Introduction

A single incident can undo months of work. A client trips over your cable management on a commercial panel job, files a suit, and suddenly you're looking at legal fees before any settlement is even discussed. A crew member takes a shock during a service upgrade, and without workers' comp, those medical costs come straight out of your operating account. A wiring issue surfaces three months after a job closes, and your general liability policy won't touch it.

Electrical work sits at the higher end of the risk spectrum among all the trades. According to the NFPA, electrical failures and malfunctions caused an estimated average of 527 civilian deaths, 1,580 injuries, and $2.4 billion in direct property damage annually between 2020 and 2024. That exposure runs in both directions — toward your clients' property and toward your own crew.

That's exactly why getting your coverage right matters. This guide covers the core and optional insurance types electrical contractors need, what each policy typically costs, what factors push premiums up or down, and where standard insurance leaves a gap worth addressing separately.

TL;DR: Key Takeaways

- General liability, workers' comp, commercial auto, and commercial property (or a BOP) are the minimum coverage set for most electrical contractors

- Most states require GL and workers' comp for contractor licensure — and nearly all commercial contracts demand both

- Annual costs run roughly $685 for GL alone up to $5,000–$6,000+ when adding workers' comp and commercial auto

- A Business Owner's Policy bundles GL and commercial property at a lower combined cost than buying each separately

- Standard insurance excludes warranty callbacks on completed work — electrical contractors close that gap with a contractor-owned warranty reinsurance program

Why Electrical Contractors Need Specialized Insurance

Electrical work isn't like drywall or painting. Live panels, exposed wiring, and active circuits create injury and property damage scenarios that happen fast and cost a lot. BLS data shows 70 fatal work injuries for electricians in 2020, with electric shock and falls among the leading causes.

The liability exposure runs in multiple directions simultaneously:

- Third-party property damage — faulty wiring causes a fire at a client's facility

- Third-party bodily injury — someone trips over your equipment on a job site

- Employee injuries — a crew member falls during a panel installation or takes a shock

- Vehicle accidents — one of your work trucks rear-ends another vehicle between job sites

- Completed-work claims — a client discovers an installation issue months after the job closes

Each of those exposures carries a real price tag when you're uninsured.

The Cost of Being Uninsured

Going without coverage creates predictable financial exposure that compounds over time. Common consequences include:

- Out-of-pocket settlements for property damage or bodily injury claims

- Full employee medical costs and lost wages without workers' comp

- Lost contract bids because you can't provide a certificate of insurance

- License suspension or denial in states that require proof of coverage

Most state contractor licensing boards require proof of general liability insurance before issuing or renewing an electrical contractor license. Commercial clients and general contractors require a certificate of insurance before allowing any subcontractor on-site. In practice, insurance is the entry ticket to most commercial work.

Core Insurance Policies Every Electrical Contractor Needs

No single policy covers everything electrical contractors face. A complete program stacks several policies together, each targeting a specific category of risk — from job-site injuries to vehicle accidents to property loss.

General Liability Insurance

General liability (GL) covers third-party bodily injury, property damage, and advertising injury claims. If your crew damages a client's wall during a rough-in, or a visitor trips over your equipment, GL handles legal fees, settlements, and repair costs.

Most states require proof of GL as a condition of electrical contractor licensure. Minimum state limits vary — Texas requires $300,000 per occurrence, Philadelphia requires $500,000, and Florida's requirements differ by license class. The market standard for commercial work is typically $1 million per occurrence / $2 million aggregate.

Workers' Compensation Insurance

Workers' comp covers medical expenses, lost wages, and rehabilitation for employees injured on the job. Electric shock, falls, and overexertion injuries are all documented electrician injury categories in BLS data.

Most states require workers' comp as soon as you hire your first employee — including part-time and temporary workers. California requires it even for one-person construction businesses.

Requirements vary significantly by state. Some, including Tennessee, apply special rules to sole proprietors in the construction trades. Verify your state's rules with the contractor licensing board or your insurance broker before assuming you're exempt.

Commercial Auto Insurance

Your work trucks are on the road daily, and that creates consistent liability exposure. Commercial auto covers accidents, damage, and theft involving vehicles used for business purposes.

Two critical gaps apply if you skip this policy:

- Personal auto insurance typically excludes vehicles used primarily for business purposes

- A Business Owner's Policy does not provide any vehicle coverage

Common commercial auto liability limits are $500,000 to $1,000,000. Most states also require at least minimum statutory auto liability coverage for any vehicle used commercially.

Commercial Property Insurance

Commercial property covers the physical space your business uses — shop, office, storage — and the tools, equipment, and inventory inside it. For electrical contractors storing breakers, conduit, wire, and diagnostic gear, this protection matters.

Covered perils typically include fire, storm damage, vandalism, and theft. Note that this covers your property at your business location. Damage you cause to a client's property on a job site falls under GL, not commercial property.

Business Owner's Policy (BOP)

A BOP bundles GL and commercial property into a single policy at a lower combined cost than buying each separately. Most insurers require businesses to have fewer than 100 employees and under $1 million in annual revenue to qualify.

Many BOPs also include business interruption coverage, which helps replace lost income if a covered event forces a temporary shutdown. What a BOP does not cover: vehicles, workers' comp, or job-specific liability beyond standard GL. Those require separate policies regardless of business size.

Policy Coverage at a Glance

| Policy | What It Covers | Typically Required? |

|---|---|---|

| General Liability | Third-party injury, property damage, advertising injury | Yes — most state licenses |

| Workers' Compensation | Employee injuries, lost wages, rehabilitation | Yes — most states (1+ employee) |

| Commercial Auto | Business vehicle accidents, damage, theft | Yes — any commercially used vehicle |

| Commercial Property | Your shop, tools, equipment, inventory | No — but strongly recommended |

| Business Owner's Policy (BOP) | GL + property bundled; often includes business interruption | No — but cost-efficient for smaller shops |

Additional Coverage Options Worth Considering

The core policies above cover most scenarios. These additional options address gaps that emerge as electrical businesses grow or take on commercial work.

Professional Liability (E&O): Covers claims tied to professional mistakes discovered after job completion — for example, a commercial client claiming a panel wiring error caused equipment damage six months later. GL does not cover this scenario. E&O is increasingly required on commercial contracts.

Commercial Umbrella Insurance: Extends your liability limits beyond base policy caps. If a wiring-caused fire generates a $1.5 million lawsuit but your GL cap is $1 million, the umbrella covers the remaining $500,000. Underlying liability policies must be in place first.

Contractor Tools and Equipment Insurance (Inland Marine): Covers tools and gear in transit between job sites or stored off-site. Standard commercial property policies exclude these items because coverage requires a fixed location — making this the right fit for portable equipment theft and loss.

Surety Bonds: Not insurance. A bond is a three-party guarantee between you, the surety company, and your client or licensing authority — guaranteeing your contractual performance. Required for licensure in some states and for public contract bids. If a claim is paid against the bond, you must repay the surety. Unlike insurance, the protection runs to the client, not to you.

How Much Does Electrical Contractor Insurance Cost?

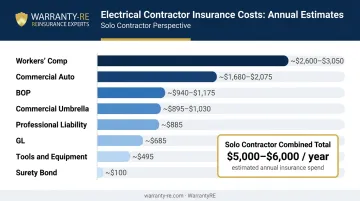

The figures below are marketplace benchmarks from Insureon and TechInsurance — they represent typical midpoints, not guaranteed premiums. Actual costs vary based on payroll, number of vehicles, coverage limits, and claims history.

| Policy Type | Typical Annual Cost |

|---|---|

| General Liability | |

| Business Owner's Policy (BOP) | |

| Workers' Compensation | |

| Commercial Auto (per vehicle) | |

| Tools & Equipment (Inland Marine) | |

| Professional Liability (E&O) | |

| Commercial Umbrella | |

| Surety Bond |

A solo electrician carrying GL, workers' comp, and one commercial vehicle can expect to spend roughly $5,000–$6,000 annually on combined coverage before adding tools or umbrella policies. A multi-crew operation with several vehicles and a larger payroll will pay significantly more.

Understanding Per-Occurrence vs. Aggregate Limits

These terms appear on every GL quote — know what they mean before you start comparing policies:

- Per-occurrence limit — the maximum the insurer pays on any single claim

- Aggregate limit — the maximum paid across all claims in a policy year

A $1M per occurrence / $2M aggregate policy means no single claim is covered above $1 million, and the total payout across the entire policy year won't exceed $2 million. Commercial clients frequently specify minimum per-occurrence requirements before allowing subcontractors on-site.

Pull quotes from at least three carriers — rates can vary by 20–30% for the same coverage, and your claims history, crew size, and service area all influence where you land.

Factors That Affect Your Insurance Premiums

Insurers price based on risk. The factors below directly influence what you'll pay:

- Business size and payroll — more employees increases workers' comp costs; more projects increases GL exposure

- Type of work — high-voltage commercial and industrial installations carry higher premiums than residential service work; electrical is already priced as a higher-risk trade within the construction category

- Number of vehicles — each commercial vehicle adds to your auto premium

- Claims history — a pattern of past claims signals elevated risk and raises future premiums; a clean record can qualify you for preferred pricing over time

- Location — states with higher required coverage minimums raise your baseline; geographic factors like local weather exposure and litigation frequency also affect pricing

- Coverage limits and deductibles — higher limits cost more; higher deductibles lower premiums but increase your out-of-pocket cost when claims occur

Beyond these individual factors, your cumulative claims history feeds into a formal pricing mechanism. NCCI's experience modification factor uses your actual payroll and loss history to adjust your workers' comp premium above or below the manual rate. Businesses with fewer claims pay less than the baseline; those with frequent claims pay more.

How to Choose the Right Coverage for Your Electrical Business

Start With Your Legal Minimums

Before comparing quotes, confirm the insurance requirements for your state and license classification. Contact your state contractor licensing board and identify mandatory coverage types and minimum limits. Meeting the legal floor is a starting point, not a complete program — commercial clients and general contractors will commonly require higher limits or specific endorsements as a contract condition.

Evaluate Providers on Four Criteria

When comparing insurers, look at:

- Policy range — does the carrier offer specialized coverage like E&O, inland marine, and umbrella alongside core policies?

- Financial strength — check AM Best or S&P Global financial strength ratings to confirm the insurer can pay claims

- Customer satisfaction — J.D. Power's Small Commercial Insurance Study and BBB ratings provide useful context for how carriers treat small business clients

- Bundling options — purchasing multiple lines from the same carrier typically costs less than buying each separately

Compare at least two or three quotes before committing. An independent broker who works with multiple carriers can simplify this process, especially for businesses with non-standard risk profiles.

The Gap Standard Insurance Doesn't Cover

Standard insurance protects against accidents, third-party injuries, property damage, and liability. It does not cover the cost to repair or redo your own completed work. GL's workmanship exclusion is clear on this: if a callback requires you to fix a connection, replace a breaker, or redo a panel installation due to your own workmanship, the repair cost is yours.

Electrical contractors who offer labor warranties or service agreements carry this exposure on every job. WarrantyRE helps address it by establishing contractor-owned warranty reinsurance structures:

- A small warranty fee built into each job price flows into a reinsurance account the contractor owns

- When warranty callbacks occur, claims are paid from that account

- Unused funds stay with the contractor rather than going to a third-party warranty provider

- Over time, the account builds into a financial asset the contractor controls

That shift — from unpredictable callback costs to a funded, contractor-owned structure — is what separates a managed warranty program from simply absorbing repair costs out of pocket.

Frequently Asked Questions

What insurance should an electrical contractor have?

The minimum coverage set is general liability, workers' compensation, commercial auto, and either commercial property or a BOP. E&O, commercial umbrella, and tools and equipment insurance add important protection layers depending on the scope and scale of work you perform.

How much is business insurance for electrical contractors?

A small electrical contractor carrying GL, workers' comp, and one commercial vehicle can expect combined annual costs in the range of $5,000–$6,000 based on marketplace benchmarks. Actual premiums vary based on payroll, number of vehicles, chosen limits, and claims history.

Is general liability insurance required for electrical contractors?

General liability is required for electrical contractor licensure in most states and is routinely required by commercial clients before allowing site access. Exact requirements — including minimum limits — vary by state and license classification, so check with your state licensing board directly.

What is the difference between a surety bond and insurance for electricians?

Insurance protects the contractor by covering claim costs when something goes wrong. A surety bond protects the client or licensing authority by guaranteeing your performance — and if a claim is paid against the bond, you must repay the surety company.

Can I bundle multiple insurance policies to save money?

A Business Owner's Policy combines GL and commercial property at a lower cost than purchasing each separately. Many insurers also offer reduced pricing when you purchase multiple policy types through the same carrier. When requesting quotes, ask each carrier about multi-policy discounts.

Do I need workers' compensation if I'm a solo electrician?

Most states exempt sole proprietors with no employees, but some states — including certain construction trade classifications — require it regardless. Even where it's optional, coverage is worth carrying: personal health insurance frequently excludes injuries sustained while working, leaving a coverage gap if you're injured on the job.