.

The Exclusions That Catch Contractors Off Guard

Within professional liability and CGL policies, specific exclusions are routinely triggered in installation defect claims. IRMI's breakdown of the contractors professional liability policy confirms these forms are non-standardized — meaning the same exclusion can be written broadly in one policy and narrowly in another.

The Faulty Workmanship Exclusion

Most professional liability policies include a faulty workmanship exclusion. Broader versions cover any error in installation, including failure to follow manufacturer specifications. Narrower versions may only apply to self-performed structural work.

The practical fix: review the exact policy language before a claim surfaces. Some insurers — Berkley, for example — offer a faulty workmanship liability endorsement that provides coverage for repair or replacement of faulty workmanship performed by the insured. That endorsement can be the difference between a covered claim and an out-of-pocket loss.

The Warranty Exclusion

According to Ames & Gough, professional liability policies commonly exclude liability arising from oral or written warranties or guarantees. That means the warranty language in your service agreement can inadvertently trigger a coverage denial — the insurer argues you failed a contractual warranty obligation rather than committed a professional error.

Review your service agreement warranty language alongside your policy terms before you sign either — not after a claim forces the issue.

The Product Liability Exclusion

This exclusion draws a line between problems caused by the contractor's work and problems caused by the product's design or manufacture. Stricter policies exclude all products used on a job. More flexible policies carve out exceptions for custom-specified products. Contractors who skip this verification step often find themselves caught between the manufacturer's denial and their own insurer's exclusion — with no clear path to coverage.

Key questions to ask your broker about this exclusion:

- Does it apply to all third-party products used on a job, or only those you specify?

- Are there carve-outs for custom-specified or engineer-selected products?

- What documentation do you need to support a covered claim if a product fails?

How Non-Conforming Installation Voids Manufacturer Warranties

Install a product outside the manufacturer's published specifications and the warranty may be void entirely — regardless of whose fault the defect actually is.

Specific consequences by manufacturer:

- GAF: Wind coverage voided if fastening doesn't strictly follow printed instructions

- Lennox: Non-licensed service or installation not per Lennox instructions explicitly excluded

- CertainTeed SureStart PLUS: Wind upgrades void if incompatible starter or ridge accessories are used

- Carrier/Trane: Registration failure drops the coverage tier automatically

The 2021 International Residential Code (Section M1401.1) requires HVAC equipment to be installed per manufacturer's instructions and applicable code. Non-conforming installation creates both a code violation and a warranty voidance simultaneously — doubling the contractor's exposure.

When Warranty Claims and Insurance Claims Overlap

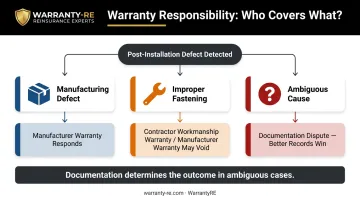

When a defect surfaces post-installation, the threshold question is almost always: is this a material failure or a workmanship failure?

The answer determines everything — who's responsible, which warranty responds, and whether any insurance policy applies. And the answer is typically determined by physical evidence.

Consider a roofing example. A leak develops 18 months after installation. Three possible root causes, three different outcomes:

- Manufacturing defect in shingles → Manufacturer warranty responds (if registered and within coverage terms)

- Improper fastening pattern → Contractor workmanship warranty applies; manufacturer warranty may be partially or fully void

- Ambiguous cause → Both parties dispute liability; whoever has better documentation wins

The National Roofing Contractors Association draws this line explicitly: manufacturer coverage addresses defects in the manufacture of roof covering material, while the roofing contractor provides workmanship coverage. They're separate instruments that respond to separate failure types.

When root cause isn't obvious, documentation is what separates a manageable claim from a prolonged dispute. The records that matter most:

- Registration confirmation and product serial numbers

- Installation date and installer credentials

- Spec-compliance evidence and inspection photos

Industry data consistently shows that construction defect claims involving incorrectly installed systems are resolved — or lost — based on what's in the file. Contractors with thorough records walk away with defensible positions; those without them absorb costs they shouldn't owe.

Documentation gaps carry an added cost for contractors working through preferred vendor or direct repair programs. When the homeowner's contractual recourse runs through the insurer, the insurer controls dispute resolution — and incomplete records tend to resolve in the insurer's favor, not the contractor's.

The Hidden Cost of Relying on Third-Party Warranty Providers

Many contractors currently pay premiums to third-party warranty companies to back their workmanship guarantees. When claims are low — as they typically are for skilled contractors — contractors lose those premium dollars permanently.

If third-party warranty providers weren't profitable, they wouldn't exist. The underwriting margin — the gap between premiums collected and claims paid — is substantial for contractors with clean installation records. That margin leaves their business every year.

How a Contractor-Owned Reinsurance Structure Works

Rather than sending that margin to a third party, contractors can establish their own administrator-obligor reinsurance company. WarrantyRE has helped contractors in the HVAC, roofing, plumbing, and electrical trades build these structures since 1994.

The mechanics at a high level:

- Warranty fees are built into job pricing and flow into the contractor's own reinsurance company rather than to an outside provider

- Claims are paid from the contractor's reserve pool — covered without out-of-pocket cost to the contractor

- Unused reserves stay with the contractor — the underwriting profit that third-party providers capture instead accumulates in the contractor's own structure

- A-rated insurers back the program — if the contractor's reinsurance company cannot meet its obligations, the direct writing insurance company assumes liability, limiting the contractor's exposure to formation costs plus accumulated earnings

WarrantyRE handles full program administration: claims adjudication, compliance, financial reporting, and staff training. The contractor carries no additional administrative burden, retains legal ownership of the reinsurance company, and stays in direct control of the warranty experience delivered to customers.

How Contractors Can Build a Stronger Warranty Strategy

Three concrete actions that reduce exposure before a claim surfaces:

1. Audit your insurance policies now, not after a claim. Review your CGL and professional liability policies for faulty workmanship exclusions, warranty exclusions, and product liability exclusions. Non-standardized forms mean these provisions vary significantly between policies. Review with a licensed insurance professional who understands contractor-specific coverage.

2. Align your warranty contract language with your insurance policy. Written warranty promises in service agreements can trigger professional liability exclusions if they're broader than what the policy covers. Before using warranty language in any contract, check it against your policy terms. Be specific: what's covered, for how long, and under what conditions.

3. Document every installation as if you'll need the records in court. The documentation that resolves disputed claims includes:

- Registration confirmation within the manufacturer's required window (GAF: 45 days; Carrier: 90 days; Trane/Lennox: 60 days)

- Installer credentials and license documentation in the job file

- Serial numbers, model numbers, and installation date on record

- Spec-compliance evidence showing installation followed manufacturer instructions

- Phase photos confirming workmanship at key stages

This file is your primary defense when the root cause of a defect is disputed. Contractors who can't produce it often absorb costs that should have gone to a manufacturer or insurer — and that's a preventable loss.

Frequently Asked Questions

Does insurance cover defective workmanship?

Standard CGL insurance covers damage to third-party property caused by faulty work, not the cost to redo the work itself. Professional liability may cover some installation errors, but faulty workmanship exclusions often limit or deny those claims depending on policy language.

What is the difference between a manufacturer warranty and a workmanship warranty?

A manufacturer warranty covers defects in the product itself — materials and components. A workmanship warranty covers errors made during installation. They're separate instruments with different owners, durations, and claim processes, and each can be voided independently of the other.

What does a general liability policy exclude for installation defects?

CGL policies commonly exclude three categories relevant to installation defects: the your-work exclusion (cost to redo the contractor's own work), faulty workmanship claims, and warranty-based disputes. Product liability coverage may apply to material failures, but contractor error typically falls outside standard CGL scope.

How long does a contractor's workmanship warranty typically last?

Duration varies by trade and state — commonly 1 year for general workmanship and up to 10 years for structural or mechanical systems. Many states also impose implied warranty obligations by law regardless of what the written contract states, meaning silence doesn't eliminate exposure.

What happens when a warranty claim and an insurance claim overlap for the same defect?

The key distinction is whether the defect is a material failure (manufacturer's responsibility) or a workmanship failure (contractor's responsibility). Without clear documentation and physical evidence to separate the two, contractors often absorb costs that should fall on another party.

Can a contractor own and control their own warranty program instead of relying on a third party?

Yes. Through a contractor-owned reinsurance structure, contractors form their own administrator-obligor company supported by A-rated insurers. That setup retains underwriting profits in-house and keeps claims control with the contractor rather than a third party. WarrantyRE has built these programs for contractors since 1994.