Introduction

Most roofing business owners excel at replacing shingles, managing crews, and delivering quality work—but come tax season, they write checks to the IRS that could've been retained and reinvested. The issue isn't tax evasion or aggressive loopholes; it's that most contractors stop at basic deductions and never explore advanced, IRS-recognized strategies designed for profitable businesses.

This guide covers the foundational tax deductions every roofing contractor should use, plus one strategy most owners never consider: owning your own reinsurance company. This structure lets roofing contractors legally reduce taxable income and capture warranty profits that typically flow to third-party providers. The result is a tax-advantaged business asset that builds long-term wealth on the side of your contracting operation.

If you're a profitable roofing business owner paying significant taxes each year, this guide is your starting point for moving from reactive filing to proactive planning.

TLDR

- Section 179, vehicle expenses, and QBI deductions are baseline strategies — and every roofing owner should already be using them

- Business structure (S-Corp vs. C-Corp) dramatically affects tax liability and warrants annual CPA review

- Reinsurance lets roofing contractors replace third-party warranty providers with their own company — capturing both profits and tax advantages

- Premiums paid into your reinsurance company are deductible business expenses that grow tax-advantaged

- Combining standard deductions with reinsurance significantly lowers tax burden while building recurring revenue

Standard Tax Deductions Every Roofing Business Owner Should Be Using

Section 179: Write Off Equipment Immediately

Section 179 allows roofing contractors to immediately expense qualifying equipment purchases rather than depreciating them over multiple years. For 2025, the maximum deduction is $2,500,000, with a phase-out threshold beginning at $4,000,000 in total equipment purchases.

Qualifying property includes:

- Work trucks and trailers

- Roofing equipment and tools

- Computers and software

- Office furniture

- Commercial roofing machinery

SUVs used for business have a $31,300 limit for 2025. Timing matters: purchases must be made and placed in service by December 31 to qualify for that tax year.

Strategic tip: If you're planning major equipment purchases, buy and place the equipment in service before December 31. Taking the full deduction in year one — rather than depreciating it over five to seven years — means more cash stays in your pocket during the growth phase when you're reinvesting heavily.

Source: IRS Publication 946 (2025)

Vehicle Deductions: Track Every Mile

Roofing businesses rely heavily on trucks and vans. The IRS offers two methods to deduct vehicle expenses:

| Method | How It Works |

|---|---|

| Standard mileage rate (2025) | $0.70 per mile for business use |

| Actual expense method | Deduct real costs (gas, maintenance, insurance, depreciation) based on business-use percentage |

Critical requirement: Maintain a same-day mileage log showing date, destination, business purpose, and mileage for each trip. Weekly logs are acceptable. Without documentation, the IRS can disallow the entire deduction during an audit.

Choosing your method: You must select your deduction method in the first year you use the vehicle for business. For leased vehicles, you must use the same method for the entire lease period.

Source: IRS Publication 463 (2025)

Qualified Business Income (QBI) Deduction: Keep 20% More

The QBI deduction allows pass-through entity owners to deduct up to 20% of qualified business income. For 2025, the income thresholds are:

| Filing Status | Threshold | Phase-Out End |

|---|---|---|

| Married Filing Jointly | $394,600 | $494,600 |

| All Other Filers | $197,300 | $247,300 |

Critical advantage for roofing contractors: Unlike law firms, accounting practices, or consulting businesses classified as Specified Service Trade or Businesses (SSTBs), roofing is not an SSTB. This means the QBI deduction is available at all income levels—it never fully phases out, though it becomes subject to W-2 wage and property limitations above the threshold.

Above the threshold, your deduction is limited to the greater of:

- 50% of W-2 wages paid by the business, or

- 25% of W-2 wages plus 2.5% of the unadjusted basis of qualified property

Example: A roofing contractor with $500,000 in QBI, $150,000 in W-2 wages, and $300,000 in qualified property basis:

- 20% of QBI = $100,000 (the ceiling)

- 50% of W-2 wages = $75,000

- 25% of W-2 wages + 2.5% of property basis = $37,500 + $7,500 = $82,500

- Actual deduction = the lesser of $100,000 or $82,500 = $82,500

- Tax savings at a 24% marginal rate: ~$19,800

Source: IRS Instructions for Form 8995-A (2025)

Employee and Subcontractor Costs

All ordinary and necessary labor costs are fully deductible:

- W-2 employee wages (including owner's reasonable salary in S-Corps)

- Payroll taxes (Social Security, Medicare, unemployment)

- Health insurance and benefits

- Training and continuing education

- 1099 subcontractor payments

Critical distinction: The IRS scrutinizes worker classification heavily in construction. Misclassifying employees as 1099 contractors to avoid payroll taxes triggers penalties under IRC Section 3509. The IRS evaluates three factors:

- Do you control how the work is performed? (behavioral control)

- Who provides tools, and how is payment structured? (financial control)

- Are there written contracts, benefits, or an ongoing working relationship? (type of relationship)

When in doubt, file Form SS-8 for an official IRS determination.

Source: IRS Construction Industry Audit Technique Guide

Commonly Missed Deductions

These expenses are fully deductible and often missed:

- Business insurance premiums (liability, workers' comp, commercial auto)

- Marketing and advertising (digital ads, truck wraps, website costs)

- Trade association memberships (NRCA dues, local contractor groups)

- Professional services (CPA fees, attorney consultations)

- Home office deduction (if you have dedicated space used exclusively for business)

- Continuing education and certifications

Choosing the Right Business Structure to Maximize Tax Savings

The Self-Employment Tax Problem

Operating as a sole proprietor or single-member LLC means you pay 15.3% self-employment tax on all net business income—12.4% for Social Security (on income up to $176,100 for 2025) plus 2.9% for Medicare. An additional 0.9% Medicare surtax applies to income above $200,000 (single) or $250,000 (married filing jointly).

Example: A roofing contractor netting $250,000 as a sole proprietor pays approximately $33,000 in self-employment taxes alone before income tax.

Source: IRS Self-Employment Tax

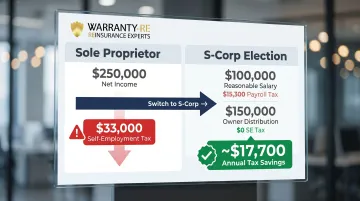

S-Corporation Election: Cut SE Taxes by Up to $17,700

Electing S-Corp status allows you to split income between salary and distributions. You pay payroll tax only on the salary portion; distributions avoid the 15.3% self-employment tax entirely.

Split your income like this:

- Pay yourself a reasonable salary based on industry standards, duties performed, and time devoted

- Take remaining profits as shareholder distributions (not subject to SE tax)

Example: Same $250,000 net income:

- Pay $100,000 reasonable salary → $15,300 in payroll taxes

- Take $150,000 as distributions → $0 additional SE tax

- Tax savings: ~$17,700 annually

The IRS scrutinizes S-Corp salaries closely. Relevant factors include training, responsibilities, time devoted, and comparable industry pay. The IRS also considers whether income comes primarily from your personal labor or from equipment and employees.

Paying yourself $40,000 while taking $200,000 in distributions will trigger an audit.

When to consider S-Corp: Generally beneficial when net income exceeds $60,000-$80,000, depending on your state and administrative costs.

Source: IRS S Corporation Compensation Issues

C-Corporation: Advanced Structures

C-Corporations are taxed at a flat 21% federal rate. This structure makes sense for roofing owners who:

- Reinvest most profits back into the business rather than taking distributions

- Are setting up a captive or reinsurance entity (discussed below)

- Want to maximize retained earnings for long-term growth

Downside: Double taxation—the corporation pays 21% on profits, and shareholders pay tax again on dividends. However, if you're not distributing profits and are building a reinsurance structure, this becomes advantageous.

Review your business structure annually with a CPA. What works at $200,000 in revenue often becomes costly at $2 million—especially once reinsurance structures and retained earnings strategies enter the picture.

Source: IRS Publication 542, Corporations

What Is Reinsurance and How Can Roofers Use It as a Tax Strategy?

The Traditional Warranty Trap

Most roofing contractors either absorb warranty costs directly from operating cash flow or pay third-party warranty providers who retain all profits when claims are low. Either way, the contractor loses: out-of-pocket claim costs or premiums paid with zero return.

Reinsurance flips this model. Instead of paying premiums to a third party, you establish your own reinsurance company that:

Reinsurance Defined for Roofing Contractors

Your reinsurance company:

- Receives warranty premiums built into every roofing job

- Backs labor warranties with an A-rated insurance carrier for compliance

- Pays claims when they arise

- Retains all unearned premiums and underwriting profits

In the admin-obligor model, your reinsurance company acts as the obligor (the responsible party) on the warranty, collects premium income, and only pays for actual claims. A fronting insurer backs the structure for regulatory compliance, meaning your personal exposure is limited to formation costs and accumulated earnings.

How the Structure Works

Step 1: Customer pays for a roofing job with a built-in warranty fee (e.g., $15,000 roof replacement includes a 10-year labor warranty)

Step 2: Warranty premium flows to your reinsurance entity (not a third party)

Step 3: Reinsurance entity is backed by an A-rated fronting insurer for regulatory compliance

Step 4: When claims arise, they're paid from your reinsurance account

Step 5: Unused premiums remain in your reinsurance company as retained profit

From the customer's perspective, the experience is identical to any standard warranty — you simply own the company behind it.

Who Should Consider This

Reinsurance makes sense for roofing companies that:

- Are already offering labor warranties or paying into third-party warranty programs

- Generate sufficient revenue to make setup costs worthwhile (typically mid-to-large operations)

- Want to capture warranty profits instead of giving them to external providers

- Seek tax-advantaged structures for wealth accumulation

WarrantyRE helps roofing contractors set up and manage admin-obligor reinsurance companies, covering legal formations, filings, compliance, tax returns, and claims administration. No prior insurance expertise required.

The Tax Advantages of Owning Your Own Reinsurance Company

Core Tax Advantage: Deductible Business Expense

Premiums paid from your roofing business into your reinsurance entity are deductible business expenses under IRC Section 162. This reduces taxable income at the operating company level—where you earn the most and face the highest tax rates.

Example: A roofing contractor paying $150,000 annually in warranty fees to a third party gets a deduction but zero return. Under reinsurance, that same $150,000 is deductible AND flows into a company you own and control.

Source: Rev. Rul. 2002-89

IRC 831(b) Election: Tax Only Investment Income

Small insurance or reinsurance companies with net written premiums of $2.8 million or less can elect under IRC Section 831(b) to be taxed only on investment income—underwriting income is effectively tax-free.

What this means: Premium dollars flowing into your reinsurance company aren't immediately taxed. Only the investment income earned by investing those reserves faces taxation. This creates meaningful tax deferral—and lets reserves compound inside your company rather than sitting on your tax return.

The IRS does require genuine risk distribution—you can't funnel all premiums from one entity into a captive without meeting risk-shifting and risk-distribution tests established in Rev. Rul. 2002-89 and Rev. Rul. 2002-90. WarrantyRE structures programs to meet these requirements through proper risk pooling.

Source: 26 U.S. Code Section 831(b)

Unearned Premium Reserves and Loss Reserves

Under IRC Section 832(b)(4), insurance companies use an 80% rule for unearned premium reserves—only 80% of the change in reserves is deductible, with the remaining 20% treated as a proxy for acquisition costs already expensed. This spreads premium income recognition over the warranty term, creating significant tax deferral for multi-year warranties.

Loss reserves (estimated unpaid claims) are also deductible but must be discounted to present value under IRC Section 846. This allows your reinsurance company to set aside funds for expected claims while deferring taxation.

Source: 26 U.S. Code Section 832

Investment Income: The Hidden Profit Layer

Premium reserves held in your reinsurance company are invested conservatively—typically in U.S. Treasury bonds or money market funds. All investment income earned on these reserves belongs to your reinsurance company, creating an additional ROI layer that third-party warranty providers were capturing for themselves.

Once your cash balance exceeds 125% of unearned premiums, you gain flexibility to invest excess reserves more aggressively—increasing returns beyond conservative benchmarks.

Third-Party Warranties vs. Reinsurance: The Comparison

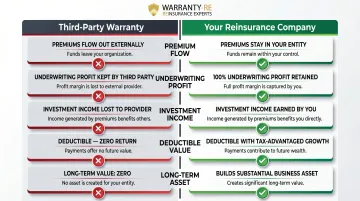

| Factor | Third-Party Warranty | Your Reinsurance Company | |--------|---------------------|--------------------------|\n| Premium destination | Paid to external company | Flows into your entity | | Underwriting profit | Kept by third party | 100% retained by you | | Investment income | Earned by third party | Earned by your company | | Tax treatment | Deductible expense, zero return | Deductible expense, tax-advantaged accumulation | | Long-term value | Zero (permanent cost) | Substantial (business asset) |

Over multiple years, accumulated premium reserves inside your reinsurance company become a real business asset. Roofing contractors use these reserves as a financial cushion, a supplemental retirement vehicle, or capital to reinvest in growth—none of which is possible when premiums flow out to a third party.

Common Tax Mistakes Roofing Contractors Must Avoid

Mixing Personal and Business Finances

Commingling personal and business funds is the #1 audit trigger for contractors. The IRS Construction Industry Audit Technique Guide specifically targets contractors who:

- Charge personal residence improvements to business job costs

- Deliver excess materials from business projects to personal properties

- Use business accounts for personal expenses

When this happens, deductions get disallowed, constructive dividends get assessed, and legal liability protections evaporate. The fix is straightforward: separate business bank accounts and credit cards from day one. Pay yourself a salary or distribution, then spend personal money on personal items.

Source: IRS Construction Industry ATG

Failing to Make Quarterly Estimated Payments

Roofing businesses have uneven, seasonal cash flow, but the IRS requires quarterly estimated tax payments if you expect to owe $1,000 or more after subtracting withholdings and credits.

Payment deadlines: April 15, June 15, September 15, and January 15 of the following year.

Safe harbor rules to avoid penalties:

- Pay at least 90% of current year's tax liability, or

- Pay 100% of prior year's tax (110% if AGI exceeds $150,000)

Penalty: The IRS charges interest on underpayments at the federal short-term rate plus 3 percentage points, compounded quarterly. Even if you file on time and pay in full by April 15, you'll owe penalties for missing quarterly deadlines.

Solution: Work with your CPA to calculate quarterly payments based on projected income, not last year's tax bill if revenue is growing.

Source: IRS Estimated Taxes

Reactive Filing vs. Proactive Planning

Most contractors hire a tax preparer to file returns based on what already happened — and leave real savings on the table. Proactive tax planning means making strategic decisions throughout the year:

- Timing Section 179 purchases before year-end

- Electing S-Corp status before the tax year begins

- Establishing a reinsurance structure during the operating year, not at filing time

- Adjusting estimated payments as revenue fluctuates

Every strategy in this article requires year-round execution. Hiring a CPA who specializes in contractor businesses — not a general tax preparer — is what separates a real tax plan from a year-end surprise.

Frequently Asked Questions

Are roofing expenses tax deductible?

Yes, most roofing business expenses—including materials, labor, equipment, vehicles, insurance, and professional services—are fully tax deductible as ordinary and necessary business expenses under IRC Section 162. Proper record-keeping is essential to claiming them and surviving an audit.

What expenses are 100% write-off?

Under Section 179 and bonus depreciation, qualifying equipment, vehicles, and software may be fully deductible in the purchase year rather than depreciated over time. The 2025 Section 179 limit is $2.5 million, though limits adjust annually—confirm current thresholds with a tax professional before major purchases.

Who is eligible for the $6,000 tax credit?

This typically refers to the Section 25C Energy Efficient Home Improvement Credit (up to $3,200/year) and Section 25D Residential Clean Energy Credit (30% for solar)—both are homeowner credits, not contractor deductions. Roofing contractors can mention them as a customer sales tool. Both credits expire after December 31, 2025.

How do I make my roofing business more profitable?

The fastest levers are tighter job costing, smarter pricing, and capturing revenue you're currently paying to third parties. A reinsurance program lets you retain warranty underwriting profits rather than sending them to external providers—directly improving your bottom line while building a tax-advantaged asset.

What is a good profit margin for a roofing company?

The average roofing contractor achieves approximately 2.8% net profit margin, while strong performers hit 12-15%+ net margins with 35-40% gross margins. Layering reinsurance profits on top of installation revenue can meaningfully increase your effective margin beyond the industry average by capturing warranty underwriting profits that third parties typically retain.

Source: NRCA via CEO Finance Academy

Can roofers make 100k a year?

Yes. The Bureau of Labor Statistics reports the median annual wage for construction managers was $106,980 in May 2024, and many contractor owners earn well beyond that. Smart tax strategies—including reinsurance—help roofing business owners keep more of what they make by reducing tax exposure and adding income streams beyond installation work.

Source: BLS Construction Managers