Introduction

Warranty callbacks represent one of the biggest margin leaks in roofing. According to industry data on roofing profitability, warranty repairs are "pure cost with zero revenue" — labor is consumed without generating the 35-40% gross margin a standard job would produce. When roofing crews are diverted from billable installation work to warranty rework, businesses absorb both the direct cost of labor and the opportunity cost of lost production.

Companies that fail to manage callbacks and rework fall into "Red Flag" territory with net profit margins below 5%. By contrast, well-run roofing operations that actively track and minimize callbacks achieve 8-15% net profit margins. This spread illustrates how unmanaged warranty liability doesn't just reduce profit — it determines whether a roofing business survives at all.

Roofing warranty liability doesn't primarily result from bad luck or severe weather. It becomes expensive through decisions made before the job starts, language written into contracts, and the absence of a system to manage claims once they arise. The good news: each of those decisions is within your control — and fixing them has a direct impact on your bottom line.

TLDR

- Warranty liability accumulates through callbacks, repair labor, materials, and customer disputes — not as one visible expense

- Installation quality, warranty contract scope, and claim handling processes are the biggest drivers

- Reducing liability starts before the job begins: tighter warranty language, crew training, pre-install inspections

- Structured post-installation management — photo documentation, customer sign-offs, scheduled follow-up — builds a defensible paper trail

- Transferring warranty risk through reinsurance protects cash flow and turns warranty programs into a profit source

How Warranty Liability Builds Up for Roofing Businesses

Warranty costs for roofing contractors rarely appear as a single line item. They accumulate over warranty periods through repeated callbacks, incremental repair costs, crew time diverted from paid jobs, and the administrative burden of managing disputes.

A single warranty event may trigger multiple service visits, each consuming labor hours, materials, truck rolls, and administrative overhead that never appears on a P&L statement as "warranty expense."

Most roofing warranty liability is unpredictable rather than gradual. It surfaces when conditions expose an installation issue — after the first major storm, freeze-thaw cycle, or following a homeowner modification. Roofs can perform well for years, then multiple warranty issues surface at once — long after the contractor has mentally closed out the job.

According to research on commercial roofing warranties, a typical 20-year No Dollar Limit warranty often sees roofs perform for 15 years with only minor repairs before major failures occur. At that point, warranty value has depreciated significantly while repair costs have increased — creating a financial gap the contractor must absorb.

Direct repair costs are only part of the picture. Each warranty event can trigger additional losses:

- Customer escalations that turn into legal disputes with attorney fees

- Consequential damage claims — interior water damage, mold, structural issues — that exceed the cost of the roof repair itself

- Reputational damage affecting future sales and referral business

- Loss of crew productivity when billable work stops for warranty callbacks

Average insurance payouts for water damage claims reach $13,954, while typical roof leak repairs cost $350 to $1,500. When interior damage follows a roofing failure, the contractor's exposure can dwarf the original repair cost — and that gap falls squarely on your business unless your warranty program is structured to handle it.

Key Drivers of Roofing Warranty Liability

Installation Quality and Manufacturer Specifications

Installation quality and crew adherence to manufacturer specifications represent the single largest driver of warranty claims. According to NRCA guidance, many warranty claims brought against roofing material manufacturers are ultimately traced back to poor installation practices rather than material defects.

Common installation deviations that trigger predictable, repeat claims:

- Incorrect nail count, placement, or penetration depth on fastening

- Ventilation below NRCA's minimum 1:150 ratio (1 sq ft of net free ventilation per 150 sq ft of attic space)

- Wrong underlayment type or improper installation method

- Layering new materials over old, creating an unstable substrate

- Using incompatible system components that void the manufacturer's coverage

Each deviation can void manufacturer coverage and shift the liability entirely onto the contractor. Owens Corning requires four nails per shingle for warranty qualification on Duration shingles, with six required in high-wind zones. In Florida, for example, building code outside high-velocity hurricane zones requires only four nails — but Owens Corning's warranty requires six. A code-compliant installation can still void the manufacturer warranty entirely.

Warranty Language and Legal Exposure

Warranties written without clear exclusions for homeowner-caused damage, acts of God, improper maintenance, or unauthorized modifications leave contractors exposed to claims they never intended to cover. Vague language around what constitutes a "defect" or "failure" gives courts room to interpret coverage broadly.

One of the most critical vulnerabilities in this area involves consequential damages.

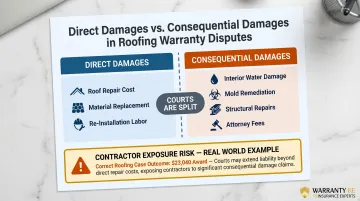

Direct vs. Consequential Damages — Courts Are Split:

According to legal analysis by construction attorneys, courts have struggled to distinguish between direct and consequential damages from defective roofs. Some courts rule that interior water damage from a defective roof is a "direct damage," making standard consequential damage disclaimers ineffective. Other courts classify interior damage as "consequential," upholding the disclaimer.

Recommendation: Use specific, unambiguous exclusionary language such as "Damage to the interior of the building is excluded" rather than relying on general "consequential damages" waivers.

Case Example: In Correct Roofing Inc. v. Alfredo Vasquez (2024), an Indiana contractor was held liable for $23,040 total: $7,000 for hiring a second contractor to repair the roof, $9,800 in consequential damages for interior water damage, and $6,240 in attorney fees. The court found interior water damage was a "reasonably foreseeable" consequence of the roof failure, making the contractor liable despite the breach being installation-related.

Post-Installation Homeowner Behavior

Homeowner actions after installation can cause failures that are genuinely not your fault — but without explicit exclusions in the warranty, the claim lands on you anyway.

Common homeowner actions that void coverage when properly excluded:

- Pressure washing that damages shingles or displaces granules

- Installing satellite dishes or solar panels without consulting the contractor

- Neglecting maintenance requirements like gutter cleaning

- Allowing excessive foot traffic or unauthorized roof access

- Delaying leak reporting, allowing minor issues to become major damage

Without written exclusions for these actions, contractors remain liable even when homeowner negligence caused the failure.

Strategies to Reduce Roofing Warranty Liability

Reducing warranty liability requires roofing businesses to address three distinct leverage points: decisions made before and during installation, how warranties are managed after job completion, and the broader financial structure behind the warranty program.

Strategies That Reduce Liability by Changing Decisions

Narrow Warranty Definitions:

Reduce liability at the point of warranty design. Roofing contractors should narrowly define what the workmanship warranty covers — specific installation-related failures only.

Explicitly exclude:

- Storm damage and acts of God

- Homeowner-caused modifications or unauthorized penetrations

- Improper maintenance or deferred upkeep

- Manufacturer material defects (already covered by manufacturer warranty)

Pre-Installation Site Documentation:

Create a defensible baseline before work begins:

- Photograph roof deck conditions, existing damage, and structural issues

- Document ventilation assessments and measurements

- Record any pre-existing conditions in writing

- Obtain written customer acknowledgment of existing conditions

Claims against pre-existing conditions cannot be defended without this paper trail. Industry guidance emphasizes that documentation may be required to file warranty claims and provides critical protection in disputes.

Subcontractor Indemnification Agreements:

Subcontractor agreements should include indemnification clauses that assign liability back to the party responsible for the work. If a subcontracted crew causes an installation defect, the contractor's warranty exposure should not absorb a loss the subcontractor caused. Many roofing businesses operate without these agreements and end up covering costs that belong to the subcontractor.

Warranty Pricing Based on Actual Risk:

Many contractors offer warranties as sales tools without calculating actuarial cost per job. According to warranty program administrators, warranties are "generally seen as a cost-of-doing-business but are rarely accounted for as such." Contractors who fail to track callback rates and warranty claim costs per install create unsustainable liabilities when under-priced warranties accumulate over time.

Strategies That Reduce Liability by Changing How Warranties Are Managed

Structured Post-Installation Inspections:

Schedule inspections at defined intervals — 30-day and 12-month check-ins work well — to catch minor issues before they become full warranty claims. Proactive outreach also signals professionalism, which lowers the likelihood of disputes reaching legal escalation.

Customer Sign-Offs at Job Completion:

A documented sign-off at job completion creates a clear legal record. Require customers to acknowledge:

- Documented punch list showing all work completed

- Photos of final installation condition

- Maintenance responsibility agreement outlining homeowner obligations

- Clear record of installation's condition at handoff

Courts and insurance adjusters rely heavily on this documentation when warranty disputes arise.

Crew Training on Warranty Implications:

Crews need to understand what a deviation from spec actually costs the business — not just how to install correctly, but why it matters to the bottom line. Contractors who tie installation quality to warranty reserve performance or bonus structures see lower callback rates.

Defined Claims Adjudication Process:

Establish a clear process:

- Who reviews a claim

- Who approves a repair

- What documentation is required

- What triggers escalation to legal review

This reduces cost per claim by preventing reactive, inconsistent responses that often result in over-spending to appease customers.

Structuring Warranties to Protect Cash Flow

Specific Warranty Exclusion Language:

General waivers rarely hold up — courts need specifics. Disclaim consequential damages by name: "Damage to interior finishes, mold remediation, and structural repairs are excluded from this warranty."

This approach addresses the legal inconsistency where courts have ruled differently on whether interior water damage is direct or consequential.

Manufacturer-Certified Contractor Programs:

Align with manufacturer-certified contractor programs to transfer significant portions of defect liability back to material manufacturers.

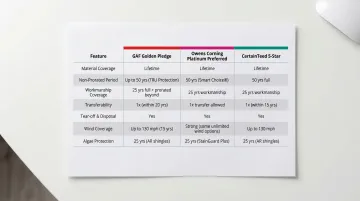

Examples:

- GAF Golden Pledge: 25 years workmanship coverage for Master Elite contractors. GAF assumes workmanship liability; even if the contractor goes out of business, GAF remains responsible.

- Owens Corning Platinum Protection: Limited Lifetime workmanship coverage for Platinum Preferred Contractors.

- CertainTeed 5-STAR Coverage: Fully transferable for 15 years.

These programs reduce contractor personal exposure on high-value jobs while providing extended coverage that differentiates their services.

Administrator-Obligor Reinsurance Structure:

Roofing contractors who establish a dedicated warranty reserve or administrator-obligor reinsurance structure stop absorbing warranty claim costs out of operating cash flow.

Instead of sending warranty premiums to a third-party warranty company that keeps the underwriting profit, contractors can work with a reinsurance partner like WarrantyRE to build a program where:

- Warranty fees collected on each job fund a claims reserve the contractor owns

- Warranty costs become predictable, funded liabilities rather than surprise expenses

- Unspent reserves become profit retained by the contractor

- Claims administration is handled entirely by the reinsurance administrator

- The program is backed by A-rated insurers for catastrophic claim protection

This transforms warranties from a cost center into a controlled revenue stream while protecting business cash flow from warranty-related volatility.

Conclusion

Roofing warranty liability doesn't come from a single source. It builds across installation decisions, contract language, claims handling, and financial structure — and each layer requires its own solution.

The most resilient roofing businesses treat warranty management as an ongoing operational discipline, not a one-time document. Contractors who build a structured, funded program around their warranty obligations protect their margins, improve their customer experience, and turn warranty costs into a predictable, manageable line item — rather than an unpredictable drain on cash flow.

One structural option worth exploring: a captive reinsurance program, where warranty premiums your customers pay are held in a company you own — rather than handed to a third-party provider. WarrantyRE has helped roofing and exterior contractors set up exactly this kind of program since 1994, giving them more control over claims, costs, and long-term profitability.

Frequently Asked Questions

What is the difference between a manufacturer's warranty and a workmanship warranty for roofing contractors?

The manufacturer's warranty covers material defects and is tied to the product, issued by companies like GAF or Owens Corning. The workmanship warranty is issued by the contractor and covers installation errors. Workmanship claims come out of the contractor's pocket — manufacturer warranties do not.

What warranty language should roofing contractors include to limit their legal liability?

Include explicit disclaimers of consequential damages with specific language: "Damage to interior finishes is excluded." List specific homeowner-caused exclusions: pressure washing, unauthorized penetrations, deferred maintenance. Use precise failure definitions rather than vague terms like "defect" to prevent broad judicial interpretation.

How can I reduce warranty claims without shortening my warranty period?

Claim frequency is driven by installation quality and documentation, not warranty length. Improve crew training on manufacturer specifications, conduct pre-install inspections with photo documentation, and require post-install customer sign-offs. These steps reduce claims regardless of coverage term.

What is roofing warranty reinsurance and how does it protect my business?

Reinsurance allows a roofing contractor to establish their own warranty company backed by an insurer. You collect warranty fees on each job into a funded reserve, and warranty claim costs are paid from that pool rather than operating cash flow. Unspent reserves remain your property as profit.

Can homeowner negligence void a roofing contractor's workmanship warranty?

Yes, but only if the warranty explicitly states which homeowner actions constitute grounds for voiding coverage: pressure washing, unauthorized attachments, failure to maintain gutters, or delayed leak reporting. Without written exclusions naming these specific actions, contractors may remain liable even when homeowner negligence caused the failure.

How long should a roofing contractor's workmanship warranty be?

Warranty length should match your ability to fund or insure claims over that period. A structured reinsurance program makes longer warranties a practical selling point rather than a financial risk, letting you offer extended coverage without the liability exposure.