Introduction

HVAC contractors invest heavily in customer warranties to build loyalty and differentiate their businesses—but many don't realize they're funding third-party companies' profits every time they sell a warranty plan. Those warranty providers wouldn't stay in business if they weren't making money from the premiums you collect. The question is: why should they capture those profits instead of you?

The cost environment makes this question urgent. HVAC equipment costs surged 5-12% annually across major manufacturers in recent years, with installed system costs rising approximately 58-75% from 2020 to 2026. Labor costs climbed 16.4% from 2021 to 2024, with median HVAC technician wages reaching $59,810 annually.

Meanwhile, approximately 120,000 HVAC contractors now compete for the same customers—making every margin point matter.

In that environment, how you structure your warranty program directly impacts profitability, cash flow, and long-term business value. This post examines two paths: staying with a third-party warranty company or establishing your own reinsurance program—so you can evaluate which model delivers better profit, control, and risk protection for your business.

TLDR

- Third-party warranty companies keep the underwriting profits—you do the sales work but see none of the margin

- Reinsurance lets HVAC contractors own their warranty company structure, backed by A-rated insurers

- IRC 831(b) tax advantages and investment income on reserves make reinsurance a genuine profit center

- Third-party programs are easier to start but cost you significantly more over time

- The right choice comes down to your installation volume and whether you want warranties to generate profit or just retain customers

HVAC Warranty Reinsurance vs. Third-Party Companies: At a Glance

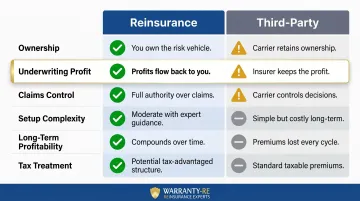

| Factor | Reinsurance | Third-Party |

|---|---|---|

| Ownership | Contractor owns the warranty company structure | External company owns the process |

| Underwriting Profit | Contractor keeps 100% | Third party retains all profit |

| Claims Control | Contractor controls claims decisions and customer experience | Third party controls adjudication and resolution |

| Setup Complexity | Higher initial involvement (handled by reinsurance partner) | Low friction, minimal setup required |

| Long-Term Profitability | Strong financial upside through profit retention and investment income | Minimal financial benefit beyond sales margin |

| Tax Treatment | Tax-advantaged structure under IRC 831(b) | No tax benefits for contractor |

| Backing | A-rated insurance carrier provides backstop | A-rated insurance carrier provides backing |

Both models carry A-rated insurance backing. The real difference is ownership: in a reinsurance structure, you keep the underwriting profit, control the claims experience, and build an appreciating asset — instead of handing that upside to a third party every year.

What is HVAC Warranty Reinsurance?

HVAC warranty reinsurance is a structure where you establish your own administrator obligor company—supported by A-rated insurance carriers—to take on warranty risk and capture underwriting profits from your customer base. Instead of paying those profits to a third party, you keep them.

The Admin Obligor Model

Under the admin obligor model, your company becomes the obligor on warranty contracts sold to customers. A-rated reinsurance carriers backstop the risk, protecting you from catastrophic claim events.

If your reinsurance company cannot meet obligations due to insufficient reserves, the insurance carrier covers the shortfall. Your personal liability is limited to formation costs plus accumulated earnings.

How Premium Dollars Flow

When customers pay warranty fees:

- Premiums are collected and flow into your reinsurance company (not a third party)

- A portion funds claims reserves managed in your reinsurance structure

- Remaining funds become underwriting profit that stays with your entity

- Investment income earned on reserves belongs to you

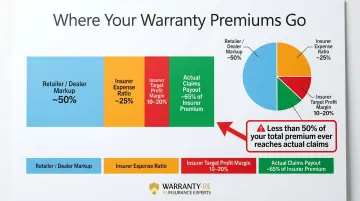

Third-party models work differently. Less than 50% of retail warranty prices go toward actual claims, with insurers targeting 10-20% profit margins. That gap is profit leaving your business every time a customer buys a warranty.

Tax Planning Advantages

Reinsurance structures operate under IRC Section 831(b), which allows qualifying small insurance companies to:

- Receive up to $2.8M in annual premiums with underwriting income tax-exempt

- Pay standard 21% corporate tax only on investment income

- Deduct premiums as business expenses under IRC Section 162

For HVAC contractors doing steady installation volume, this keeps money that would otherwise go to the IRS inside a tax-advantaged structure.

Investment Income on Reserves

Premium reserves are initially invested conservatively in government bonds. Once your balance sheet cash exceeds 125% of unearned premiums, excess funds may be invested more aggressively at your direction—generating additional ROI beyond underwriting profit.

Full-Service Administration

WarrantyRE specializes in helping HVAC contractors set up and manage reinsurance programs, providing:

- Training and onboarding for your staff

- Complete claims adjudication from first call to resolution

- Compliance management and regulatory filings

- Monthly financial statements and performance reports

- Legal filings, tax returns, and renewals

- Bookkeeping and accounting services

You don't need to become an insurance expert—you focus on installations while your reinsurance partner handles administration.

Use Cases of HVAC Warranty Reinsurance

Reinsurance works best for:

- Contractors already offering (or planning to offer) labor warranties on furnace, AC, heat pump, and mini split installations

- Businesses that want to fund warranty obligations through customer premiums rather than absorbing callback costs out-of-pocket

- Owners who want warranties to generate recurring revenue and long-term equity, not just serve as a customer perk

- Contractors who want direct control over the claims process and customer experience

There's no minimum volume requirement. WarrantyRE works with contractors of all sizes, starting with a brief business analysis.

What Are Third-Party HVAC Warranty Companies?

Third-party warranty companies are businesses HVAC contractors partner with to administer labor and parts warranty plans sold at installation. Providers like JB Warranties and Trinity Warranty handle compliance, claims, and legal structure—contractors simply sell the warranty and remit premiums.

How the Partnership Works

Typical engagement model:

- Contractor sells the warranty to the homeowner at installation

- Contractor remits premium to the third-party provider

- Provider handles all claims adjudication and compliance

- Provider reimburses contractor for covered repairs at predetermined rates (often up to $300/hour for labor)

The third party owns the warranty company structure. You're a sales channel for their product.

Real Advantages

Third-party programs offer legitimate benefits:

- Requires no company setup or upfront infrastructure

- Includes built-in compliance and legal framework

- Pays predetermined reimbursement rates for covered repairs

- Offloads all claims processing and administration

For smaller contractors or those new to extended warranties, that hands-off structure is a real operational advantage. The tradeoff shows up in where the money goes.

The Structural Limitation

The core problem is profit retention. Third-party companies keep all underwriting profit. According to industry analysis, extended warranty programs typically allocate premiums as follows:

- Approximately 50% retailer/dealer markup on dealer cost

- Approximately 25% insurer expense ratio

- 10-20% insurer target profit margin

- Approximately 65% of insurer premium goes to actual claims

Less than 50% of the retail warranty price goes toward actual risk and claims. If you do quality installations that generate low claims, the third party captures that financial upside entirely.

Use Cases of Third-Party HVAC Warranty Companies

Third-party programs make sense for:

- Contractors just starting to offer extended warranties who want minimal administrative overhead

- Businesses with lower install volume where reinsurance setup costs might not justify the profit capture

- Short-term solutions while building volume toward thresholds where reinsurance becomes financially meaningful

As install volume grows, however, the profit you're leaving on the table grows with it. That's where the comparison with reinsurance starts to matter.

HVAC Warranty Reinsurance vs. Third-Party: Which Model Should You Choose?

The decision hinges on three factors: install volume, growth mindset, and financial goals.

Choose Third-Party If:

- You're early in building a warranty program

- Install volume is low or inconsistent

- You want zero administrative overhead

- Warranties serve primarily as a customer satisfaction tool, not a profit center

- You prefer predictable costs and simple operations

Choose Reinsurance If:

- You have consistent or growing installation volume

- You want to capture underwriting profits your quality work generates

- You're interested in building long-term business equity

- You're willing to work with a reinsurance partner to manage back-end administration

- Tax planning advantages matter for your financial situation

Understanding the Financial Difference

The numbers make the difference concrete. Here's how the two models compare at the same volume:

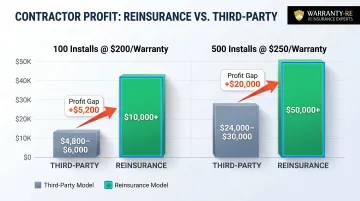

Scenario: 100 annual installations with $200 warranty fee per install

Third-Party Model:

- Total premiums collected: $20,000

- Contractor margin: 24-30% = $4,800-$6,000 (one-time sales commission)

- Underwriting profit (10-20% of premium): $2,000-$4,000 goes to third party

- Investment income on reserves: $0 for contractor

- Total contractor benefit: $4,800-$6,000

Reinsurance Model:

- Total premiums collected: $20,000 (flows into contractor's reinsurance company)

- Contractor retains: 100% of underwriting profit after claims and reserves

- If claims consume 50% ($10,000), contractor retains $10,000 in underwriting profit

- Investment income on reserves: Additional returns (contractor keeps this)

- Tax treatment: Underwriting income tax-exempt under 831(b)

- Total contractor benefit: $10,000+ (significantly higher long-term value)

The gap widens at higher volumes. A contractor running 500 installs annually at $250 per warranty captures $125,000 in total premiums — and under a reinsurance structure, retains the majority of that rather than passing underwriting profits to a third party.

Risk Control Advantage

Under reinsurance, you influence the claims experience directly:

- Quality installations reduce claim frequency

- Customer selection impacts loss ratios

- You control how claims are adjudicated

- Customer interactions reflect your brand standards

Under third-party models, claims adjudication and customer service sit entirely outside your control. When a claim goes sideways, it's your customer relationship on the line — handled by someone else's process.

Conclusion

Third-party warranty companies provide convenient structure, but they're built to capture the financial upside of warranty programs. For HVAC contractors who do quality work, that upside is real and recapturable through reinsurance.

A 2026 survey found that 58% of contractors already offer extended warranties, with those including warranties in total job pricing achieving 30% margins versus 24% for separate add-ons. The warranty market is maturing—the question is whether you pocket that margin or keep passing it to a third party.

WarrantyRE offers owner analysis consultations that model your installation volume, claims history, and profit retention potential—giving you a concrete picture of what reinsurance would return to your business. Call (804) 824-9533) to find out whether the numbers make sense for your operation.

Frequently Asked Questions

Is reinsurance only beneficial for large HVAC contractors, or can smaller contractors participate?

Reinsurance works across a range of business sizes. Smaller contractors with consistent install volume can still capture meaningful underwriting profits, particularly as their business grows. WarrantyRE evaluates each contractor individually rather than applying a blanket volume threshold.

How do HVAC contractors price labor warranties under a reinsurance model?

Contractors typically set warranty pricing based on their historical labor costs, call-back rates, and desired profit margin. Because you own the reinsurance structure, you control pricing — unlike third-party programs where the provider sets terms and retains the spread.

What is the difference between reinsurance and a third-party warranty company for HVAC contractors?

The difference comes down to ownership and profit retention. With reinsurance, you own the warranty company structure and keep underwriting profits. With a third-party program, an outside company owns the structure and keeps the profits — you earn only a sales margin.

How much install volume does an HVAC contractor need to justify setting up a reinsurance program?

Volume thresholds vary by provider and program structure. WarrantyRE has no minimum volume requirement and evaluates each contractor individually through an owner analysis. Contact a reinsurance partner to assess whether your current or projected volume supports the model financially.

What happens to warranty claims under a reinsurance model if the contractor's company can't cover them?

In an admin obligor reinsurance structure, an A-rated insurance carrier provides the financial backstop. If claims exceed reserves, the carrier absorbs the shortfall — your personal or business assets are not directly at risk beyond your formation costs and accumulated reinsurance earnings.

Can an HVAC contractor switch from a third-party warranty provider to a reinsurance program?

Yes, contractors can transition. Typically, new warranty contracts go through the reinsurance program going forward while existing third-party contracts run their course under original terms. A reinsurance partner like WarrantyRE can guide the transition timeline and process based on your specific contractual obligations and business goals.