According to CFMA benchmark data, the median net profit before tax for roofing contractors (NAICS 238160) was 3.0% in fiscal year 2022. That's not a typo. For every $1 million in revenue, the average contractor kept $30,000 before taxes.

This article breaks down where roofing profit actually goes, which operational levers move the needle fastest, and how a warranty reinsurance structure can convert a cost center into ongoing income — a model most competitors haven't discovered yet.

TL;DR

- Roofing median net profit runs around 3–6% industry-wide — most contractors are leaving significant money behind

- Top margin killers: material waste, commissions tied to revenue (not gross profit), and unmanaged overhead

- Repair and maintenance jobs typically carry higher margin rates than full replacements, despite lower ticket sizes

- A contractor-owned reinsurance structure converts warranties from a cost line into a funded profit center

What Roofing Profit Margins Really Look Like

Gross vs. Net: Where the Gap Lives

CFMA's fiscal year 2022 data for roofing contractors (NAICS 238160) puts median gross profit at 28% and median net profit before tax at 3%. That 25-point gap is where the business runs — or bleeds out.

Gross profit covers direct job costs: materials, labor, and commissions. Everything else — rent, insurance, vehicles, software, admin, marketing — comes out of that remaining margin before you see a dollar of net income.

The NRCA/Sageworks data shows roofing contractors averaged 6% net margin in 2018, up from 4.2% in 2014. The trajectory is positive, but there's still a wide gap between what well-run operations achieve and what most contractors actually take home.

Why Roofing Margins Run Structurally Thin

Roofing is materials-heavy in a way HVAC or plumbing simply isn't. In service trades, the bulk of revenue comes from labor and diagnostics — materials are a relatively small share. In roofing, materials can consume 40–50% of every job dollar before a single overhead expense is counted.

Three cost pressures squeeze the margin from both sides:

- Materials — high cost-of-goods relative to other trades, with limited ability to mark up competitively

- Labor — increased for seven in ten contractors since January 2023, with 42% of those seeing increases of 11–20%, per Roofing Contractor's 2024 State of the Industry report

- Overhead — fixed costs that don't scale down when job volume dips

That combination leaves little room for pricing mistakes or inefficiency.

Profit Margins Vary Significantly by Job Type

A blended margin number hides the real story. Different job types carry meaningfully different margin profiles:

| Job Type | Margin Characteristics |

|---|---|

| Repair / Maintenance | Lower ticket, minimal material cost — often highest margin rate |

| Retail Re-Roof | Mid-range margin, depends heavily on pricing discipline |

| Storm / Insurance | High volume potential, but supplement capture critical to margin |

| Commercial | Competitively bid, typically lower gross margin percentage |

Repair and maintenance work stands out in that table. A service call has almost no material cost and no sales commission — the revenue is nearly all labor. Contractors who build repair programs into their mix improve blended profitability without adding overhead proportionally. Preventative maintenance agreements take that further, turning one-time customers into predictable, recurring revenue.

The Hidden Costs Killing Your Roofing Margins

Material Waste and Pricing Discipline

With 49% of contractors citing increased material costs as a chief concern in 2024, material buying has never been more consequential. Materials represent the single largest direct cost category in roofing — and unlike labor, where productivity improvements take time, pricing discipline shows up in the next invoice.

Even marginal improvements in ordering accuracy, waste reduction, and supplier negotiation drop directly to net income. There's no overhead allocation to dilute the effect.

Commission Structures That Destroy Pricing

Paying sales commissions on revenue — not gross profit — creates a predictable incentive problem. A salesperson who can close faster by discounting 5% loses nothing personally. The contractor absorbs the entire margin hit.

Shifting commissions to gross-profit-based structures changes the calculation for sales staff immediately. Discounting a job reduces their check, not just yours. Blended margins often improve within the first selling season after making this change.

Supplement Leakage on Insurance Work

The US roof repair and replacement claim cost value reached nearly $31 billion in 2024, up approximately 30% since 2022. Insurance work is a significant revenue channel — but many contractors accept the first adjuster estimate without pursuing legitimate supplemental line items:

- Code upgrades and enhanced ventilation requirements

- Drip edge, ice and water shield, and pipe boots

- Additional labor for code-mandated tear-off or disposal

Every line item left off the scope is revenue the contractor performed work for but never collected.

Callbacks and Overhead Creep

Callbacks generate no revenue: just time and materials out the door. Tracking callback rates by crew turns a frustrating operational problem into a data problem with a solution. If one crew accounts for a disproportionate share of returns, that's a training issue. Addressed early, the improvement compounds across a full season.

Overhead creep works more slowly but hits just as hard. Costs that made sense at $2M in revenue (software subscriptions, additional admin, a larger facility) don't automatically scale down if growth stalls. A line-by-line overhead review whenever revenue plateaus is more valuable than chasing additional jobs to cover costs that should have been cut.

How to Price for Maximum Profit

A Roofing Contractor pricing exercise found that 90% of roofers underbid a 33-square job versus professional benchmarks — and 33% bid below the $12,000 stated hard cost of materials and labor alone. At that point, you're not competing on price — you're paying to do the work.

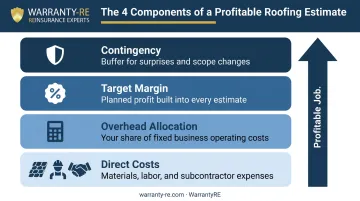

A profitable estimate has a clear structure:

- Direct costs — materials, labor, subcontractor costs, equipment

- Overhead allocation — assign a proportional share of fixed costs to every job

- Target margin — decide in advance what net margin this job type needs to carry

- Contingency — especially on insurance work where scope can shift

Pricing must recover overhead, not just cover direct costs. If your estimate stops at materials and labor, every job is subsidizing your fixed costs without you realizing it.

Warranties as a Pricing Premium

A documented, well-funded labor warranty gives homeowners a concrete reason to choose you over a lower bid. Warranties, licensing, and material quality are consistently grouped as essential factors in homeowner decision-making, according to Roofing Contractor's 2026 homeowner survey. A longer warranty term with real backing behind it — not just a verbal promise — supports higher pricing on retail jobs without reducing close rates.

Pricing that reflects your warranty's real value is one lever. Timing is another.

Seasonal Pricing Strategy

Roofing revenue swings hard between seasons, and pricing strategy needs to move with it. Tracking job profitability by month reveals when the market will bear higher prices and when reducing overhead matters more than chasing volume.

A few principles that hold across most markets:

- Peak season: Support premium pricing — demand justifies it

- Slow season: Protect margin first; discounting to keep crews busy often costs more than it recovers

- Year-round: Monitor actual job profitability monthly, not just revenue

Operational Levers That Directly Boost Net Margin

Crew Productivity and Tracking

The difference between a high-output crew and an underperforming one, multiplied across a full season, creates substantial margin variation. Tracking squares installed per day per crew — and cost per square installed — provides the data needed to address performance gaps before they become costly.

With 54% of the typical roofing contractor workforce made up of full-time employees and 29% subcontractors (per Roofing Contractor's 2026 State of the Industry), the labor model itself is a lever. Subcontractor costs are often more flexible to adjust than in-house labor.

Supplier Relationships and Volume Negotiation

Roofing companies that skip renegotiating supplier pricing as volume grows are handing margin back to the distributor. When approaching suppliers at volume milestones, negotiate beyond unit price:

- Delivery reliability — fewer delays, fewer crew idle days

- Returns policy — reduces the cost of over-ordering

- Priority allocation — critical during supply crunches when material availability determines who can complete jobs

A 2025 distributor survey of 1,020 roofing and exterior respondents found 50% listed increasing margins as a priority. Suppliers have flexibility built into their pricing. Contractors who ask for it at the right moment capture it; those who don't simply fund the distributor's margin instead.

Job-Level Profitability Tracking

Capturing better supplier pricing only matters if you can see where that margin lands internally. Mixing storm, retail, repair, and commercial revenue into one blended view hides which segments are actually making money. The minimum financial setup worth having:

- Separate P&L tracking by job type

- Job-level gross margin (not just revenue) tracked per crew

- Monthly review of which segments are performing and which are not

Cash Flow as a Profit Protector

Contractors who maintain peak-season spending through slow months often borrow to cover the gap — adding interest cost that erodes net margin steadily throughout the year. A cash reserve of two to three months of operating expenses provides the buffer that prevents financing costs from becoming a recurring margin drain.

Turning Warranties into a Recurring Profit Center

The Problem With How Most Contractors Handle Warranties

Right now, most roofing contractors treat labor warranties as an unfunded liability. A callback comes in — a leak, a flashing issue — and it comes straight out of operating cash with no reserve behind it. There's no predictability, no planning, and no upside.

The alternative is a warranty reserve: a small fee built into every job price that flows into a dedicated fund to cover future claims. Claims get paid from the fund. Any money that isn't used stays with you.

That single structural change converts warranties from a surprise expense into a managed, predictable cost.

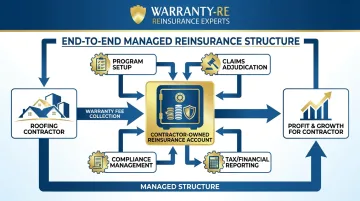

Contractor-Owned Reinsurance: The Next Level

The model most competitors haven't reached yet is owning the reinsurance structure outright. Instead of paying a third-party warranty provider and watching their underwriting profit disappear, a contractor-owned reinsurance company means the premium flows into a structure you legally own, backed by A-rated insurers.

Claims get covered when they happen. Unused premiums stay with you — the underwriting profit that third-party providers are currently keeping.

This is what WarrantyRE has been building for contractors since 1994. For roofing contractors, the program works by including a warranty fee in every job's contract price. That fee flows into the contractor's reinsurance account.

WarrantyRE handles the administrative side end-to-end, so contractors get the financial benefit without adding internal complexity:

- Program setup and company formation

- Claims adjudication and coverage decisions

- Compliance management and regulatory filings

- Tax returns and ongoing financial reporting

The structure is also tax-advantaged. Contributions to the reinsurance account carry significant tax benefits — a meaningful financial advantage on top of the underwriting income itself.

A common misconception is that this model requires high volume or significant capital to start. Neither is true — the program is designed to scale from wherever a contractor's business currently stands.

Warranties as a Sales Tool

Beyond the financial mechanics, a strong warranty offering closes retail jobs. When homeowners are comparing two contractors and one has a documented, backed labor warranty and the other has a verbal promise, the decision often comes down to confidence — and the contractor with the funded warranty program can support that confidence with proof.

Homeowners consistently rank warranty backing alongside licensing and material quality when choosing between contractors. That means the same program that builds a profit reserve also becomes a closing tool — one that works before the job starts and keeps paying after it's done.

Frequently Asked Questions

How much profit does a roofer make on a roof?

At a 28% median gross margin (per CFMA NAICS 238160 data), a $15,000 job generates roughly $4,200 in gross profit before overhead. After overhead, industry data puts median net margin at 3–6% — meaning that same job nets $450–$900. Repair work typically carries higher margin rates than full replacements.

Is $30,000 too much for a roof?

Roof pricing depends on size, pitch, material, and regional labor costs. The national average for professional roof replacement is $9,544, so $30,000 likely reflects a larger home, premium materials, or a complex installation. From a contractor's standpoint, the price needs to cover all direct costs plus overhead allocation to be profitable — regardless of what competitors are charging.

What is a good profit margin for a roofing business?

CFMA data shows a median gross margin of 28% for roofing contractors, with median net profit around 3%. Well-run operations targeting 6–10% net margin are outperforming most of the industry. Anything below 3% net signals a structural issue — typically in pricing, overhead, or both — worth investigating line by line.

What are the biggest costs that hurt roofing profit margins?

Materials represent the largest direct cost category, followed by labor (which has increased for seven in ten contractors since 2023), and sales commissions structured on revenue rather than gross profit. Overhead creep — costs that grew with the business but didn't shrink when revenue plateaued — is the margin drain most contractors don't catch until it's already costing them real money.

How can roofing contractors create recurring revenue?

Roofing runs on projects, but recurring income is achievable. Annual inspections, gutter cleaning, and preventative maintenance agreements create predictable seasonal revenue. Contractor-owned warranty reinsurance structures through programs like WarrantyRE also generate ongoing underwriting income from warranty fees collected on every completed job.

Why do roofing profit margins tend to be lower than HVAC or plumbing?

Roofing is materials-heavy in a way most trades aren't — materials consume a large share of every job dollar before overhead is even applied. Service-based trades like HVAC and plumbing carry far less material cost relative to revenue, which leaves them structurally more margin. That's why pricing discipline and material cost control matter more in roofing than in almost any other trade.