This guide isn't for homeowners trying to understand what their roof warranty covers. It's for contractor owners who want to understand what the three main warranty program structures actually cost them, how each one affects profitability and liability, and what questions to ask before committing to any of them.

By the end, you'll have a clear picture of each model's financial mechanics and a framework for deciding which one fits where your business is headed.

TL;DR

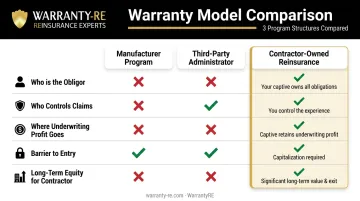

- Roofing warranty programs fall into three models: manufacturer certification, third-party administration, and contractor-owned reinsurance — and which one you choose determines where the profit goes.

- Manufacturer programs build credibility but keep all underwriting profit with the manufacturer.

- Third-party programs are easier to enter but charge ongoing premiums with no contractor control over claims decisions.

- With contractor-owned reinsurance, unused premiums stay in your company — turning warranty coverage into a profit center and a long-term business asset.

- Business size and growth goals shape the decision — but so does how long you're willing to let someone else keep your underwriting profit.

Why Your Warranty Program Choice Matters More Than You Think

For most small contractors, warranty programs feel like a customer service feature — something you offer to close jobs. The financial reality is different.

Every roofing install that carries a warranty fee generates income. Where that money goes depends entirely on your program structure. In some models, it flows permanently to a manufacturer or administrator. In others, it stays with your business.

The Competitive Pressure Is Real

According to IBISWorld, there are 108,598 roofing contractor businesses in the US in 2026 — up 2.6% from the prior year and growing at a 3.4% annual rate over the past five years. In that environment, the ability to hand a homeowner a documented, branded warranty at the table is a real closing advantage.

Homeowners do ask about workmanship coverage before signing. Contractors without a structured program lose jobs to competitors who can hand a customer a documented, branded warranty at the table. A verbal promise carries neither the weight nor the financial backing of a documented program.

The warranty program question has two layers: what you offer customers, and who keeps the fees you collect. Most contractors focus on the first. The second is where long-term business value — and real margin — actually gets built.

The Three Types of Roofing Warranty Programs Contractors Can Offer

These aren't just products to sell customers. They're business structures with different financial and operational consequences for the contractor. Here's how each one works.

Manufacturer Certification Programs

Programs like GAF's Master Elite, Owens Corning's Platinum Contractor, and CertainTeed's ShingleMaster tiers follow the same basic structure: contractors apply for tiered certification, meet ongoing requirements around training, volume, and liability insurance, and in return unlock enhanced warranty products — including workmanship coverage that the manufacturer backs.

What this looks like in practice:

- GAF Master Elite requires $1M liability insurance, workers' compensation, state licensing, 1,000 Rewards Squares annually, 500 Warranty Squares for Silver and Golden Pledge, and 10 Learning Credits per renewal cycle.

- Owens Corning Platinum Contractor requires $1M general liability, satisfactory business credit, required licenses, and completion of training through Owens Corning University.

- CertainTeed ShingleMaster PRO/PREMIER requires the Master Craftsman Roofing Contractor and Shingle Quality Specialist credentials and unlocks SureStart PLUS coverage with up to 25 years of workmanship protection.

The trade-off for small contractors is straightforward: manufacturer programs provide real credibility and transfer some liability risk. Under GAF's Golden Pledge and Owens Corning's Platinum Protection, the contractor covers the first two years when an installation error is found — and if the contractor is unable or unwilling to perform repairs, the manufacturer steps in.

But all underwriting profits stay with the manufacturer. You pay fees and meet volume commitments; they keep the spread between premiums collected and claims paid.

Official fee details aren't publicly disclosed on manufacturer websites, so request current written contractor terms directly before building projections around any tier.

Third-Party Warranty Administrators

In this model, a contractor pays a premium to an outside organization — per project or annually — and receives a branded warranty product to offer customers. The administrator handles claims adjudication and compliance.

The appeal is lower barriers to entry. No volume commitments, no multi-year certification pathway. Small or newer contractors can offer documented workmanship coverage quickly.

There are real limitations:

- The contractor pays premiums indefinitely and earns no underwriting profit

- Claims are adjudicated by the administrator, not the contractor — so denials or delays happen without contractor input

- The contractor's customer relationship suffers when a claim goes sideways and the contractor has no recourse

For a contractor early in business, a third-party program may be a reasonable starting point. For one doing steady volume, it's a recurring cost with no equity upside.

Contractor-Owned Reinsurance Programs

This is the model most small contractors have never heard of — and the one with the most significant long-term financial implications.

In a contractor-owned reinsurance structure, the contractor establishes their own administrator-obligor reinsurance company, backed by A-rated insurers. Warranty fees are collected from customers into an account the contractor's company controls. Valid claims are paid from that pool. Whatever remains after claims are paid is underwriting profit — and it stays with the contractor's company.

WarrantyRE helps small roofing contractors establish and manage this structure. Their full-service administration covers every piece the contractor would otherwise need to build independently:

- Claims adjudication from first call to final payout

- Monthly financial statements and annual reporting for tax preparation

- Compliance coordination and all legal filings, tax returns, and renewals

The contractor's reinsurance company is supported by A-rated insurers — so if the contractor's company can't meet its obligations, the direct writing insurance carrier covers claims.

The core shift is financial: warranty revenue that once left on every job now accumulates in a company the contractor owns — one that can grow in value, improve tax positioning, and compound over time.

Key Warranty Terms Small Contractors Need to Understand

Four terms come up in nearly every warranty program conversation — and not knowing them puts you at a real disadvantage when evaluating what you're actually signing up for.

Workmanship Warranty vs. Manufacturer Warranty

These are distinct obligations, and confusing them creates real liability problems.

A manufacturer warranty covers defects in materials — shingles, underlayment, accessories. It comes from the product company, not the contractor. A workmanship warranty covers installation errors. It comes from the contractor.

When a contractor offers a workmanship warranty, they are personally taking on financial liability for their installation quality. The program structure behind that warranty determines who actually funds that liability — the contractor's own pocket, an administrator, or a reinsurance structure the contractor owns.

Prorated vs. Non-Prorated Coverage

Prorated coverage decreases in value as the roof ages. A claim filed in year 12 of a 25-year prorated warranty won't pay full replacement cost — it pays a fraction based on remaining useful life. Non-prorated coverage maintains full replacement value throughout the coverage period.

This gap matters directly when setting customer expectations and when calculating what your program must be funded to cover. GAF's warranty comparison materials use non-prorated periods to define full-coverage windows within their tiered products.

Administrator-Obligor and Underwriting Profit

The administrator-obligor is the entity legally responsible for paying warranty claims. In a contractor-owned reinsurance structure, the contractor's company takes on this role, backed by a reinsurance agreement with an A-rated carrier.

Underwriting profit is what remains after valid claims are paid from collected premiums. In manufacturer and third-party programs, that profit goes to the program provider. In a contractor-owned structure, it stays with the contractor's company.

Claims Adjudication

Claims adjudication is the evaluation and approval or denial of warranty claims. In manufacturer and third-party programs, the administrator controls this entirely. A contractor whose customer faces a denied or delayed claim has no input into that decision — and takes the reputational hit regardless of how the claim is resolved.

In a contractor-owned model managed by a company like WarrantyRE, adjudication is handled on the contractor's behalf, and the financial outcome of that process flows back to the contractor's company rather than a third-party administrator.

How to Evaluate a Warranty Program: What Small Contractors Should Ask

Before committing to any program, work through these questions:

On obligations and control:

- Who is the obligor — the manufacturer, a third party, or your own company?

- Who controls claims adjudication, and what are the typical response timelines?

- Can you exit the program, and what are the terms for doing so?

On costs and eligibility:

- What are the total annual costs — membership fees, per-project enrollment, inspection requirements?

- What are the minimum eligibility requirements — years in business, liability insurance levels, volume commitments?

- Do you currently qualify, or would you need to meet conditions before the program applies?

On profit and equity:

- Does the program generate any long-term equity in your business, or is it purely an operating expense?

- Who keeps the underwriting profit from warranty fees collected on your jobs?

That eligibility question deserves a closer look. Manufacturer certification programs often require minimum years in business, $1M+ in liability coverage, and ongoing volume commitments. Newer or smaller operators may not yet qualify for the highest tiers. Building a sales pitch around Golden Pledge or Platinum Protection before confirming eligibility is a waste of time — and a real customer service problem when the offer falls apart.

Program flexibility is the final piece worth examining. Some programs let contractors set their own coverage terms and durations. Others lock you into fixed products with no room to adjust. The more flexibility you have, the better positioned you are to price competitively and tailor offerings to your local market.

The Hidden Profit Opportunity in Warranty Programs

Here's the financial reality most small contractors miss: every roofing job with a warranty fee moves money somewhere. In manufacturer and third-party models, that money leaves permanently. In a contractor-owned reinsurance structure, it stays inside a company you own.

How the Math Works

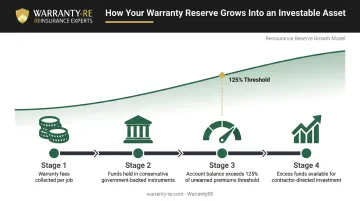

When contractors build warranty fees into job pricing, those fees flow into a reinsurance account the contractor controls. Claims come out of that account. Whatever isn't paid in claims accumulates as underwriting profit — funds that belong to the contractor's reinsurance company.

WarrantyRE's program also allows accumulated warranty reserves to be invested. Initially, those funds are held in conservative government-backed instruments. Once the account balance exceeds 125% of unearned premiums, excess funds can be invested at the contractor's direction — creating a secondary return on top of underwriting profits.

The IRC Section 831(b) Consideration

Contractors who establish their own small reinsurance company may qualify for an election under IRC Section 831(b). For 2026, IRS Rev. Proc. 2025-32 sets the net written premium limit at $2,900,000 annually. Companies qualifying under this election are taxed only on investment income — not on premium revenue.

Profits distributed from the reinsurance company may qualify for capital gains tax treatment rather than ordinary income rates, depending on the entity structure, shareholder details, and holding period. This is a meaningful difference for a contractor in a high income-tax bracket.

This is not a tax shelter. The IRS has flagged poorly structured micro-captive arrangements as transactions of interest under Notice 2016-66. Disqualifying factors typically include:

- Vague or undefined coverage terms

- Premiums not grounded in actuarial analysis

- Weak or absent claims administration

A properly structured program — with real underwriting, genuine claims administration, and qualified tax counsel — satisfies IRS standards. WarrantyRE coordinates with specialized CPAs and legal counsel throughout.

Money that flows to a manufacturer or third-party administrator today could be building a financial asset you own instead. That's the structural shift this program makes possible.

Frequently Asked Questions

Do small roofing contractors actually need to offer a warranty program?

Without a written warranty, you're carrying unmanaged liability with no financial backing. Verbal guarantees offer no protection if a claim arises — and increasingly, customers won't sign without documented workmanship coverage. A structured program protects both sides.

What is the difference between a workmanship warranty and a manufacturer warranty for contractors?

A manufacturer warranty covers material defects and comes from the product company. A workmanship warranty covers installation errors and comes from the contractor — meaning the contractor's own program structure determines how that liability is funded, whether that's out of pocket, through a third party, or through a reinsurance company the contractor owns.

How much does it cost a small contractor to offer a warranty program?

Costs vary by model. Manufacturer certification carries fees and volume requirements; third-party programs charge per-project premiums with no equity upside. Contractor-owned reinsurance programs have setup costs, but retained underwriting profits are structured to offset them over time.

Can a small roofing contractor set up their own warranty company?

Yes — through an administrator-obligor reinsurance structure backed by A-rated insurers. WarrantyRE helps small contractors establish and manage this type of program, handling compliance, legal filings, tax returns, claims adjudication, and financial reporting. Volume doesn't need to be large for the structure to work.

What happens to a customer's workmanship warranty if the roofing contractor goes out of business?

If a contractor closes, a standard contractor-issued workmanship warranty becomes unenforceable. Manufacturer-backed programs like GAF's Golden Pledge transfer that obligation to the manufacturer. In a properly structured reinsurance program, the A-rated carrier maintains claims responsibility even if the contractor's company can't.

What warranty program terms should small contractors watch out for?

Key terms to scrutinize before signing: proration clauses (reduce payout as the roof ages), exclusions that leave common installation errors uncovered, eligibility requirements that may disqualify newer businesses, and exit restrictions that lock you into the program. These rarely come up during the sales conversation — ask for the full contract language upfront.