Introduction

Most roofing contractors treat labor warranties as a necessary cost of doing business — a liability attached to every job. Every time a claim comes in, you're dispatching crews, burning fuel, and losing productive time, all while covering costs with no return. That same warranty structure can be redesigned to generate profit instead.

By controlling how warranty obligations are funded, managed, and backed, roofing contractors can stop subsidizing third-party warranty providers and start keeping that money in-house. The shift isn't theoretical — it's a structural change that contractors nationwide are already using to build recurring revenue from work they've already completed.

TLDR

- Labor warranties drain cash flow when callbacks hit operating accounts with no dedicated reserve to cover them

- Setting aside 1–2% of each job's revenue into a warranty reserve turns callbacks into a funded, predictable cost

- A strong labor warranty becomes a sales differentiator that justifies premium pricing and closes more jobs

- The highest-margin model is owning your own warranty reinsurance company, recapturing profits that currently go to third-party providers

Why Most Roofing Labor Warranties Drain Profits Instead of Building Them

The default model for most roofing contractors is informal and reactive. When a warranty callback happens — a leak, flashing issue, or improper nail pattern — the crew goes back out and the cost comes straight out of the original job's margin. This happens weeks or months after the job closed and the money was spent elsewhere. As Chris Margarites noted in Roofing Contractor Magazine, most contractors treat warranty work as "a necessary evil to support your installation work," absorbing costs from operating cash flow rather than maintaining a formal reserve.

Without a funded reserve, a single bad batch of jobs or a streak of weather-related callbacks can wipe out margin from dozens of profitable installs. GAF's contractor training content estimates that poorly trained crews experience callback rates of 10–20% of jobs, while well-trained crews keep that number at 1–3%.

At either end of that range, real money is leaving your business.

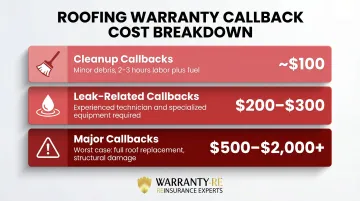

The hidden cost of "free" labor warranties:

- Cleanup-related callbacks: approximately $100 (2–3 hours labor, fuel, truck expense, lost productive time)

- Leak-related callbacks: $200–$300 (experienced technician plus equipment)

- Major callbacks: $500–$2,000+ (worst case involves full roof replacement)

These figures from GAF reflect direct costs only. They don't account for reputation damage, lost referrals, or the opportunity cost of pulling your best crews off revenue-generating work. Most contractors who offer labor warranties are self-insuring in the least efficient way possible — no reserve structure, no tax advantage, and no mechanism to turn that exposure into profit.

The Warranty Reserve: Your First Step Toward Profitability

A warranty reserve is a dedicated fund, separate from operating accounts, funded by a fixed percentage (typically 1–2%) of every new installation job's revenue. The deposit is made at the time of invoicing, not when a claim happens. That timing distinction is what gives the model its financial leverage.

The tax advantage matters: the reserve deposit is treated as a cost charged against the job, so it's funded with pre-tax dollars. You're pre-paying for future warranty work before it hits taxable income. Tax treatment varies by accounting method and entity structure, so confirm the specifics with your CPA.

How the Reserve Changes Your Service Department

Instead of warranty callbacks being unpaid burdens, the service team invoices the reserve at normal labor rates, making every warranty call a billable event internally. This transforms your service department from a cost center into a profit center. As Margarites explained in his Roofing Contractor Magazine article, this structural logic is an established best practice in the industry.

The "leftover money" dynamic:

In years with low warranty claims, the reserve accumulates. That surplus can be returned to the bottom line as taxable income — profit from jobs that performed better than expected.

One contractor who maintained this discipline throughout his career had accumulated over $1 million in his reserve by the time he sold his business.

Secondary Benefits of a Funded Reserve

- Protects business valuation: Buyers conducting due diligence request historical callback volume and reserve practices. Wexford Insurance notes that a funded reserve eliminates warranty holdbacks at time of sale.

- Signals financial discipline: Demonstrates credibility to lenders, partners, and prospective buyers — without requiring a pitch.

- Surfaces quality problems early: If reserve spending spikes on certain crews or job types, you have a specific, data-driven reason to address training or process gaps immediately.

Making Labor Warranties a Sales Tool That Closes More Jobs

In a market where most contractors offer 1–2 years of labor coverage, a contractor who confidently offers 5–10 years of backed labor warranty stands apart. This matters especially with homeowners who've been burned before by companies that disappear after installation.

A funded labor warranty changes the sales conversation. Instead of being a footnote, it becomes proof of financial stability and long-term accountability — the kind of proof homeowners actually weigh at the point of decision.

Roofing Contractor Magazine's 2025 Homeowner Survey found that 67% of homeowners cited "better communication" as the top factor when choosing between contractors, and 88% use referrals to measure trust. A longer, backed warranty addresses both — it signals transparency upfront and gives past customers something concrete to reference.

Premium Pricing Justified by Stronger Warranties

Longer warranty terms allow for premium pricing. The cost of funding the reserve (1–2% of job revenue) is far less than the price premium a strong warranty can command. Contractors can build reserve funding directly into their pricing model without reducing margin — the reserve creates margin by preventing future losses and generating surplus in low-claim years.

That surplus doesn't disappear — it accumulates inside the contractor's own reinsurance structure. The financial mechanics work in three directions:

- Reserve contributions are priced into each job, so funding costs nothing out of pocket

- Low-claim years generate underwriting profit that stays with the contractor

- Premium pricing becomes defensible because the warranty backing is real and documented

The Next Level: Owning Your Own Warranty Reinsurance Company

The real margin loss occurs when roofing contractors use third-party warranty administrators or extended warranty providers, the underwriting profit — the money left over after claims are paid — stays with the provider, not the contractor. Well-managed warranty programs achieve loss ratios of 45–60%, meaning 40–55% of collected premiums are available for expenses and profit after claims are paid. Right now, that 40–55% margin is going to someone else.

The Reinsurance Model

Contractors can establish their own administrator obligor reinsurance company, funded by warranty premiums collected from customers and backed by A-rated insurers. This structure allows the contractor to keep the underwriting profit themselves instead of surrendering it to a third party.

Two additional advantages compound the profit picture:

- Investment income: Premiums held in the reinsurance company can be invested, generating returns on funds that would otherwise sit in a third-party's account. Single-parent captive insurance companies — the closest analog to contractor-owned reinsurance — achieved average underwriting profits of nearly 20% of premium and average ROE of 13%, per Milliman's 2021 analysis.

- Tax efficiency: Profits within a properly structured reinsurance entity can receive favorable tax treatment. A tax advisor can clarify specifics, as benefits vary by entity structure and domicile.

WarrantyRE's Role

Companies like WarrantyRE specialize in helping roofing contractors set up and manage their own administrator obligor reinsurance companies. Their full-service model covers every operational layer, so contractors aren't trading one administrative headache for another:

- Company formation and regulatory compliance

- Claims adjudication and performance reporting

- Legal filings, tax returns, and annual renewals

The result: contractors capture the underwriting profits their third-party providers currently keep, without adding staff or complexity to their business.

Building Your Warranty Profit System: Practical Steps to Get Started

Before you can build a warranty profit system, you need a baseline. Calculate your current annual callback volume, average cost per callback, and total warranty-related labor spend per year. That total labor spend becomes your funding target for the reserve.

From there, the implementation is straightforward:

- Set your reserve at 1–2% of install revenue to start

- Open a dedicated account so warranty funds stay separate from operating cash

- Bill the reserve internally — your service team invoices it for warranty work at standard rates

- Review quarterly to compare reserve balance against actual spend and catch trends early

From here, the path scales naturally. Start with a warranty reserve, refine your pricing to embed reserve funding, then evaluate whether your warranty volume and margin justify moving to a reinsurance structure. Larger contractors doing consistent volume typically see the strongest returns from owning their reinsurance entity — but there's no minimum volume requirement to get started with WarrantyRE.

Frequently Asked Questions

Are roof warranties worth it?

Labor warranties are worth it when they're properly funded. An unfunded warranty is a liability that drains cash flow. A reserve-backed or reinsurance-backed warranty generates profit on low-claim years and protects margin on high-claim ones.

How much should a roofing contractor set aside for a warranty reserve?

The typical starting range is 1–2% of each installation job's gross revenue, deposited at time of invoicing. Adjust the exact percentage based on your historical callback frequency and average cost per warranty visit.

What is the difference between a warranty reserve and a warranty reinsurance program?

A warranty reserve is an internal fund you manage yourself. A reinsurance program means forming a separate company that collects premiums, is backed by A-rated insurers, and returns underwriting profit and investment income to you.

Can a roofing contractor actually make money from labor warranties?

Yes, through two mechanisms. Reserve surpluses in low-claim years flow back as profit. In a reinsurance structure, the underwriting margin that would otherwise go to a third-party provider stays with your own company.

What can void a roofing labor warranty?

Common triggers include improper attic ventilation, unauthorized repairs by unlicensed contractors, failure to maintain gutters and flashing, and modifications to the roof system without notifying the original contractor.

How does a roofing contractor set up their own warranty reinsurance company?

A reinsurance specialist like WarrantyRE handles the process — forming the administrator obligor entity, securing A-rated insurer backing, and managing claims adjudication, compliance, and all administrative requirements on your behalf.