Introduction

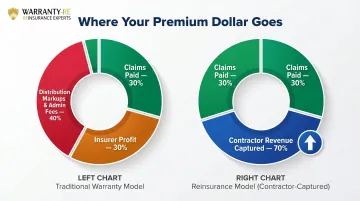

When a contractor sells a warranty through a third-party warranty provider, as little as 30 cents of every premium dollar goes toward actual claims. The remaining 70 cents flows to distributor markups, administrator fees, and third-party profits—none of which return to the contractor's bottom line.

For HVAC, roofing, plumbing, and electrical contractors, that gap represents thousands of dollars in lost profit on every job. The decision to keep funding a third party's balance sheet—or to capture those underwriting profits through a contractor-owned reinsurance company—directly shapes long-term profitability, claims control, and business valuation.

This guide breaks down how each model works, where the money goes, and which structure makes sense for your business.

TL;DR:

- Third-party warranties handle all admin but keep underwriting profits

- Contractor reinsurance captures those profits through company ownership

- Reinsurance requires setup but delivers compounding financial benefits

- The right choice depends on volume, goals, and appetite for control

- Most contractors running $1M+ in annual warranty volume have a viable path to reinsurance

Reinsurance vs. Third-Party Warranty Companies: Quick Comparison

| Dimension | Third-Party Warranty | Contractor Reinsurance |

|---|---|---|

| Profit Ownership | Third party keeps underwriting profits; contractor receives small commission | Contractor captures 100% of underwriting profits through owned reinsurance company |

| Claims Control | Third party manages all claims decisions and customer interactions | Contractor controls claims process, decisions, and customer experience |

| Setup Complexity | Minimal setup; no company formation or legal filings required | Requires reinsurance company formation; WarrantyRE handles legal filings, compliance, and onboarding |

| Tax Advantages | No contractor tax benefit; commissions taxed as ordinary income | IRC 831(b) election defers tax on premium income; investment income grows in reserve |

| Customer Loyalty | Disconnected warranty experience managed by external provider | Warranty integrates with contractor brand, reinforcing customer loyalty |

| Long-Term Value | Generates no equity or business asset for contractor | Builds an equity-generating business asset with accumulating reserves |

What is a Third-Party Warranty Company for Contractors?

A third-party warranty company is an external organization that sells, administers, and backs warranty products on behalf of contractors. The contractor recommends or sells the warranty to customers, but the third party collects premiums, manages all claims, and retains the underwriting profit—the money left over after claims are paid.

How the arrangement works:

The contractor acts as a distributor, selling the third party's warranty program to homeowners. Premiums flow directly to the warranty administrator, who may pay the contractor a commission (typically 10–20% of the premium) or a volume bonus. The bulk of the premium reserve—the funds set aside to pay future claims—stays with the third party.

According to NAIC research, distributor markups are often as high as 100% of the wholesale price, meaning contractors receive only a fraction of what their customers actually pay.

Core limitations for contractors:

- Claims decisions—approvals, denials, payout amounts—are made by the third party, not you, which can frustrate customers and damage your reputation

- Unused premium reserves stay with the provider, building their balance sheet instead of yours

- Pricing, coverage terms, financial stability, and customer service are entirely outside your control

Every premium dollar your customers pay that flows to a third party is underwriting profit you'll never see—profit that a reinsurance structure would let you keep.

What is Contractor Reinsurance?

Contractor reinsurance is a structure where the contractor establishes their own reinsurance company—specifically, an administrator obligor model—that sits behind a licensed, A-rated front insurer. The contractor's reinsurance company assumes the warranty risk and receives the premium reserves, capturing underwriting profit that previously went to third parties.

How the money flows differently

Customer premiums are collected when warranties are sold. A fronting insurer issues the policy and takes a fee (typically 6-10% of gross written premium), leaving 90-94 cents per dollar within the contractor's reinsurance entity. The remaining premium reserves flow into a trust account owned by the contractor's reinsurance company. Claims are paid from this trust; unused premiums become profit.

What the contractor actually owns and controls

The contractor owns:

- A separate legal entity structured under IRC Section 831(b) tax treatment

- Premium reserves held in a U.S.-based trust account, invested conservatively

- Authority to approve claims, manage customer experience, and maintain brand consistency

- Flexibility to design warranty terms that align with their service offerings

- Access to unused reserves and investment income once reserve thresholds are met

In a standard commission relationship, none of these elements belong to the contractor — the profit, the reserves, and the customer data all stay with the third party.

Understanding "administrator obligor"

In plain language, the administrator obligor model means the contractor's reinsurance company is supported by an A-rated insurer as a backstop. If the contractor's reinsurance reserves are insufficient to pay claims, the fronting insurer covers the obligation—ensuring customers are protected while the contractor retains the financial upside.

Reinsurance isn't just for large companies

Reinsurance works at smaller scales than most contractors expect. HVAC, roofing, plumbing, and electrical contractors of various sizes have entered these programs successfully. With a full-service partner like WarrantyRE handling company formation, regulatory filings, tax returns, and claims administration, contractors capture the financial benefits without managing the complexity themselves.

Reinsurance vs. Third-Party Warranty: Which is Better for Your Contracting Business?

Key decision factors

The right choice depends on:

- Volume of installs and service agreements per month - Higher volume accelerates reserve accumulation and profit capture

- Desire for claims control - Contractors who want to own the customer experience benefit from reinsurance

- Interest in tax planning and wealth accumulation - Reinsurance offers tax-advantaged premium accumulation under IRC 831(b)

- Long-term business asset goals - Contractors building enterprise value gain equity through reinsurance company ownership

Profitability trajectory over time

Under a third-party model, contractor earnings plateau at commission levels, typically 10-20% of premiums. Under reinsurance, contractors earn profit distributions from reserve accounts that grow with each install.

Casualty Actuarial Society research documents that retail-level extended service contract loss ratios can be as low as 30%. That means up to 70 cents of every premium dollar goes to distribution markups, administrator fees, and insurer profit. In a reinsurance structure, the contractor captures that underwriting profit directly.

As reserves accumulate, investment income adds a second revenue stream. With current money market yields above 5% and conservative bond portfolios yielding approximately 4-4.5%, these funds generate returns that belong entirely to the contractor's reinsurance company.

Claims control and customer satisfaction

Profitability isn't the only reason contractors switch models. Claims control matters just as much to long-term growth.

Third-party warranties create disconnected customer experiences. When homeowners call with warranty issues, they reach external adjusters who may deny claims or delay approvals, damaging the contractor's reputation in the process.

ACHR News reports that 7 percentage points of the 11% annual customer churn contractors experience stems from customers feeling the contractor didn't care enough about their business.

Contractor-owned reinsurance keeps warranty management in-house. The contractor, or their reinsurance partner, handles claims directly. That keeps the brand relationship intact and turns warranties into a retention tool rather than a source of friction.

Setup and administrative burden

Third-party programs:

- Minimal setup — just sign a dealer agreement

- Zero administrative responsibility

- Zero financial ownership

Contractor reinsurance:

- Initial company formation required

- Ongoing compliance and reporting

- Full financial ownership and equity building

The critical distinction: with a full-service partner like WarrantyRE, contractors don't handle compliance, filings, or bookkeeping independently. The partner manages company formation, tax returns, regulatory coordination, claims adjudication, and monthly financial reporting, so the administrative burden stays off the contractor's plate while the financial upside stays in their pocket.

Situational recommendations

Third-party warranties work best for:

- Very new contractors establishing service volume

- Low-volume operations not yet ready for reinsurance scale

- Contractors seeking to test warranty offerings before committing to ownership

Reinsurance makes sense for:

- Contractors ready to treat warranties as a profit center

- Owners focused on long-term wealth accumulation and business equity

- Operations focused on customer experience ownership and brand loyalty

- Contractors interested in tax-advantaged premium accumulation

Real-World Gains: What Contractors Capture by Owning Their Warranty Program

Profit recapture opportunity

With retail loss ratios as low as 30%, contractors using third-party programs forfeit up to 70% of premium value. On a $12,000 HVAC installation with a $500 warranty fee, only $150-$200 may ultimately fund claims. The remaining $300-$350 flows to distributors, administrators, and insurers — not back to the contractor who did the work.

In a contractor reinsurance structure, that $300-$350 stays in the contractor's trust account. Multiply this across hundreds of jobs annually, and the profit differential becomes substantial.

Investment income as a second revenue stream

Premium reserves sitting in a trust account can be invested in conservative government bonds and money market funds. With 10-year Treasury yields projected near 4.35% and money market funds yielding above 5%, a $200,000 reserve balance generates $8,700-$10,000 annually in investment income.

That's income generated by reserves you already collected — sitting in your company, compounding over time. Those returns flow to tax planning next.

Tax planning advantages specific to contractors

Unlike commissions, retained earnings in a reinsurance trust aren't immediately subject to income tax. Under IRC Section 831(b), qualifying reinsurance companies with annual gross premiums not exceeding $2.3 million pay tax only on investment income, not on premium income. This creates real tax deferral advantages.

Rather than writing large tax checks annually, contractors redirect funds into a structure that builds wealth while deferring taxation. Consult a qualified tax advisor to understand how this applies to your specific situation.

Scenario-based example

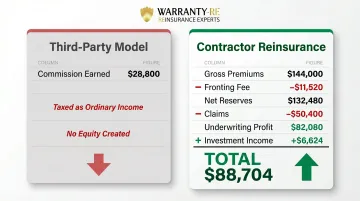

A mid-sized roofing contractor averaging 40 installations per month at $15,000 per job builds a $300 warranty fee into each contract. Annually, this generates $144,000 in warranty premiums ($300 × 40 × 12).

Under a third-party model:

- Commission earned: $28,800 (20% commission rate)

- Taxed as ordinary income immediately

- No equity created

Under contractor reinsurance:

- Premium reserves accumulated: $144,000

- Fronting fee (8%): -$11,520

- Net reserves: $132,480

- Claims paid (assuming 35% loss ratio): -$50,400

- Underwriting profit: $82,080

- Investment income (5% yield): +$6,624

- Total first-year gain: $88,704

- Equity created in reinsurance company

- Tax-deferred accumulation under 831(b)

Over five years, this contractor builds a reinsurance company with substantial reserve balances, equity value, and compounding investment returns—none of which exist under a third-party arrangement.

Stop funding a third party's profits. WarrantyRE can help you set up your own program from the ground up.

Conclusion

Contractors who are newer or lower-volume may benefit from starting with a third-party warranty program to establish the service line and test customer demand. This provides immediate administrative simplicity without capital commitment.

For contractors focused on profitability, customer experience, and long-term wealth building, reinsurance is the clearer path forward. Every month under a third-party warranty model, the underwriting profits your customers fund go directly to that provider's bottom line — not yours.

The tangible business outcomes contractor reinsurance makes possible include:

- Recurring revenue from warranty premiums and investment income

- Tax-advantaged accumulation under IRC 831(b)

- Direct claims control, which strengthens customer relationships and protects your brand

- Equity in your own reinsurance company — a genuine balance sheet asset

If your volume and goals support it, there's a straightforward question worth asking: why continue funding another company's profits when you could own the structure yourself? WarrantyRE has helped contractors make that shift since 1994 — handling setup, compliance, and administration so the transition doesn't add operational burden to your business.

Frequently Asked Questions

What is warranty reinsurance?

Warranty reinsurance is a structure where a reinsurance company—owned by the contractor—assumes risk behind a front insurer and receives premium reserves. This allows contractors to capture underwriting profits instead of paying them to third parties while customers remain protected by A-rated insurers.

What are the 4 types of reinsurance?

The four main types are proportional (quota share and surplus share) and non-proportional (excess of loss and stop loss). Contractor warranty programs most commonly use quota share reinsurance, where the contractor's company assumes an agreed percentage of each warranty's premium and claims obligation.

What are the four types of warranties?

The four common warranty types are manufacturer's warranty, extended warranty/service contract, implied warranty (automatic under state law), and workmanship warranty (a contractor's guarantee of quality). Contractor reinsurance programs most commonly apply to extended warranties and service agreements.

What are the 5 reasons insurers need to reinsure?

Insurers reinsure for risk transfer, capacity expansion, loss stabilization, capital relief, and regulatory compliance. Contractors use reinsurance for the same reasons—protecting against catastrophic claims while building profitable warranty programs.

Can a small contractor afford to set up their own reinsurance company?

Yes. Reinsurance is not limited to large contractors. Program costs vary based on structure and volume, but working with a full-service reinsurance partner like WarrantyRE significantly reduces administrative burden and initial complexity. The partner handles company formation, compliance, claims management, and financial reporting, making reinsurance accessible to contractors of various sizes.