That's a mistake — and it's quietly costing established contractors real money.

With over 108,000 roofing contractor businesses competing across a $92.5 billion market, differentiation matters. But this article isn't primarily about using warranties to stand out from competitors. It's about how your warranty program's structure determines whether premium dollars build your business — or someone else's.

You'll learn how warranty strategy drives scaling through three specific levers: winning better jobs, building lasting customer loyalty, and turning premium dollars into a recurring revenue stream you actually own.

TL;DR

- Most roofing contractors send premium dollars to third parties without examining who keeps the profit.

- Three warranty models exist — manufacturer certification, third-party administration, and contractor-owned reinsurance — and your choice determines where the money lands.

- The contractor-owned reinsurance model lets you collect premiums, control claims, and retain underwriting profits instead of forfeiting them.

- Strong warranties reduce price objections, create post-sale touchpoints, and generate referrals that compound over time.

- This guide breaks down each model and shows you how to choose the one that builds your business — not someone else's.

Why Most Roofing Businesses Hit a Growth Ceiling

The classic roofing plateau looks something like this: revenue climbs to a threshold, then stalls. The owner is still running jobs, managing crews, and handling customer calls. The business runs on hustle, not systems. There's no recurring revenue to smooth out slow seasons or fund the next phase of growth.

Warranties play an underappreciated role in this dynamic. On every job, a warranty fee goes out the door to a manufacturer or third-party administrator. Multiply that across dozens or hundreds of annual installs, and the total is substantial. Yet almost no contractors audit this number, let alone ask whether any portion of it could stay in their business.

The core issue is structural. More than 90% of professional contractors offer some form of warranty, according to HIRI — which means warranty availability is table stakes, not a differentiator.

The question isn't whether you offer one. It's whether your warranty program makes your business more profitable or just transfers risk in exchange for ongoing fees.

There's a real financial distinction between those two outcomes:

- Transferring risk to a third party creates a recurring expense with no upside, even when your claim rate stays low

- Owning the program structure means unused premiums accumulate in an account your business controls

- Higher install volume amplifies both outcomes — the more jobs you run, the more you gain or lose depending on which side of that line you're on

- No change to your installation process is required — the shift is purely structural, not operational

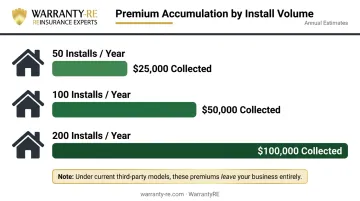

That difference compounds at scale. A contractor doing 50 installs a year loses less to third-party premiums than one doing 200 — but the contractor doing 200 has the most to gain by changing the structure. At 200 installs annually, even a modest per-job premium recaptured adds up to tens of thousands of dollars that currently leave your business every year.

The Three Warranty Program Models Every Roofing Contractor Should Know

Most contractors choose their warranty program based on brand name or ease of setup — not on financial terms. Here's how each model affects your bottom line.

Manufacturer Certification Programs

Programs from GAF, Owens Corning, CertainTeed, and similar manufacturers offer tiered certification that unlocks progressively stronger warranty products. At the top tiers, contractors can offer workmanship coverage backed by the manufacturer — GAF's Master Elite tier, for example, allows contractors to offer the Golden Pledge warranty with up to 30 years of workmanship coverage.

The credibility these programs provide is real. The manufacturer's name carries weight with homeowners, and workmanship liability is transferred off the contractor for qualifying claims.

The financial trade-off is equally real: certification requires ongoing fees and product commitments, and all underwriting profits stay with the manufacturer. If your claim rate is low — as it tends to be for quality contractors — the manufacturer keeps the difference between what they collect and what they pay out. You receive none of it.

Third-Party Warranty Administrators

Third-party programs let contractors offer branded warranty products without manufacturer certification, paying premiums to an outside administrator who manages claims. The barrier to entry is lower, and there's less administrative complexity than manufacturer programs.

The underlying economics, though, follow the same pattern. Premiums flow out on every job, claims are adjudicated by someone else, and underwriting profit (the gap between premiums collected and claims paid) stays with the administrator. You also have minimal influence over how claims are handled — a secondary risk to your reputation when customers interact with a third party on your behalf.

Contractor-Owned Reinsurance

This is the model most contractors have never examined closely. In a contractor-owned reinsurance structure, the contractor establishes their own administrator-obligor warranty company (backed by A-rated insurers) that collects premiums, controls the claims process, and retains 100% of underwriting profits.

Premiums collected on every install go into an account the contractor's business owns. Claims are paid from that account. Whatever remains is yours.

Which model fits which stage:

- Newer or lower-volume contractors — manufacturer or third-party programs offer simplicity and lower setup burden

- Established contractors with significant install volume — contractor-owned reinsurance becomes increasingly advantageous as the dollar amount flowing to third parties grows

- Contractors expanding into premium product lines — owning the warranty program reinforces premium positioning and matches the quality signal of higher-end work

How Owning Your Warranty Program Turns Installs Into Recurring Revenue

The Profit Flow Shift

On a $9,544 average roof replacement (per Angi's 2026 data), a warranty fee is already built into the price — the homeowner is paying it. Under a manufacturer or third-party program, that fee leaves your business the moment the job closes. Under a contractor-owned reinsurance structure, it goes into an account you control.

Consider what that difference looks like across a year of installs:

| Annual Installs | Warranty Fee Per Job | Annual Premiums Collected |

|---|---|---|

| 50 | $500 | $25,000 |

| 100 | $500 | $50,000 |

| 200 | $500 | $100,000 |

These numbers are illustrative — actual fee structures vary by program, job size, and coverage scope. At volume, the premium dollars flowing to third parties add up to a real and largely unexamined loss.

Claims Retention and Underwriting Profit

The contractor-owned model's financial case rests on claims retention. Well-run contractors who do quality work typically have low claim rates. Under a third-party model, that low claim rate benefits the administrator — not you.

Under a contractor-owned structure, the gap between premiums collected and claims paid out accumulates in your reinsurance account. That balance is a financial asset your business owns, and it grows with every install and every claim-free year.

The Tax Dimension

Under IRC Section 831(b), qualifying small insurance companies with net written premiums at or below $2,900,000 (the 2026 limit per IRS Rev. Proc. 2025-32) may elect to be taxed only on investment income rather than underwriting income. This election can be material for contractors whose reinsurance company stays within the threshold.

Two important caveats apply here:

- The IRS has identified certain micro-captive arrangements as transactions of interest or listed transactions, particularly where financing flows back to related parties or claim rates are unusually low

- Tax outcomes depend on your specific structure, and this area requires qualified tax and legal counsel — not a DIY approach

WarrantyRE partners with insurance tax experts and CPAs to handle all tax filings and compliance for client reinsurance companies, and takes IRS compliance seriously at every step.

Controlling the Claims Experience

When a customer files a warranty claim through a manufacturer or third-party administrator, the outcome and timeline are outside your control. A slow or adversarial claims process becomes your reputation problem — not the administrator's.

When you own the program, that changes. WarrantyRE handles all administration and claims adjudication, from the first call to final payout. The contractor stays out of the paperwork, but the process reflects the contractor's standards rather than a third party's.

WarrantyRE: The Implementation Pathway

For contractors asking "how do I actually do this?", WarrantyRE (warrantyRE.com, (804) 824-9533) has been setting up administrator-obligor reinsurance companies for roofing and other home service contractors since 1994. Their full-service administration covers legal formation, compliance management, claims adjudication, staff training, tax returns, and performance reporting.

The contractor doesn't build the structure alone — that's the point. WarrantyRE handles the infrastructure so contractors can focus on running their business while the reinsurance company runs in the background, accumulating profit on every install.

How a Strong Warranty Strategy Builds the Customer Loyalty That Scales a Business

A workmanship warranty doesn't just close the sale — it keeps the contractor connected to the customer after the job is done. That ongoing relationship creates natural touchpoints: annual check-ins, seasonal follow-ups, renewal reminders. Without a warranty program, the transaction ends when the crew leaves. With one, you have a legitimate reason to stay in contact.

That ongoing contact directly fuels referrals. According to Jobber's 2026 Home Service Trends Report, 59% of home service professionals say referrals and repeat work are their top sources of new leads, with benchmarks suggesting 15% to 35% of new work should come from this channel.

Customers who feel genuinely protected — and who have a claim handled without friction — refer more. Word-of-mouth in home services runs on one story: not your nail pattern, but how you responded when something went wrong six months after the job.

What separates contractors who win referrals from those who don't:

- Customers remember how a problem was resolved, not how smoothly the install went

- A warranty honored quickly turns a frustrated caller into a vocal advocate

- Regular check-ins keep your name top of mind when a neighbor asks for a roofer

Standing Out When Everyone Is Bidding the Same Job

When multiple contractors are competing for the same project, the one who can clearly explain what their warranty covers, who backs it, and what happens during a claim projects more credibility than the one pointing to manufacturer fine print. Owning your warranty program gives you something concrete to say — and homeowners notice.

Pairing Warranty Strategy With Other Scaling Moves

A strong warranty program doesn't operate in isolation — it works alongside the other moves contractors make to scale. Three areas where it compounds:

Premium pricing: Price sensitivity is real. Modernize's 2025 homeowner research found that 40% of homeowners cite lowest overall price as their primary reason to choose one contractor over another. A well-articulated warranty — one that clearly explains coverage, backing, and the claims process — removes a key objection that drives homeowners toward cheaper bids. The warranty becomes part of the value case, not just a line item.

Premium product lines: Contractors expanding into metal roofing, full exterior replacement, or higher-end product tiers need warranty programs that match the quality signal of those products. A contractor-owned program, structured and administered professionally, reinforces that premium positioning — rather than undermining it with manufacturer fine print that applies to everyone equally.

Operational efficiency: When warranty administration is handled by a full-service program, contractors free up time that would otherwise go to administrative follow-up. Pair that with AI scheduling tools, CRM automation, and streamlined estimating, and the result is concrete: more hours available for sales and installation, less time managing paperwork.

How to Start Using Warranty Strategy as a Scaling Tool

Step 1: Audit Where Your Current Warranty Dollars Go

Calculate the total you pay in warranty-related fees annually across all jobs — to manufacturers, third-party administrators, or elsewhere. Then ask: does any portion of underwriting profit return to your business?

For most contractors, the answer is no. That single exercise often reveals a profit leak that's been running quietly for years.

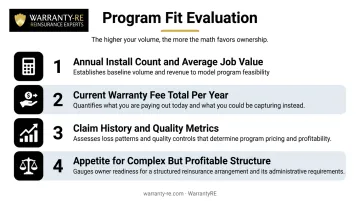

Step 2: Evaluate Your Install Volume and Program Fit

The financial advantage of a contractor-owned reinsurance structure scales with volume. The biggest misconception is that you need to be a large operation or that startup costs are prohibitive. Both are wrong. Contractors at earlier growth stages often start with manufacturer or third-party programs, then move into a reinsurance structure as volume builds.

An honest program-fit evaluation looks at:

- Annual install count and average job value

- Current warranty fee total (what you're paying out per year)

- Claim history and quality metrics

- Appetite for a more complex but more profitable structure

Step 3: Partner With a Program Administrator

Setting up a contractor-owned reinsurance company involves legal formation, state compliance requirements, claims adjudication infrastructure, and ongoing reporting systems. This isn't a DIY project. The contractors who do it successfully work with experienced administrators who've built this structure hundreds of times.

WarrantyRE handles the full setup for you. That means legal filings, compliance management, staff training, claims adjudication, tax returns, and performance reporting — all managed on your behalf. You get the financial benefits of ownership without needing to become an insurance compliance expert.

Frequently Asked Questions

How to scale a roofing business?

Scaling requires building systems that run without the owner on every job, diversifying lead channels, and using tools that reduce overhead per install. What most contractors overlook: restructuring your warranty program to retain underwriting profits — rather than sending them to a third party — turns a recurring cost into a financial asset that grows with volume.

Do most roofing companies offer a warranty?

Yes — HIRI reported that more than 90% of professional contractors offer a warranty. But warranty availability isn't the real question. The more important question for business owners is whether their warranty program structure returns any financial value to the business, or simply transfers risk at a recurring cost.

What is a contractor-owned warranty reinsurance company?

It's an administrator-obligor entity the contractor establishes — backed by A-rated insurers — that collects warranty premiums, manages claims, and retains underwriting profits. Instead of sending premium dollars to a manufacturer or third-party administrator, those funds accumulate in an account the contractor's business owns.

How does owning a warranty program help a roofing business grow?

Owning your warranty program works on three levels:

- Captures underwriting profit on every install instead of sending it to a third party

- Keeps claims under your control, protecting customer relationships when issues arise

- Builds business equity through accumulated premium reserves that grow with each job

What warranty should a roofing contractor offer to win more jobs?

The most competitive contractors offer both material and workmanship coverage. The structure backing that warranty — manufacturer, third-party, or contractor-owned — determines how credible the offer sounds. It also determines how much of the premium dollar stays in your business rather than leaving it.

Can a smaller roofing contractor benefit from a reinsurance warranty model?

The model scales with install volume, and there's no hard threshold to qualify. Smaller contractors often start with manufacturer or third-party programs, then move to a reinsurance structure as volume grows. WarrantyRE evaluates each business individually and can help assess when the switch makes financial sense.