Introduction

Most roofing contractors offer warranties to win jobs and protect customers — but many don't realize that a significant share of their warranty revenue is flowing directly to someone else. The choice between a third-party warranty company and a reinsurance program determines who keeps those underwriting profits: an outside administrator, or you.

Research from the NAIC confirms that service contract markups often reach 100%. Well-managed warranty programs typically achieve loss ratios of 45–60% — meaning 40–55 cents of every premium dollar may never reach a claims pool when you're working through a third party.

That's real money leaving your business on every job. This guide breaks down how each model works, where they diverge on profitability and control, and which structure makes sense depending on where your roofing business stands today.

TL;DR

- Third-party warranty companies handle administration and claims but keep underwriting profits that belong to the contractor

- Starting with a third-party program is straightforward, but the ongoing cost is high — reinsurance requires more upfront setup and pays off significantly over time

- Warranty reinsurance lets roofing contractors own their warranty program, backed by an A-rated insurer, capturing 100% of those profits

- Reinsurance puts claims control and tax planning in the contractor's hands, turning installations into recurring revenue

- The right choice depends on business size, volume, and long-term growth goals

Roofing Warranty Reinsurance vs. Third-Party Warranty Companies: Quick Comparison

Here's how the two models stack up across the five factors that matter most to roofing contractors.

Profit Structure

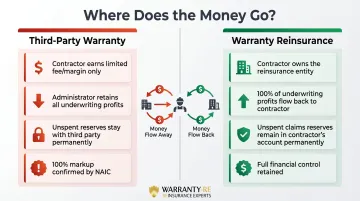

Third-Party Warranty Companies:

Contractors earn a fee or margin on warranty sales, but the third-party administrator retains underwriting profits from unspent claims reserves. Research from the NAIC confirms distributor markups on service contracts often reach 100%, with pricing remaining largely unregulated.

Warranty Reinsurance:

Contractors own the reinsurance entity. All underwriting profits flow directly back to the contractor's company. Any warranty fees not used for claims remain in the contractor's account permanently.

Claims Control

Third-Party Warranty Companies:

The third party adjudicates all claims, which may prioritize cost reduction over customer satisfaction. When a customer calls about a warranty issue, they experience the third party's service standards — not yours.

Warranty Reinsurance:

Contractors control the claims experience through their reinsurance structure, protecting customer relationships and brand reputation. WarrantyRE handles all claims administration while the contractor maintains oversight through ownership of the reinsurance company.

Setup Complexity

Third-Party Warranty Companies:

Low barrier to entry. Sign an agreement and start selling immediately with minimal administrative burden.

Warranty Reinsurance:

Requires formation of an administrator obligor entity, compliance setup, and ongoing administration. Partners like WarrantyRE handle entity formation, legal filings, compliance, claims adjudication, tax returns, and ongoing administration — so the complexity doesn't fall on the contractor.

Long-Term ROI

Third-Party Warranty Companies:

Predictable but limited. The profit ceiling is set by the margin structure of the third-party agreement.

Warranty Reinsurance:

Premiums can be invested for additional ROI. According to WarrantyRE's structure, once your balance sheet cash exceeds 125% of unearned premiums, excess funds may be invested more aggressively. Compounding returns grow as warranty volume increases.

Tax Planning

Third-Party Warranty Companies:

No special tax structure. Warranty income is treated as standard revenue.

Warranty Reinsurance:

Reinsurance entities operating under IRC Section 831(b) may be taxed only on investment income, excluding up to $2.85 million (2025 threshold) in premiums from taxable income. A tax advisor experienced in property and casualty insurance can help you confirm eligibility.

What Are Third-Party Warranty Companies?

Third-party warranty companies act as the administrator and obligor for contractor-sold warranties. They collect premiums from customers and pay out claims when covered work fails. Under the NAIC Service Contracts Model Act, these service contracts are not classified as insurance, though more than 30 states have adopted some form of insurance department oversight.

The contractor sells the warranty at point of sale. The third party collects and holds premiums, pays claims from that reserve, and keeps whatever remains. This leftover — underwriting profit — adds up fast. Industry data from iNube Solutions shows well-managed extended warranty programs achieve loss ratios in the 45–60% range, meaning 40–55% of premiums collected may be retained as underwriting profit, administrative costs, and margin.

For contractors getting started, the appeal is straightforward:

- Low administrative burden

- No entity formation required

- Immediate access to branded warranty products

- No direct financial exposure to claims

The trade-off is control. Because the third party owns the claims relationship and the reserve, contractors lose visibility into profitability and have no say in how claims are handled. A denied or delayed claim reflects on the contractor's reputation — not the third party's.

Use Cases of Third-Party Warranty Companies

That reputation risk matters less when volume is low and infrastructure is limited. Third-party warranty companies fit best for:

- Early-stage roofing companies without established infrastructure

- Contractors in low-volume markets

- Businesses that want branded warranty products without committing internal resources

The model's limitations show up at scale. As install volume and quality records improve, the underwriting profits surrendered to third parties grow with them. The U.S. roofing industry generated approximately $76.4 billion in revenue across 100,000+ businesses, with median company revenue ranging from $500K to $4.9 million. For contractors in that range with strong quality control, that profit leakage becomes a structural cost — one reinsurance alternatives are specifically designed to eliminate.

What Is Roofing Warranty Reinsurance?

Roofing warranty reinsurance is a structure where the contractor establishes their own administrator obligor entity, which administers and backs the warranty, with the risk reinsured by an A-rated insurance carrier. The contractor's company functions as the warranty company — not just a reseller.

Financial mechanics:

Customer premiums are collected into the contractor's reinsurance entity. Claims are paid from that pool. The remaining reserve (underwriting profit) belongs entirely to the contractor. On a $15,000 roof replacement with a 5 or 10-year labor warranty, the warranty fee built into the job price flows into the contractor's reinsurance account — not to an outside company.

Key benefits beyond profit capture:

- Contractors control claims adjudication and the entire customer experience

- Tax planning under IRC Section 831(b): Qualifying small captive insurers pay tax only on investment income, excluding up to $2.85 million in premiums from taxable income

- Warranty fees collected on every job build a pool of customer-funded capital that generates ongoing returns

- Premiums held in trust earn interest or investment returns that stay within the contractor's reinsurance company

The reinsurance structure doesn't leave contractors exposed. An A-rated carrier provides the financial backstop — AM Best defines A-rated insurers as having "Excellent" financial strength and ability to meet ongoing obligations. Customers and contractors gain financial security while contractors capture the upside.

Companies like WarrantyRE handle entity formation, legal filings, compliance, claims adjudication, tax returns (Form 1120PC), and ongoing administration. Contractors own a warranty company without becoming insurance experts.

Use Cases of Roofing Warranty Reinsurance

Warranty reinsurance fits best for:

- Roofing contractors with consistent installation volume

- Businesses with low callback rates and strong quality control

- Growth-oriented contractors who want to convert quality records into recurring profit

Beyond profitability, owning a warranty program increases customer lifetime value, differentiates contractors in competitive markets, and builds a compounding asset in the reinsurance company itself. As Retrofit Magazine notes, offering a 15-plus-year NDL warranty improves chances of securing projects, with warranty scope often becoming "a deciding factor between competing proposals."

Reinsurance vs. Third-Party Warranty: Which Is Better for Your Roofing Business?

Key factors to weigh:

- Higher installation volume means more underwriting profit surrendered to a third party each year

- Contractors with strong quality records and low defect rates lose the most under third-party models

- Early-stage businesses may not yet have the infrastructure to run a reinsurance program

- Reinsurance builds long-term business equity; third-party programs trade that equity for short-term simplicity

Financial tipping point:

The NAIC confirms that service contract pricing is unregulated, and distributor markups routinely reach 100%. With loss ratios in the 45-60% range, roughly 40-55 cents of every warranty premium dollar becomes underwriting profit.

For a roofing contractor doing $1 million in annual installations with a 3% warranty fee built into pricing, that's $30,000 in warranty fees — with $12,000-$16,500 in underwriting profit handed to a third-party provider every year.

That profit gap grows with volume. Beyond the financial case, there's a second reason to weigh which model you choose: what happens when a customer calls.

Customer experience and brand risk:

When customers call about warranty claims, they call the contractor first. Controlling that conversation through a reinsurance-owned claims process protects customer relationships. Third-party programs may prioritize cost reduction over satisfaction, leaving contractors to manage damaged relationships without control over claim outcomes.

Situational recommendations:

Choose a third-party warranty company if:

- You're in the early stages of business

- Annual install volume is below $500,000

- You need to offer warranties immediately while building infrastructure

Choose warranty reinsurance if:

- Your volume and quality record justify capturing underwriting profit

- You want to build a long-term business asset

- You're willing to work with a partner to manage program administration

Transition note:

The two models aren't permanently exclusive. Many contractors start with third-party programs and migrate to reinsurance once their volume and infrastructure support it. The right time to make that move is before the profit you're surrendering becomes too large to ignore.

Conclusion

Third-party warranty companies offer simplicity at the cost of profit and control. Reinsurance programs require more structure but return both to the contractor. For a roofing business focused on long-term growth, that structural difference translates directly into dollars — either kept or surrendered.

Your quality of work generates the warranty revenue — the only question is who keeps it. Start by evaluating your current warranty structure against your growth goals. Then reach out to WarrantyRE to see exactly what a reinsurance program could look like for your business.

Frequently Asked Questions

Are roofing warranties worth it?

Yes — warranties increase close rates and build customer trust. The average close rate for roofing companies hovers around 27%, and warranty differentiation moves that number. What determines long-term value is whether the financial structure behind the warranty is working for your profitability or against it.

Should your roofer be insured?

Yes, but understand the distinction. Liability insurance protects against property damage during installation. Warranty programs protect customers against post-installation defects. Both matter, but they serve distinct purposes and shouldn't be confused.

What should you not say to a roof insurance adjuster?

Avoid speculating on damage causes before a full inspection, admitting fault before reviewing the scope, or agreeing to claim scopes without confirming they cover all code-required work. Adjusters typically look for 25-30% damage to justify full replacement and actively check policy exclusions.

What makes a roof not insurable?

Common factors include roofs over 20 years old, pre-existing damage, non-compliant installation, or materials that don't meet carrier standards. Roof damage accounts for 70-90% of total insured residential catastrophic losses most years — which is why carriers apply strict eligibility criteria.

What is the difference between a third-party warranty company and a reinsurance program for roofing contractors?

A third-party company administers and profits from warranties the contractor sells. A reinsurance program means the contractor owns the warranty entity and captures those profits directly, backed by an A-rated insurer. The contractor controls the structure, claims, and financial outcomes.

Can a small roofing contractor set up their own reinsurance program?

Volume and business maturity matter, but the barrier is lower than most expect. WarrantyRE handles setup, compliance, and administration — so contractors don't need to navigate the structure alone. Call (804) 824-9533 to find out whether your current volume qualifies.