Contractor-owned reinsurance companies flip this equation. Instead of paying third-party warranty companies for coverage you're already standing behind with your own crews, you establish your own IRS-recognized reinsurance entity. Premiums from customers flow into an account you control, claims are paid from reserves you own, and profits stay inside your business—all within a tax-advantaged structure that's been helping contractors build wealth since the early 1990s. Yet most contractors in HVAC, roofing, plumbing, and electrical trades have never even heard this option exists.

This article breaks down exactly what contractor reinsurance is, how the tax savings mechanism works, the specific financial benefits available, and what it takes to set up your structure the right way.

TLDR

- Contractors who own their reinsurance company deduct warranty premiums as ordinary business expenses.

- Underwriting profits stay in-house rather than flowing to a third-party warranty provider.

- Reserves and investment income grow inside the entity and are taxed only when distributed.

- This structure is backed by state regulation and IRS Code 831(b)—not a loophole when properly administered.

- Compliance is non-negotiable: real insurable risk, actuarially sound pricing, and ongoing regulatory filings are required.

What Is a Contractor-Owned Reinsurance Company?

A contractor-owned reinsurance company is a business entity you establish and own 100% that backs the warranties you sell to your customers. Instead of paying all warranty premiums to a third-party provider, those customer fees flow into your own reinsurance account.

Here's how the flow works:

- You sell a labor warranty or service agreement to a customer (built into your job pricing)

- The warranty fee flows into your reinsurance company's reserve account

- When warranty claims arise, they're paid from those customer-funded reserves

- Underwriting profits—the difference between premiums collected and claims paid—stay with you, not a third party

This is fundamentally different from simply self-insuring. The administrator obligor model gives your structure regulatory standing and consumer protection without requiring you to become a licensed insurer yourself.

Your reinsurance company is backed by an A-rated admitted insurance carrier that provides the ultimate financial guarantee if claims exceed your reserves. That backing is what separates this structure from informal self-insurance arrangements — and what makes it viable for contractors in any trade.

Who This Applies To

This structure works for home service contractors who already sell—or could sell—warranties, service agreements, or maintenance contracts:

- HVAC contractors offering labor warranties on system installations

- Roofers backing installation work with multi-year labor coverage

- Plumbers selling service agreements on water heaters, repiping, or fixture installations

- Electricians offering labor warranties on panel upgrades, rewiring, and electrical installations

- General contractors providing warranty coverage on remodeling and construction projects

The key requirement: your warranties must cover genuine, uncertain risks—equipment failure, labor callbacks, parts replacement—for the arrangement to qualify as insurance for tax purposes under IRS standards established in Helvering v. LeGierse.

How Contractor Reinsurance Reduces Your Tax Bill

The tax reduction comes from four interconnected mechanisms that work together to defer taxes and build wealth inside your business.

1. Premium Payments Are Deductible Business Expenses

When your operating company pays warranty premiums to your affiliated reinsurance company, those payments are fully deductible as ordinary and necessary business expenses in the year paid. This immediately reduces your taxable business income.

Example: If your HVAC company collects $100,000 in warranty fees and contributes those premiums to your reinsurance entity, that $100,000 is deducted from your operating company's taxable income, lowering your tax bill right now.

2. Reserves Accumulate Tax-Deferred

Your reinsurance company holds reserves for future claims. Under IRC Section 832, insurance companies can deduct losses incurred and the increase in unpaid loss reserves. This means:

- Premiums collected today are not treated as taxable income

- Reserves grow inside the entity without immediate taxation

- Funds are taxed only when distributed to you—not when collected from customers

That's tax deferral working in your favor: deduct premiums now, pay tax on profits later — often years down the road, potentially at a lower effective rate or in a more favorable tax year.

3. Investment Income Compounds Inside the Entity

Reserves held in your reinsurance company are invested in conservative investments like government bonds. All investment returns generated on those reserves belong to your entity and compound within it. Those returns are not immediately taxable at your operating company level.

For a contractor generating $100,000 in annual premiums, even modest investment returns inside the entity compound year over year — wealth that disappears entirely when you write a check to a third-party warranty provider instead.

4. Legitimate Risk Transfer Qualifies for Insurance Treatment

Pure self-insurance doesn't get you these tax benefits because there's no real risk transfer — you're just setting money aside. The administrator obligor structure achieves genuine risk transfer by involving an independent A-rated insurer that assumes ultimate liability. This is the IRS's core requirement for insurance tax treatment, as clarified in Revenue Ruling 2002-89 — and it's what separates a compliant reinsurance program from a tax shelter that won't survive scrutiny.

Key Tax Advantages: Breaking Down the Benefits

Each of the four advantages below works independently—but together, they create a compounding tax and wealth-building effect that no third-party warranty arrangement can replicate.

Deductible Premium Payments

Your operating business writes off warranty premiums paid to your affiliated reinsurance company as ordinary and necessary expenses—directly reducing taxable business income each year premiums are paid. The deduction is identical to what you'd get paying a third party. The difference: now that money stays in your ecosystem.

Reserve Accumulation Without Immediate Taxation

Funds held in claims reserves aren't treated as current income. They're set aside for anticipated future claims, allowing capital to grow tax-deferred inside the entity rather than being taxed in the year received. This tax-deferred growth treatment—codified under Subchapter L of the Internal Revenue Code—is what separates insurance company taxation from standard business taxation.

Recapturing Underwriting Profits

When actual claims come in lower than premiums collected—meaning your warranties perform well—the surplus is **underwriting profit** that stays within your reinsurance company instead of enriching a third party.

Industry data suggests that well-administered warranty programs in the home service space typically retain 10% to 20% of premiums as underwriting profit after claims and expenses, according to warranty industry analysis. The exact margin varies based on warranty terms, claim frequency, and operational quality—but that margin belongs to your company, not a third-party provider's bottom line.

Investment Income Inside the Entity

Premium reserves can be invested. Returns generated inside the entity aren't immediately taxable, allowing those gains to compound before distribution. Over a 10- or 20-year horizon, that compounding effect can meaningfully accelerate total returns in ways a standard business account simply can't match.

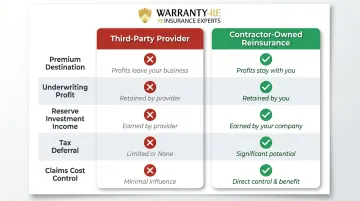

Reinsurance vs. Paying a Third-Party Warranty Provider: The Financial Difference

Most contractors pay a third-party warranty company to back their labor warranties. In that model:

- Premium dollars leave your business and go to the warranty company

- You get no share of underwriting profits if claims are lower than expected

- You earn no investment income on the reserves held

- You receive no tax deferral on the funds collected

- The third party captures all of those benefits

Now compare that to owning your own reinsurance company:

| Financial Component | Third-Party Provider | Contractor-Owned Reinsurance |

|---|---|---|

| Premium destination | Leaves your business | Flows into your reinsurance account |

| Underwriting profit | Kept by third party | Stays with you |

| Reserve investment income | Kept by third party | Belongs to your entity |

| Tax deferral | None | Yes—reserves grow tax-deferred |

| Claims cost control | You pay for callbacks anyway | Covered from customer-funded reserves |

The tax reduction comes from ownership. When you own the reinsurance company, you own the reserves, the underwriting profits, and the investment income those reserves generate. The tax deferral isn't a separate strategy layered on top—it's built into how the structure works.

How to Set Up Your Contractor Reinsurance Company

Setting up a contractor reinsurance company is not a DIY project. It requires careful structuring and professional administration to ensure compliance and maximize benefits.

Key steps include:

- Select the right legal entity structure for your reinsurance company (typically a captive insurance entity eligible for IRC 831(b) treatment)

- Establish the reinsurance agreement with a licensed fronting insurer that provides A-rated backing

- Set actuarially sound premium rates based on your warranty terms, claim history, and risk exposure

- File compliance documents with applicable state insurance regulators and the IRS

- Implement operational procedures for premium collection, claims handling, and financial reporting

Each of these steps involves regulatory, actuarial, and legal coordination that most contractors aren't equipped to handle alone. WarrantyRE has been guiding contractors and auto dealers through this process since 1994, with full-service program administration that covers:

- Entity formation and regulatory filings

- Compliance management and tax return preparation

- Claims adjudication and administration

- Ongoing bookkeeping and financial reporting

- Owner advisory meetings to review performance

Your reinsurance company must be built around genuine warranty products you already sell or plan to sell. The structure exists to support a real warranty program—not as a standalone tax shelter. WarrantyRE partners with A-rated insurance carriers to provide the fronting insurer backing your program requires, so your reinsurance entity operates on solid regulatory and financial footing from day one.