Introduction

A surprisingly common belief among home service contractors and auto dealers is that warranty reinsurance programs are reserved for large corporations with deep pockets and high-volume operations. That assumption is wrong — and expensive. Every contract sold through a third-party warranty provider sends underwriting profit out the door that a qualified business owner could be keeping.

Most mid-sized contractors and independent dealers already meet the core qualifications. The volume thresholds are lower than most expect, and the structure is built to work with what you're already doing.

This guide covers:

- What warranty reinsurance actually is and how it works

- Who qualifies — and what the real entry requirements look like

- The specific financial and operational benchmarks to meet

- The step-by-step path to getting a program started

By the end, you'll know exactly where your business stands.

TL;DR

- Warranty reinsurance lets you own the company that keeps underwriting profit from your service contracts, not a third-party provider

- Most home service contractors (HVAC, roofing, plumbing, electrical) and auto dealers already qualify

- No personal insurance license required — the fronting carrier and administrator handle regulatory obligations

- WarrantyRE handles claims, compliance, filings, and tax returns on your behalf

- The first step is a free business and volume assessment — not a large upfront commitment

What Warranty Reinsurance Actually Is

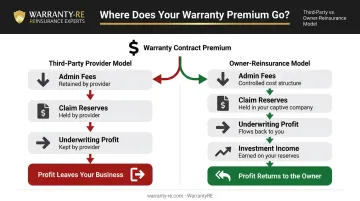

Warranty reinsurance is a property and casualty financial structure — one that lets a business owner establish and operate their own warranty company rather than paying a third party to do it.

The core mechanism works like this: when you sell service contracts or labor warranties through a third-party provider, that provider collects the premium, pays claims from it, and keeps whatever is left as underwriting profit. If your customers rarely file claims, the provider wins — and you see nothing beyond your initial commission or margin.

A contractor-owned or dealer-owned reinsurance company flips that arrangement. As Mercer Capital explains, the contract premium is split among administrative fees, third-party costs, and claim reserves — and underwriting profit is realized when claims are lower than the reserves collected, plus investment income generated while reserves are held.

Where 831(b) Comes In

The IRC Section 831(b) tax election adds a meaningful financial layer. It allows eligible small property and casualty insurance companies to be taxed on investment income only, rather than on underwriting income. IRS Rev. Proc. 2025-32 sets the 2026 premium limit at $2,900,000 — within reach for most contractors and dealers.

This is a qualified-tax-advisor conversation, but it's a meaningful part of how reinsurance programs are structured for eligible clients. WarrantyRE's FAQ addresses the 831(b) election directly, including how it factors into program setup for contractors and dealers exploring this path.

Who Qualifies for Warranty Reinsurance

Eligible Business Types

Warranty reinsurance is available to a wider range of businesses than most people realize:

- Home service contractors — HVAC, roofing, plumbing, electrical, and general contractors

- Auto dealers — franchise, retail, Buy Here Pay Here (BHPH), and independent dealers

- F&I-focused dealer principals who sell vehicle service contracts (VSCs), GAP, and ancillary products

The U.S. home maintenance services market — including HVAC and plumbing — represents a $543 billion industry made up mostly of small local businesses and franchises. The opportunity exists at every level of that market, not just the top.

Volume: What's Actually Required

This is where most contractors and dealers are surprised. Published administrator benchmarks for auto dealers typically suggest 25–30 vehicle service contracts per month (or 300–350 annually) as a viability threshold for a producer-owned reinsurance company. Some programs model examples using as few as 20 VSCs per month.

For home service contractors, no published minimum exists — but the principle holds: consistent warranty or service contract sales are what fund the reserve meaningfully. The biggest misconception in this space is that you need massive volume or significant upfront capital to get started. You don't.

Other Baseline Qualifications

Beyond volume, qualifying businesses generally need to:

- Have an existing customer base purchasing warranties or service contracts (whether sold separately or bundled with installations)

- Operate as a legitimate, registered business entity

- Be willing to form a separate reinsurance company (typically a corporation) to hold the reinsurance structure

- Not have any specific insurance license personally — the administrator and fronting carrier handle that

What You Need to Qualify: Key Requirements

Financial Readiness

There is an initial capital contribution to establish the reinsurance trust account. The amount varies by program structure, administrator, and domicile requirements — state captive statutes set their own capital and surplus minimums, and these differ by jurisdiction. No universal figure applies across all programs.

What's consistent: the startup cost is lower than most contractors assume, and warranty fee income from your existing customers funds ongoing reserves — not out-of-pocket capital.

A Warrantable Product or Service

Your business must offer something customers can buy a warranty or service contract on. For home service contractors, that means:

- Labor warranties on installations (furnaces, AC units, roofing, repiping, panel upgrades)

- Service plans and maintenance agreements

- Workmanship warranties built into project pricing

For dealers, that means VSCs, GAP, tire and wheel protection, and other F&I ancillary products. The key point: manufacturers cover parts — the labor exposure is what reinsurance addresses for contractors.

A Licensed Program Administrator

Once you have a warrantable product, you need someone to run the program compliantly. A qualified administrator like WarrantyRE handles:

- Claims adjudication (first call through final resolution)

- Compliance management and regulatory filings

- Monthly financial statements and bookkeeping

- Annual tax returns and renewals

- Performance reporting

Your role is to sell warranties and review results. The administrator handles everything else.

A-Rated Fronting Insurer

Per IRMI's definition, a fronting insurer is a licensed, admitted carrier that issues the policy, takes a fee, then cedes the risk back to your reinsurance company. This arrangement keeps you on the right side of consumer protection requirements and state insurance regulations.

WarrantyRE's programs are backed by A-rated insurers — carriers rated "Excellent" or better by AM Best — confirming their ability to meet ongoing policy obligations.

Common Myths About Who Can Qualify

Myth 1: "You Have to Be a Large Business"

Mercer Capital confirms that reinsurance is accessible to small and mid-sized dealers. The same holds for contractors.

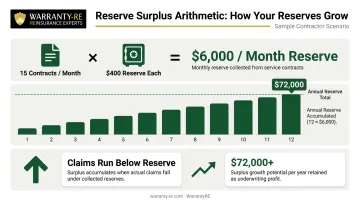

Consider a simple illustration: if a contractor sells 15 labor warranties per month with $400 flowing into reserve from each, that's $6,000 in monthly reserve accumulation — $72,000 annually before investment income. If actual claims run below reserve levels (which is common for quality installers with low callback rates), the surplus builds inside an account the owner controls.

That's the basic arithmetic of how reserve surplus works. Your actual numbers depend on claim frequency and contract values, which a reinsurance assessment can model for you.

Myth 2: "You Need an Insurance License"

The business owner functions as the reinsurer — not the direct insurer. The fronting carrier holds the insurance license. The program administrator maintains compliance with state and federal regulatory requirements. You own the reinsurance company; you don't operate as an insurer.

Myth 3: "It's Too Complicated to Manage"

Full-service administration is what makes this myth collapse on contact. With WarrantyRE, there's no extra admin on your end, no adjusters to manage, no claims paperwork to chase. The team handles everything from the first call to final resolution — your job is to keep technicians in the field on paying work.

The Step-by-Step Path to Getting Started

Step 1 — Business and Volume Assessment

A reinsurance administrator reviews your current warranty sales volume, average contract value, and estimated loss ratio. WarrantyRE typically provides this analysis at no initial cost. The goal is to determine whether program economics make sense for your specific book of business before any commitments are made.

Step 2 — Program Structure Selection

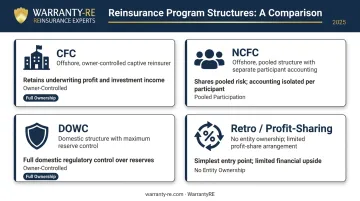

The right structure depends on your volume, tax goals, and desired level of control. Common options include:

- Controlled Foreign Corporation (CFC) — offshore entity controlled by the owner, commonly used to retain underwriting profit and investment income

- Non-Controlled Foreign Corporation (NCFC) — pooled offshore structure with separate accounting for each participant

- Dealer/Contractor-Owned Warranty Company (DOWC) — domestic structure with greater control over reserves and claims

- Retro/profit-sharing — not a reinsurance structure; profit participation without entity ownership (see FAQ below)

Your administrator guides this decision based on your specific profile.

Step 3 — Company Formation

With your structure selected, WarrantyRE manages the full formation process:

- Naming and registering the reinsurance entity

- Establishing the trust account (funds remain in a U.S. trust company)

- Completing state and regulatory filings

- Arranging the fronting insurer agreement

No legal or compliance work falls to the business owner.

Step 4 — Onboarding and Staff Training

Once the company is formed, your team goes through onboarding that covers:

- How to present warranties to customers

- How claims are submitted and tracked

- How to read performance and financial reports

WarrantyRE offers both online and in-person training formats.

Step 5 — Ongoing Program Management

After launch, the administrator handles:

- Monthly financial statements covering all reinsurance activity

- Claims management from submission through resolution

- Trust account monitoring, including investment of surplus funds

- Annual tax returns and renewals

- Periodic owner reviews to assess financial direction

Your role is straightforward: review the reports, ask questions, and use the data to make informed decisions about your business. WarrantyRE handles the rest.

Why Your Choice of Administrator Matters

The administrator you choose has a direct impact on how much profit you retain and how cleanly the program runs. Weak claims handling, hidden fees, and poor compliance management all erode the underwriting profit the program is designed to capture.

When evaluating a reinsurance partner, look for:

- Experience with your specific business type (contractor vs. dealer)

- Transparent fee structure with no hidden charges

- A-rated insurance backing

- In-house claims adjudication

- Full compliance and regulatory management

One administrator that checks all five is WarrantyRE. Founded by Tim Byrd in Southeast Virginia in 1994, the company has spent over 30 years helping 400+ contractors and dealers run profitable programs — handling claims, compliance, financials, and filings under one roof.

The guiding principle is simple: if you win, we win. That shared incentive is what separates a true partner from a vendor who profits whether your program performs or not.

Frequently Asked Questions

What is the 72-hour clause in reinsurance?

The 72-hour clause groups losses occurring within a 72-consecutive-hour period — typically from storms, floods, or earthquakes — into a single occurrence for claims purposes. It's a property catastrophe reinsurance provision and does not apply to contractor or dealer warranty reinsurance programs.

Do small contractors really qualify for warranty reinsurance?

Yes. Volume thresholds are lower than most assume, and a reinsurance administrator can assess eligibility based on your actual warranty sales figures. WarrantyRE works with contractors of varying sizes across all home service trades.

Do I need an insurance license to own a warranty reinsurance company?

No. The program is backed by a licensed fronting insurer, and the administrator manages all regulatory compliance. The business owner functions as the reinsurer, not the direct insurer — no personal producer license is required.

How long does it take to set up a warranty reinsurance company?

Setup timelines vary by structure and state filing requirements. Most programs complete company formation and launch within 4–8 weeks when working with a full-service administrator.

What is the difference between a retro profit-sharing program and full reinsurance?

Retro programs return a limited share of underwriting profit after claims and expenses, under conditions set by the third-party provider. The dealer or contractor does not own an insurance entity. Full reinsurance gives the owner direct ownership of the trust account and full access to earned surplus, typically resulting in greater long-term profit retention.

What happens to my trust account if I stop selling warranties?

The trust account continues paying claims as existing contracts run off. Once all obligations are settled, the remaining surplus belongs to the reinsurance company owner.