Introduction

Home service contractors—HVAC technicians, roofers, plumbers, and electricians—face mounting pressure to stand behind their work with formal warranties. Customers expect protection, lenders sometimes require it, and competitors are already offering it. The problem is that most warranty arrangements are built to benefit the provider, not the contractor.

The typical warranty arrangement works like this: you pay premiums to a warranty provider, they collect fees on every job you complete, and when claims stay low, they pocket the difference. Meanwhile, your phone still rings when a customer has a problem—even if the warranty company is slow to respond or disputes the claim.

When you sell through a third-party warranty provider, you hand over the underwriting profits while keeping 100% of the reputational risk when claims go wrong.

This guide ranks the best home service contractor warranty companies based on program structure, profit potential, compliance support, and contractor control. Whether you're an HVAC contractor managing callbacks on $15,000 system replacements or a roofer protecting labor on $30,000 installations, the right warranty partner directly impacts your bottom line.

TL;DR

- Contractor warranty programs cover post-installation repairs, callbacks, and system failures—distinct from manufacturer coverage

- The best programs give contractors control over claims, pricing, and profits—not just coverage

- Third-party providers keep underwriting profits; reinsurance models let contractors own their warranty company and recapture those dollars

- Five providers stand out across different contractor needs: from plug-and-play third-party coverage to full reinsurance ownership

- Choose based on who controls claims, who keeps the profits, and how much compliance support is included

Overview of Home Service Contractor Warranty Programs

A home service contractor warranty is a structured agreement you offer customers covering repair or replacement costs on your installed systems and labor for a defined period. This is distinct from manufacturer warranties (which cover equipment defects) and consumer home warranties (third-party service contracts homeowners purchase separately).

Contractors encounter two primary program models:

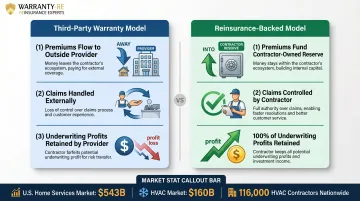

Third-Party Warranty Providers: You sell coverage underwritten and administered by an outside company. The provider collects premiums, handles claims, and keeps underwriting profits when claims run lower than premiums collected.

Reinsurance-Backed Programs: You establish your own administrator-obligor warranty company, fund it through customer premiums, and retain underwriting profits. A reinsurance administrator (like WarrantyRE) handles setup, compliance, claims, and financials—but you own the entity.

The stakes behind that choice are significant. The U.S. home services market has reached $543 billion, with HVAC alone generating nearly $160 billion in revenue across approximately 116,000 contractors. Which model you choose determines whether your warranty program is an expense line or a profit source.

Best Home Service Contractor Warranty Companies

The companies below were selected based on program structure, contractor profitability, administrative completeness, compliance track record, and suitability across HVAC, roofing, plumbing, electrical, and general contracting trades.

WarrantyRE

Founded in 1994 and operating nationwide, WarrantyRE helps home service contractors establish and manage their own administrator-obligor reinsurance companies—eliminating third-party warranty providers entirely. Primary trades served include HVAC, roofing, plumbing, electrical, and general contracting.

Rather than paying premiums to an outside warranty company, contractors using WarrantyRE fund their own warranty entity backed by A-rated insurers. This structure lets contractors capture **100% of underwriting profits** and control the claims experience from start to finish. Retained premiums can also be invested for additional ROI.

WarrantyRE handles full-service administration: claims adjudication, IRS Code 831(b) compliance, tax filings, monthly financial statements, and staff training.

| Best For | HVAC, roofing, plumbing, electrical, and general contractors seeking to own their warranty program and recapture profits from third-party providers |

|---|---|

| Key Program Features | Admin-obligor reinsurance structure; full-service administration including claims, compliance, financials, and tax returns; fast company setup; training and onboarding support; A-rated insurance backing |

| Pricing Model | Transparent fee structure with no hidden costs; model built around contractor premium retention rather than monthly premiums paid to third parties—contact (804) 824-9533 for detailed pricing |

2-10 Home Buyers Warranty

Operating for over 45 years since 1981, 2-10 Home Buyers Warranty offers contractor-facing structural and systems warranty programs primarily for home builders and remodeling contractors. Programs are insurance-backed and transferable to homebuyers at closing. The company holds a BBB A+ rating and has warranted millions of homes nationwide.

Known for its compliance infrastructure and coverage of structural defects (1-2-10 year coverage tiers), 2-10 is a strong fit for general contractors and builders who need documented, transferable warranties that meet lender and real estate requirements. Coverage includes:

- 1-Year Workmanship and Materials: Roof covering, cabinets, countertops, siding, flooring, drywall

- 2-Year Systems: Behind-the-wall mechanical defects (piping, ductwork, electrical wiring)

- 10-Year Structural: Load-bearing elements, foundation, framing

HUD eliminated the FHA requirement for 10-year structural warranties on high-LTV new construction as of March 2019, so the value proposition has shifted from regulatory compliance to voluntary risk management and competitive differentiation.

| Best For | Home builders, remodeling contractors, and general contractors needing lender-accepted, transferable structural warranties |

|---|---|

| Key Program Features | 1-year workmanship, 2-year systems, 10-year structural coverage tiers; transferable to buyers; compliance documentation support; insurance-backed |

| Pricing Model | Quote-based pricing; builders must become members to access programs—contact 2-10 HBW directly for enrollment fees and per-home costs |

AmTrust Risk Solutions (Home Protection Division)

AmTrust Financial Services holds an A- (Excellent) AM Best rating with $8.8 billion in gross written premium and $27.1 billion in total assets. Its Home Protection division offers B2B2C service contract programs for home systems, appliances, and utility lines—this is the relevant entity for contractors, not the Warrantech brand, which covers automotive and powersports.

AmTrust functions as a fully external administrator. Contractors enroll, set retail pricing for customer-facing contracts, and AmTrust handles underwriting and claims. The company offers multiple partnership structures including reinsurance, profit share, and risk-sharing arrangements. This works well for contractors who want a ready-made product without building their own program, though underwriting profit margins remain with the provider under traditional models.

| Best For | HVAC and home systems contractors seeking a turnkey third-party warranty product with established underwriting infrastructure and financial strength |

|---|---|

| Key Program Features | Service contract administration; claims processing; regulatory compliance support; multi-trade coverage options; B2B2C model; multiple partnership structures (reinsurance, profit share, first dollar) |

| Pricing Model | Customized partner programs; commission and margin structures not publicly disclosed—contact AmTrust Risk Solutions for contractor pricing details |

Residential Warranty Corporation (RWC)

Residential Warranty Corporation has offered insured warranty programs to contractors and home builders since 1981, specializing in structural, mechanical, and systems warranties for new construction and major renovation projects. RWC has warranted over 4 million homes and is backed by Western Pacific Mutual Insurance Company, which holds an A- (Excellent) AM Best rating with over $130 million in surplus equity since 2001.

RWC programs are insurance-backed and designed to meet HUD, FHA, and VA requirements (historically—note that FHA no longer mandates 10-year plans), making them relevant for contractors working on new builds or government-financed projects. The company operates affiliate programs including HOME of Texas (Texas-specific compliance), MHWC (manufactured housing), Key Estates (resale home warranties), and RWC Insurance Advantage (commercial insurance).

Builders must become "Builder Members" to access programs. RWC describes membership as exclusive, requiring quality construction standards and a strong claims track record. Members can earn cash back for meeting quality benchmarks.

| Best For | Home builders and contractors on new construction or major renovations requiring government-accepted, insured structural warranties |

|---|---|

| Key Program Features | Insured structural warranty programs; 1-2-10 coverage tiers; transferable to homeowners; A- rated insurance backing; Warranty Express online portal; affiliate programs for specialized markets |

| Pricing Model | Quote-based pricing described as "economically-priced"; builders must qualify for membership—contact RWC for enrollment fees and per-home costs |

ProHome International

ProHome International has operated for over 40 years, providing homebuilder and contractor warranty and customer service management programs. The company combines warranty administration with structured customer care workflows, third-party inspections, and service request management—serving primarily residential contractors and production builders nationwide with highlighted presence in California and New York.

What sets ProHome apart is its per-unit pricing model: warranty management costs are passed through at closing by the title company. This converts warranty administration from a fixed overhead line item to a variable cost, eliminating staffing expenses for builders.

ProHome's services include:

- Full management of 1-year builder warranty claims

- 24/7 Client Relationship Coordinators as primary homeowner contact

- Pre-closing walks and new home orientation

- Emergency support (evenings, weekends, holidays)

- Subcontractor coordination and dispatching

- ProHomeLive CRM for claims, photos, and subcontractor performance tracking

- California SB 800 compliance and 11-year record archiving for legal defense

| Best For | Production builders and residential contractors seeking combined warranty administration and post-sale customer service management |

|---|---|

| Key Program Features | Warranty administration; customer care management systems; third-party inspection services; service request workflows; ProHomeLive CRM; CA SB 800 compliance; 11-year record retention |

| Pricing Model | Per-unit pass-through cost paid at closing by title company; no fixed overhead for builders—contact ProHome for per-unit pricing details |

How We Chose the Best Home Service Contractor Warranty Companies

Companies were evaluated based on how well they serve the contractor's business interests—not just the end customer. Many contractors evaluate warranty programs on coverage breadth alone, overlooking the direct impact on their bottom line and claims exposure.

Key selection factors included:

- Program model — Third-party vs. reinsurance-backed ownership structure

- Claims adjudication quality — Contractor control over outcomes and speed of resolution

- Compliance and legal administration — State filings, licensing, tax returns, regulatory coordination

- Onboarding and training support — Staff education and program implementation assistance

- Long-term profitability potential — Ability to capture underwriting profits and invest retained premiums

Beyond these core factors, contractors should assess proven track records (years in operation, industry memberships), account management responsiveness, and whether the provider's incentives align with contractor growth rather than their own underwriting margin.

Regulatory compliance is increasingly a deciding factor. State-level requirements are tightening, which raises the stakes for choosing a provider that handles compliance management in-house:

- Florida: Mandatory one-year statutory builder warranty effective July 1, 2025

- California SB 800: 14-day claim acknowledgment and 40-day inspection timelines

These requirements drive demand for third-party administration and directly benefit providers that specialize in regulatory coordination.

Conclusion

Choosing the right warranty company shapes a contractor's profitability, reputation, and customer retention for years. The right partner doesn't just protect customers — it protects the business behind them.

Before committing to a program, match the model to your business:

- High-volume contractors: An owned, reinsurance-backed program typically captures more profit than a third-party arrangement justifies over time

- Smaller operations or builders: Traditional third-party programs offer administrative simplicity and lender-accepted compliance infrastructure without the overhead of ownership

For contractors ready to stop paying profits to outside warranty companies and start building a warranty program they own, WarrantyRE offers a proven reinsurance model backed by over 30 years of experience. Reach out at (804) 824-9533 to explore whether owning your warranty company is the right move for your business.

Frequently Asked Questions

What is the best home service warranty?

The "best" warranty depends on perspective. For contractors, the best program protects customers while allowing the contractor to control claims, pricing, and profits. Reinsurance-backed programs like WarrantyRE's model offer contractors the most financial upside compared to third-party providers, where underwriting profits stay with the warranty company.

How do home service contractor warranty programs work?

Contractors either partner with a third-party warranty administrator or establish their own reinsurance-backed warranty company. In the reinsurance model, premiums collected from customers fund a contractor-owned reserve backed by A-rated insurance — claims draw from that reserve, and any unused premiums stay with the contractor.

What is the difference between a contractor warranty and a home warranty?

A contractor warranty is offered by the contractor directly on their work, installations, or systems—covering labor, callbacks, and installation defects. A home warranty is a consumer-purchased service contract covering multiple systems and appliances from a third-party provider. They serve different purposes and are structured differently.

How can contractors profit from offering a warranty program?

In a reinsurance-backed model, contractor-collected premiums fund a warranty reserve that the contractor owns. When claims run lower than premiums collected, the contractor retains the underwriting profit—plus investment income on reserves. Unlike third-party programs where that surplus stays with the provider, reinsurance structures let contractors capture 100% of underwriting gains.

What should contractors look for when choosing a warranty company?

Start by evaluating these six factors:

- Ownership structure — who keeps the underwriting profits

- Claims control — who approves and manages claims

- Administrative completeness — whether compliance, filings, and bookkeeping are included

- Profitability alignment — does the provider win only when you do

- Trade-specific coverage — options suited to your trade (HVAC, roofing, plumbing, etc.)

- Track record and financial backing — proven history with A-rated reinsurance support

What is an admin-obligor reinsurance warranty program for contractors?

In an admin-obligor model, the contractor forms their own warranty company backed by A-rated reinsurance — collecting premiums, administering claims, and retaining profits. A specialist like WarrantyRE handles setup, compliance, and day-to-day administration, so the contractor owns the entity without managing it directly.