This article walks electrical business owners through both their foundational tax reduction strategies AND the advanced reinsurance approach—so you can make an informed decision about which combination is right for your business. All strategies should be reviewed with a qualified tax professional or advisor familiar with contractor reinsurance structures.

TLDR

- Section 179 expensing, vehicle write-offs, and retirement contributions cut your taxable income fast

- Reinsurance lets you own the entity holding warranty premiums—capturing profit instead of paying third parties

- Premiums paid to your reinsurance company reduce current-year taxable income and build a long-term asset

- Stack reinsurance with an S-corp structure and retirement plans to reduce taxes at multiple levels

- WarrantyRE specializes in helping electrical contractors establish and manage these programs

Standard Tax Deductions Every Electrical Contractor Should Maximize First

Before layering advanced strategies, get the fundamentals locked in. According to the 2024 NFIB Tax Survey, 52% of small business owners are unfamiliar with the 20% qualified business income deduction alone — and that's just one of several high-value categories most contractors underuse. The IRS projects a $696 billion annual tax gap, with underreporting accounting for $539 billion.

Vehicles, Equipment, and Tools

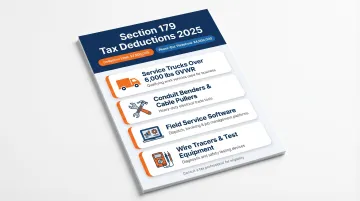

Section 179 Deduction for Electrical Contractors:

The One Big Beautiful Bill Act raised the Section 179 limit from $1,220,000 (2024) to $2,500,000 (2025), with the phase-out threshold jumping to $4,000,000. Qualifying assets include:

- Service trucks (especially those over 6,000 lbs GVWR)

- Conduit benders and cable pullers

- Field service software

- Wire tracers and test equipment

GVWR Threshold Explained:

Vehicle weight matters at purchase. Per IRS Publication 946, vehicles rated at or below 6,000 lbs GVWR face a first-year depreciation cap of $12,200 (2025). Those over 6,000 lbs qualify for full Section 179 expensing up to $31,300 for SUVs—or potentially full cost under bonus depreciation rules.

Bonus Depreciation Restored:

Property acquired after January 19, 2025 qualifies for 100% bonus depreciation under OBBBA, reversing the TCJA phasedown. Purchase a $50,000 work truck after that date and deduct the full amount in year one.

De Minimis Safe Harbor:

Per IRS regulations, items costing $2,500 or less per invoice can be expensed immediately without depreciation schedules. Qualifying items include:

- Multimeters and voltage testers

- Hand tools and power drills

- PPE and safety equipment

- Small diagnostic tools

File the de minimis election annually to take advantage of this immediate write-off.

Licensing, Insurance, and Operating Costs

Deductible operating expenses specific to electrical contractors:

- State license renewals (master, journeyman, apprentice)

- OSHA and NEC continuing education courses (deductible when they maintain or improve skills in your current trade)

- General liability and workers' compensation premiums

- Trade association dues (NECA, IEC) — deductible as business expenses per IRS guidance

- Field service software subscriptions

Self-Employed Health Insurance Deduction:

Self-employed electrical business owners and S-corp shareholders owning more than 2% can deduct 100% of health insurance premiums as an above-the-line adjustment, reducing adjusted gross income directly. Covered insurance types include:

- Medical, dental, and vision premiums

- Qualified long-term care insurance

- Coverage for your spouse and dependents

What Is Contractor Reinsurance and How Does It Work for Electrical Businesses?

Instead of selling service agreements and handing the premium to a third-party warranty company, electrical business owners set up their own reinsurance entity: an administrator obligor structure backed by A-rated insurers. That entity holds the premiums, pays covered claims, and keeps the underwriting profit.

Core Mechanism:

Your customers pay for service agreements or extended warranties. Those premiums flow into your reinsurance company rather than enriching a third-party provider. Claims are still paid, but leftover underwriting profit belongs to you, not an outside insurer.

Before vs. After:

| Third-Party Warranty | Administrator Obligor Reinsurance |

|---|---|

| Contractor sells contract | Contractor sells contract |

| Third party pockets premium | Contractor's entity holds premium |

| Third party retains profit | Contractor retains profit |

| No control over claims | Contractor controls claims experience |

Legal Structure:

The reinsurance company is a separate legal entity, typically structured as an offshore or domestic captive-style vehicle. Key requirements include:

- Liability separation: Protects your contracting business from warranty claims exposure

- IRS compliance: Structure must be properly established and maintained to meet federal tax requirements

- Financial backing: Per the NAIC Service Contracts Model Act, administrator obligor arrangements require contractual liability insurance or equivalent security — WarrantyRE uses A-rated insurer backing to ensure claims are paid regardless of circumstances

Not Just for Big Insurers:

Auto dealers have used this structure in their F&I departments for decades — it's not a new concept, just one that most contractors haven't had access to.

WarrantyRE has worked with over 400 auto dealers since 1994 and now administers the same program for home service contractors, including HVAC, plumbing, and electrical businesses.

The Tax Benefits of Owning Your Own Reinsurance Company

Premium Deductibility

When an electrical contractor's business pays premiums to its own reinsurance company, the IRS treats those premiums as a business expense—potentially reducing the operating company's taxable income, similar to any other insurance expenditure.

Critical requirement: The arrangement must qualify as "insurance" for federal tax purposes. Per IRS Revenue Ruling 2002-89, this requires genuine risk shifting (you transfer economic risk to the insurer) and risk distribution (the insurer pools sufficiently large independent exposures). When structured properly with third-party customer risks pooled together, contractor warranty programs meet these tests.

Work with a specialist to ensure proper setup—improper structures can trigger IRS scrutiny under Notice 2016-66.

Tax-Deferred Reserve Accumulation

Insurance companies are taxed under IRC Section 832, which permits the deduction of loss reserves (estimated future losses) from gross income. Standard businesses can generally only deduct losses when fixed and paid—a meaningful structural disadvantage.

Reserves held in the reinsurance entity to cover future claims can grow on a tax-deferred basis. Investment returns on those reserves aren't subject to current taxation the way ordinary business income would be, creating a long-term compounding effect that standard deductions cannot replicate.

IRC Section 831(b) offers an additional advantage: qualifying small insurance companies with annual net written premiums at or below approximately $2.8 million may elect to be taxed only on investment income, effectively excluding premium income from federal taxation entirely.

Underwriting Profit as a Business Asset

When claims are lower than premiums collected—which is often the case when the contractor controls installation quality—the remaining reserve balance belongs to your reinsurance company, not an outside insurer. That profit becomes a long-term asset rather than disappearing into a third party's margin.

Third-party warranty companies wouldn't stay in business if they weren't profitable. By owning the reinsurance entity, you capture that margin.

Control Over Claims Experience

Because you own the reinsurance entity, you have direct incentive to reduce callbacks and warranty claims through better installation quality. Better installation quality means fewer claims, which directly increases the underwriting profit retained in your own company. Few tax strategies also improve the work you're doing on the ground.

Interaction with Overall Tax Picture

Paying premiums to your reinsurance entity reduces taxable income at the operating company level, which can produce several downstream benefits:

- Brings operating income into a lower tax bracket

- Reduces self-employment or pass-through tax exposure

- Shifts profit into a tax-advantaged structure that compounds over time

Consult a tax advisor familiar with contractor reinsurance to model the impact on your specific entity structure and income levels.

Combining Reinsurance with Business Structure and Retirement Planning

The most tax-efficient approach for established electrical contractors combines a reinsurance program with the right business entity structure—typically an S-corp for the operating company paired with a properly structured reinsurance entity.

S-Corp + Reinsurance Synergy:

Two tax advantages work together here:

- Distributions from an S-corp are not subject to self-employment tax (unlike sole proprietor or partnership income)

- Premium payments from your S-corp to your reinsurance entity reduce the S-corp's taxable income, potentially lowering both income tax and the required reasonable compensation base

Critical requirement: The IRS requires S-corps to pay shareholder-employees reasonable compensation subject to employment taxes. Courts have repeatedly recharacterized distributions as wages when salaries are unreasonably low. Your salary-vs.-distribution split must be defensible.

Retirement Planning Layer:

While SEP-IRA and Solo 401(k) contributions reduce current-year taxable income up to contribution limits—$70,000 for 2025 under 415(c), or $81,250 with the ages 60-63 enhanced catch-up—the reinsurance entity creates an additional long-term asset outside of retirement account contribution limits. For high-earning contractors, this means a second wealth-building vehicle that retirement accounts alone can't provide.

Coordination is Essential:

Managing an S-corp, a reinsurance entity, and retirement accounts simultaneously creates meaningful complexity. Each layer interacts with the others—premium deductions affect compensation calculations, which affect retirement contribution limits. Electrical contractors who implement this structure typically work with an advisor experienced in contractor reinsurance, alongside their CPA, to keep everything aligned.

How WarrantyRE Helps Electrical Contractors Build a Reinsurance Program

WarrantyRE (operating alongside DealerRE) has been setting up and managing administrator obligor reinsurance companies for business owners since 1994. Originally focused on the automotive dealer space, WarrantyRE now serves home service contractors — including electrical businesses.

Full-Service Administration:

WarrantyRE handles company setup, legal filings, tax returns, claims adjudication, compliance, and ongoing performance reporting, managing the administrative and regulatory side of your program end to end. Services include:

- Company formation and legal setup

- All regulatory filings and renewals

- Staff training (online and in-person)

- Claims administration from first call to resolution

- Monthly financial statements

- Annual tax return preparation by insurance tax experts

The Practical Process:

WarrantyRE conducts a business analysis to evaluate whether a reinsurance program makes sense for your volume and warranty exposure. Once established, the program is designed so you capture 100% of the underwriting profit that previously went to a third-party warranty provider—putting that money back into your business as recurring revenue and a structured tax planning asset.

Ready to see what a reinsurance program could look like for your electrical business? Call WarrantyRE at (804) 824-9533 to schedule a complimentary business analysis.

Frequently Asked Questions

What can an electrician write off on taxes?

Main categories include tools and equipment (via Section 179 expensing), vehicles, insurance premiums, licensing and continuing education costs, employee wages and benefits, marketing expenses, and retirement contributions. Reinsurance premium payments to a contractor-owned entity can also be a significant deduction when properly structured.

What is the $75 rule in the IRS?

Per IRS Publication 463, the IRS generally requires a receipt for any business expense of $75 or more (the threshold applies to certain expense documentation requirements under accountable plan rules). Keep receipts for every expense regardless of amount — the $75 threshold is a floor, not a filing suggestion.

What is the $1,000 instant tax deduction?

There is no universal "$1,000 instant deduction." The de minimis safe harbor allows electrical contractors to immediately expense individual business items costing $2,500 or less (instead of depreciating them), and Section 179 allows full first-year expensing of qualifying equipment purchases well above that threshold—up to $2,500,000 for 2025.

How does reinsurance reduce taxes for electrical contractors?

Premium payments from the operating company to a contractor-owned reinsurance entity reduce taxable income at the operating level. Reserves grow tax-deferred, and underwriting profit stays with the contractor—rather than flowing out as ordinary business income to a third-party provider.

Can electrical contractors deduct warranty program costs?

Yes. Premiums paid to a properly structured contractor-owned reinsurance company are deductible business expenses—turning a warranty program from a cost center into a source of retained underwriting profit.