Here's the tension most contractors face: the state minimums are low enough to get you licensed but not nearly enough to protect you against the claims Florida's environment actually produces. A slow leak in a multi-unit condo, a post-hurricane callback gone wrong, or a mold problem that surfaces three months after a completed job can all exceed the minimum thresholds quickly.

This guide covers both the legal floor and the practical ceiling — what you must carry, what you should carry, and what it costs.

TL;DR

- State minimums: $100K public liability, $25K property damage, workers' compensation (or valid exemption)

- Practical standard: $1M/$2M GL limits, commercial auto, tools & equipment, umbrella

- Workers' comp trigger: In Florida, hiring even one employee makes workers' compensation mandatory

- Coverage lapse: Contractors must maintain required coverage without interruption or risk license suspension and stop-work orders

What Florida Law Requires for a Plumbing Contractor License

Florida issues plumbing contractor licenses under two tiers:

- Certified Contractor — passes the state exam and can work anywhere in Florida

- Registered Contractor — limited to the local jurisdiction(s) where they hold local registration

Both tiers fall under the Construction Industry Licensing Board (CILB), which operates under the DBPR. Before either license is issued, Florida Statute 489.115 requires applicants to submit an affidavit confirming they've obtained the required liability coverage. Workers' compensation coverage — or a valid exemption — must be in place within 30 days of license issuance.

Insurance sits alongside experience requirements, exam passage, and financial responsibility documentation on the compliance checklist. It's also the item most likely to stall or sink an application when handled incorrectly.

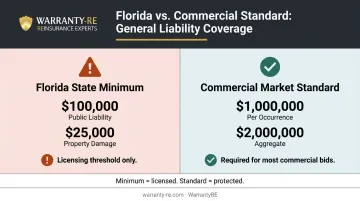

Minimum General Liability Insurance Requirements

Per Florida Administrative Code Rule 61G4-15.003, plumbing contractors (classified outside the general/building contractor category) must maintain:

- $100,000 in public liability (bodily injury) coverage

- $25,000 in property damage liability coverage

These figures satisfy the DBPR licensing requirement. They will not satisfy most general contractors, commercial property managers, or developers. The market standard for commercial work is $1,000,000 per occurrence and $2,000,000 aggregate — meaning contractors who carry only the state minimums will be disqualified from most commercial bids before the conversation even starts.

Workers' Compensation Requirements

Plumbing is a construction trade under Florida law, and Florida Statute 440.02 sets the threshold for construction employers at one or more employees — not four, which is the threshold for non-construction businesses in the state. One part-time helper triggers mandatory coverage.

The sole-proprietor exemption: A self-employed plumber with no employees can apply through the Florida Division of Workers' Compensation for an exemption. The fee is $50 (plus a $1 convenience fee), valid for two years. The moment any employee is hired, coverage becomes mandatory.

The subcontractor trap: If a subcontractor doesn't carry their own workers' comp or a valid exemption, Florida law treats those workers as the contractor's own employees — triggering premium audits, fines, and direct injury liability. Always verify subcontractor certificates before work begins.

Certificate of Insurance Requirements

Each certificate submitted to the DBPR must list the Construction Industry Licensing Board as the certificate holder. This detail is frequently missed and can delay license approval by weeks.

Recommended Coverages Beyond the Florida Minimums

The state minimums establish a legal baseline. Florida's litigation environment, hurricane exposure, and the scale of real-world water damage claims make several additional coverages worth carrying regardless of whether they're mandated.

General Liability: Why Higher Limits Matter in Florida

The case for $1M/$2M limits isn't theoretical. A slow plumbing leak in a multi-unit residential building or high-rise condo can generate water damage claims across several units simultaneously. According to the Insurance Information Institute, water damage and freezing claims averaged $15,400 per claim in the 2019–2023 period — and that's for a single-family homeowner policy. Multiply that across a building with multiple affected units and the $100K state minimum disappears fast.

Completed operations coverage is equally important. This standard GL endorsement extends protection after a job is finished. In Florida's humid climate, a leak or mold problem may not surface for weeks or months after work is complete. Without this endorsement, the contractor may have no coverage when the claim arrives.

Commercial Auto Insurance

Personal auto policies exclude vehicles used for business purposes. A plumber driving to a job site or hauling tools and equipment will have claims denied under a personal policy if an accident occurs. Commercial auto insurance covers that exposure.

Florida's state minimum auto requirements fall well short of what most contractors should carry. The recognized contractor standard is $1M combined single limit (CSL) for liability, a figure supported by both Progressive Commercial and Travelers as a common commercial auto benchmark.

Tools, Equipment, and Additional Policies

Three additional coverages worth carrying:

- Inland marine / tools & equipment — covers theft or damage to tools and equipment in transit or on a job site. General liability does not cover repair or replacement of the contractor's own equipment.

- Commercial umbrella — adds $1M–$5M of liability above primary GL and auto limits, typically in $1M increments. Cost-effective for contractors working commercial or multi-family projects.

- Professional liability (E&O) — covers plumbers providing design, consulting, or system specifications where a professional error leads to a financial loss claim rather than a physical damage claim.

How Much Does Plumber Insurance Cost in Florida?

Florida-specific premium data is limited, but national benchmarks from Insureon's 2025 plumbing insurance cost data provide a reliable starting point. Florida contractors should expect their premiums to run higher than national medians given the state's litigation environment and coastal exposure.

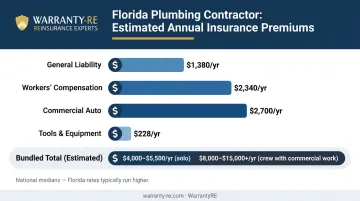

| Coverage | Estimated Annual Premium |

|---|---|

| General Liability ($1M/$2M) | ~$1,380/year ($115/month) |

| Workers' Compensation | ~$2,340/year ($195/month) |

| Commercial Auto (per vehicle) | ~$2,700/year ($225/month) |

| Tools & Equipment | ~$228/year ($19/month) |

| Bundled estimate (solo operator) | ~$4,000–$5,500/year |

| Bundled estimate (crew + commercial work) | $8,000–$15,000+/year |

Figures are national medians. Florida rates typically run higher.

For workers' comp specifically, the Florida Workers' Compensation Joint Underwriting Association lists class code 5183 (Plumbing NOC and Drivers) at a rate of $2.737 per $100 of payroll, with a minimum premium of $2,623 effective January 2026. A contractor with $100,000 in annual payroll should budget at least $2,700–$3,000 for workers' comp alone.

What Drives Premiums Higher in Florida

- High litigation frequency and social inflation

- Hurricane and coastal exposure

- Claims history (a single large water damage claim can affect rates for years)

- Business revenue and payroll size

- Use of uninsured subcontractors

- Commercial and high-rise work vs. residential service plumbing

How to Keep Premiums Manageable

- Bundle policies with one carrier; most insurers discount multi-policy accounts by 5–15%

- Keep a clean claims history — one major claim can reshape renewal pricing for three or more years

- Document a formal safety program; some carriers offer premium credits for written safety protocols

- Use an independent agent who shops multiple carriers rather than a single captive provider

- Classify the business correctly; residential service plumbing and new construction carry different GL codes with meaningfully different rates

Florida-Specific Risks Every Plumbing Contractor Should Know

The Climate Problem

Florida's combination of high humidity, aging plumbing infrastructure, and coastal exposure creates elevated risk for completed-operations claims long after a job is finished. A small leak can escalate into mold remediation costing thousands of dollars — SERVPRO puts the national average mold remediation cost at $2,368, with larger infestations reaching $6,000 or more.

Coastal markets add saltwater corrosion to the equation. Saltwater intrusion accelerates pipe corrosion and increases the likelihood of failures that emerge months after installation. A plumber who did everything correctly on the day of the job may still face a claim when the pipe fails two years later.

Those long-tail exposure risks don't exist in isolation — hurricane season adds a second, more acute layer of pressure.

Hurricane Season (June–November)

NOAA's Atlantic hurricane season runs June 1 through November 30. Post-storm emergency repair demand increases workload and job-site hazards at the same time. Workers are rushing, conditions are dangerous, and the accelerated pace is exactly what generates future liability claims.

Workers' comp and completed-operations coverage are especially important during storm response work. Hurricane Ian alone generated $22.2 billion in insured losses and over 789,000 claims in Florida. The post-storm demand surge that follows major storms puts every contractor on a job site in an elevated-risk position.

Florida's Litigation Environment

Florida has historically generated a disproportionate share of U.S. insurance litigation. A 2024 analysis noted that Florida accounted for 7% of U.S. insurance claims but 76% of lawsuits against insurers , pushing construction insurance costs sharply higher. Florida also shortened its construction defect statute of repose from 10 years to 7 years in 2024 (per Senate Bill 360), but a 7-year window is still a long tail for completed-operations exposure.

For plumbing contractors, adequate limits and an insurer with a strong claims defense track record matter as much as the coverage itself.

Common Insurance Mistakes Florida Plumbing Contractors Should Avoid

Mistake 1: Carrying only the state minimums

The $100K/$25K limits satisfy the DBPR but won't survive a real claim. A single water damage event in a multi-unit residential property can exceed those limits, leaving the contractor personally responsible for the difference. The state minimum is a licensing threshold, not a protection strategy.

Mistake 2: Letting coverage lapse

Florida Administrative Code Rule 61G4-15.003 requires licensees to continuously maintain required coverage. Allowing a policy to cancel or expire is a licensing violation, not just a paperwork problem. Depending on what lapses, the consequences can include:

- License revocation or non-renewal under Florida Statute 489.114 for failure to maintain workers' comp

- Stop-work orders on active projects under Florida Statute 489.127, which treats post-suspension work as unlicensed

- Direct project shutdowns that affect your entire job site, not just the specific violation

A lapsed policy can halt an entire job site overnight.

Mistake 3: Not verifying subcontractor coverage

This is the most commonly underestimated risk. Before any subcontractor steps on a job site, verify that they carry their own general liability and workers' compensation. If they don't, Florida law treats their workers as yours for purposes of workers' comp coverage — exposing the contractor to premium audits, fines, and direct injury liability. Request and retain certificates of insurance for every sub, every job.

Beyond Insurance: Protecting the Financial Side of Your Plumbing Business

Liability insurance protects against claims that come from outside the business. But plumbing contractors face another category of financial exposure that insurance doesn't address: warranty callbacks.

Every water heater replacement, repipe job, or sewer line repair carries an implied labor warranty. When something fails — a bad solder joint, a wax ring that didn't seat, a pinhole leak behind drywall — the contractor rolls a truck, pulls a plumber off paying work, and absorbs the entire cost.

For contractors who offer service agreements or structured warranties, those obligations are often administered by a third party that collects the warranty fees and keeps the underwriting profit.

Contractor-owned warranty reinsurance programs work differently. Instead of paying a third-party administrator to carry that risk, the contractor owns the reinsurance structure. Warranty fees are built into job pricing, flow into a reinsurance account owned by the contractor, and cover claims when they arise. Unused funds stay with the contractor rather than enriching a third-party provider.

WarrantyRE works with plumbing contractors who want to move away from that third-party arrangement and establish their own administrator obligor reinsurance company. The program covers labor warranty obligations across service work, including:

WarrantyRE works with plumbing contractors who want to move away from that third-party arrangement and establish their own administrator obligor reinsurance company. The program covers labor warranty obligations across service work, including:

- Callbacks for leaks and fitting failures

- Fixture installation and wax ring claims

- Pinhole leaks and solder joint issues

- Related service call reimbursements

WarrantyRE handles claims administration, compliance, and program management — so warranty obligations shift from a cost center to a profit-generating part of the business. Contractors keep the underwriting profit that previously went to a third party.

This is a complement to — not a replacement for — the liability coverage discussed throughout this guide. Liability insurance handles claims from the outside; a reinsurance program handles the financial exposure you carry on every job you complete.

Frequently Asked Questions

How much does insurance cost for a plumber in Florida?

A solo Florida plumber with basic general liability typically pays $1,200–$1,800 per year. A small crew carrying workers' compensation, commercial auto, and GL coverage usually budgets $8,000–$15,000+, depending on business size, work type (residential vs. commercial), and claims history.

What kind of insurance covers plumbing work?

The core policies are general liability, workers' compensation, commercial auto, and tools and equipment (inland marine). Florida also sets minimum limits for licensed contractors: $100K in public liability and $25K in property damage, both required for licensure.

What is the minimum insurance required for a Florida plumbing contractor license?

The DBPR requires $100,000 in public liability and $25,000 in property damage, per Rule 61G4-15.003. Workers' compensation coverage (or a valid exemption) must be obtained within 30 days of license issuance, and certificates must list the CILB as the certificate holder.

Do solo plumbers in Florida need workers' compensation?

A self-employed plumber with no employees can apply for a construction industry exemption through the Florida Division of Workers' Compensation ($50 fee, valid two years). That exemption is voided the moment any employee is hired. Because plumbing is classified as a construction trade, the threshold is one employee, not four.

What happens if my insurance lapses while I hold a Florida plumbing contractor license?

Failure to continuously maintain required coverage is a violation of Rule 61G4-15.003 and grounds for license suspension or revocation under Florida Statute 489.114. A suspended license can also trigger stop-work orders on active projects under Florida Statute 489.127.

Does my personal auto insurance cover my plumbing work vehicle?

No. Personal auto policies exclude commercial use. Any accident that occurs while driving to a job site or transporting tools will likely be denied under a personal policy. A commercial auto policy is required to cover business-use vehicles.