That's a problem. A warranty reinsurance agreement isn't a formality. It's the document that determines who controls the reserve, who pays claims and when, and what happens if the relationship ends. The specific terms in that contract have direct financial consequences — and missing a single clause can mean losing access to funds you thought were yours.

This post breaks down the key terms in a warranty reinsurance agreement at the operational level: what they mean, why they exist, and what to watch for.

TL;DR

- A warranty reinsurance agreement governs how premium, risk, and claims obligations are split between the ceding party (you) and the reinsurer

- Core terms include cession language, unearned premium reserve provisions, claims obligations, representations, and termination rights

- Key clauses like the 9-month rule, 72-hour clause, and 60-day premium warranty provision directly control claim eligibility and fund access

- These agreements are negotiated, not standardized — terms can look very different from one provider to the next

- An experienced program administrator reviews these documents with you, so no critical clause gets missed

What Is a Warranty Reinsurance Agreement?

A warranty reinsurance agreement is a contract that defines the legal relationship between the party offering warranty coverage — the ceding company, typically the contractor or dealer's reinsurance entity — and the party assuming that risk, the reinsurer or fronting insurer.

As the Reinsurance Association of America defines it, reinsurance is a transaction in which the reinsurer agrees to indemnify the ceding company for all or part of the losses the ceding company may sustain under the policies it has issued. In a warranty context, that means the financial exposure from claims moves from a third-party provider into a structure the business owner controls.

The Customer Contract vs. the Reinsurance Agreement

That distinction matters practically, because the two documents serve entirely different purposes:

- The warranty contract is what the customer signs — it sets coverage terms, duration, and conditions

- The reinsurance agreement is the back-end structure that determines who holds premium reserves and who pays claims

WarrantyRE structures client programs using an administrator obligor model, where the contractor or dealer owns their reinsurance company outright. Funds ceded to that company are placed in a US-based trust account, with the Trust Company serving as Trustee.

The structure is backed by A-rated insurers. If the reinsurance company cannot meet its obligations, the direct writing insurance company steps in — and the business owner retains their reserve position throughout.

Why These Contract Terms Matter to Your Business

The terms inside a warranty reinsurance agreement aren't legal boilerplate. They determine:

- Who controls the premium reserve — and under what conditions you can access it

- How claims are adjudicated — and whether you're waiting for reimbursement or covered from the first call

- What happens at termination — including your obligations to in-force policies after the agreement ends

When these terms are poorly understood, the consequences are real. Business owners too often sign agreements that hand a third-party administrator unilateral control over reserves, restrict profit access to volume thresholds they may never hit, or leave them exposed to ongoing liability during a run-off period with no clear exit.

WarrantyRE handles all legal forms, filings, tax returns, and renewals on behalf of clients. Monthly financial statements and annual reports give clients continuous visibility into program performance — so reserve positions, claim trends, and profit distributions can be evaluated and acted on throughout the life of the agreement, not just at launch.

Core Contract Terms Explained

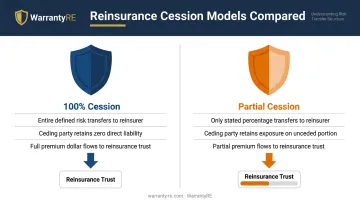

Cession Language

The cession clause defines exactly what risk is being transferred from the ceding party to the reinsurer. As IRMI explains, quota share reinsurance cedes an agreed percentage of every covered risk in the class of business subject to the treaty.

- 100% cession: The entire defined share of covered risk transfers to the reinsurer. The ceding party retains no direct liability if a claim is filed within that covered pool

- Partial cession: Only the stated percentage transfers. The ceding party retains exposure for the unceded portion

In practice, the cession percentage determines how much of each premium dollar flows into the contractor or dealer's reinsurance trust. This is one of the most financially significant clauses in the agreement, and one of the most commonly glossed over during review.

That cession percentage also drives how premiums are categorized once they arrive in the trust — which is exactly what the next clause governs.

Premium Reserve Provisions (Unearned Premium Reserve)

The UPR clause defines how collected premiums are categorized and when they shift from restricted to accessible.

Per NAIC Statutory Issue Paper No. 53, when written premium is recorded, a liability called the unearned premium reserve must be established for the portion of coverage that has not yet expired. The program recognizes premiums as income over the contract period, generally on a pro rata basis.

What this means in practice:

- Unearned premium reserve (UPR): Restricted funds covering active, unexpired warranty obligations. These pay claims and cannot be freely withdrawn

- Earned surplus: Funds that have moved beyond the UPR threshold. In WarrantyRE's structure, once balance sheet cash exceeds 125% of unearned premiums, excess funds may be invested more aggressively at the direction of company ownership

Before reaching that threshold, reserves are held in conservative government bonds as required by insurance regulatory standards. After crossing it, the business owner gains more investment flexibility — a meaningful financial distinction that the UPR clause directly governs.

Claims Obligations and Adjudication

This section of the agreement specifies who investigates, approves, and pays claims. The two common models:

- Pay-on-behalf: The reinsurer or program administrator pays covered claims directly, without requiring the ceding party to fund them first

- Reimbursement model: The ceding party pays claims out of pocket and then seeks recovery from the reinsurer, creating a timing gap that affects cash flow

WarrantyRE handles claims administration from first call to final resolution. No adjusters to track down, no claims calls to manage. This approach eliminates the reimbursement delay that can strain cash flow under other program structures.

Representations and Warranties of Parties

Both the ceding company and the reinsurer make binding legal representations in the agreement about their authority, compliance status, and the accuracy of information provided. These aren't ceremonial: breaches trigger indemnification obligations.

WarrantyRE structures programs to meet IRS standards under applicable code sections, working alongside CPAs and legal counsel throughout. Clients should understand that their own representations — about business operations, licensing, and premium data — carry the same legal weight.

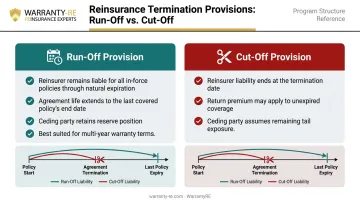

Termination and Duration Clauses

These terms define how long the agreement remains in force and what happens to active warranty obligations if it ends. Under a run-off provision, the reinsurer remains liable for losses under reinsured policies that were in force at termination. The agreement's effective life extends to the last covered policy's expiration, which can be years after the formal end date.

Some agreements use cut-off language instead, where the reinsurer's liability ends at termination and unexpired coverage may result in a return premium to the ceding party. The distinction between run-off and cut-off is one of the most consequential, and least-discussed, terms in the agreement.

Audit Rights and Recordkeeping

The audit clause gives both parties the right to examine records, verify claim data, and review performance reports. For the contractor or dealer, this is a protective mechanism — it ensures transparency in how reserves are managed and how claims experience is tracked.

WarrantyRE provides monthly financial statements detailing all reinsurance operations activity, plus annual reports prepared for tax and compliance purposes. The program administrator also meets with owners periodically to review financial direction. These reporting structures are the practical expression of what the audit clause protects.

Specific Clauses Found in Warranty Reinsurance Agreements

Minimum Contract Terms

Most reinsurance agreements include a minimum term provision — typically one to three years — that prevents early withdrawal without penalty. These minimums exist because the reserve structure needs time to reach the volume required to pay claims and generate underwriting profit. Before committing, ask:

- What is the minimum term, and what triggers the penalty for early exit?

- Is the term tied to the warranty program duration or the reinsurance agreement independently?

- What constitutes a default that could accelerate the termination date?

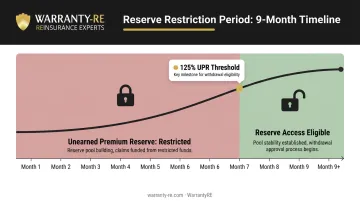

The 9-Month Rule

The 9-month rule restricts access to unearned premium reserves during the first nine months a warranty policy is active. A new reserve pool needs time to build before any portion is accessible — drawing it down too early creates solvency risk for the entire pool, including the business owner whose claims depend on it.

In WarrantyRE's structure, reserve access is governed by the Trust Agreement, with withdrawals requiring underwriting insurer approval. The 9-month rule acts as the front-end control on that process.

The 72-Hour Clause

In warranty reinsurance, a 72-hour clause typically requires that a covered event or claim be reported within 72 hours of occurrence or discovery. As IRMI notes, a ceding insurer's failure to provide prompt notice to the reinsurer may give the reinsurer a defense to coverage — and the outcome depends heavily on specific contract wording and governing law.

Missing the reporting window doesn't automatically void a claim in every jurisdiction, but it creates grounds for denial or reduced reimbursement. Before signing, confirm the exact reporting window in your agreement and verify your claims process can consistently meet it.

The 60-Day Premium Warranty Clause

This clause requires that premiums be remitted to the reinsurer within 60 days of the policy effective date. Public reinsurance agreement examples — including SEC-filed reinsurance exhibits — confirm that if premiums are not paid within the specified window, the reinsurer typically has the right to terminate coverage for policies in arrears.

Exposure from late remittances varies by contract wording and governing law, but the risk is real. Build premium remittance into your administrative calendar as a fixed deadline — not a flexible one.

Run-Off and Cancellation Provisions

Run-off and cancellation clauses govern what happens to active warranty obligations when the reinsurance agreement ends. Key considerations:

- Run-off: Reinsurer remains liable for in-force policies through natural expiration

- Cut-off: Reinsurer's liability ends at termination; ceding party may receive return premium for unexpired coverage

- Reserve distribution: Who holds remaining funds, and under what conditions can they be released?

These provisions are especially important for contractors with multi-year warranty terms. A 5-year labor warranty sold in year one of a reinsurance agreement could still carry claim exposure years after the agreement itself has ended. The run-off clause determines who covers that tail.

Common Misconceptions and Red Flags to Watch For

Misconception: All Warranty Reinsurance Agreements Are Standardized

They aren't. The RAA is explicit that reinsurance contracts are negotiated based on business needs — terms, conditions, and costs are set between the parties. IRMI notes that reinsurance contracts often contain archaic terms, industry jargon, and legalese that require careful reading. Two programs from different providers can look similar on the surface and carry very different terms underneath.

Misconception: The Ceding Party Has Full Access to Reserves at Any Time

UPR funds are restricted by regulatory and insurer guidelines. Confusing unearned premium with earned surplus leads to cash access assumptions that don't hold.

In WarrantyRE's structure, the 125% UPR threshold must be exceeded before excess funds become available for more flexible investment. All withdrawals also require underwriting insurer approval.

Red Flags to Watch For

Before signing any reinsurance agreement, flag these:

- Unilateral cancellation rights given to the administrator without defined cause or notice periods

- Profit participation thresholds controlled entirely by the third party — you only earn when they decide you've qualified

- Missing audit rights that leave you with no independent visibility into how your reserves are managed

- Vague run-off language that doesn't specify who is responsible for in-force claims or how remaining reserves are distributed

- No monthly reporting — if the agreement doesn't require regular financial statements, reserve transparency is at the administrator's discretion

Frequently Asked Questions

What are the minimum contract terms for warranty reinsurance?

Minimum terms typically range from one to three years, depending on the program structure and underlying warranty durations. These minimums exist to ensure the premium reserve reaches the volume needed to cover claims and generate underwriting profit before any distribution is permitted.

What is the 9-month rule in warranty reinsurance contracts?

The 9-month rule restricts access to unearned premium reserves during the first nine months a warranty policy is active. It protects the reserve pool from being drawn down before a sufficient claims history has developed and the reserve has reached a stable funding level.

What is the 72-hour clause in warranty reinsurance?

The 72-hour clause requires that covered events or claims be reported within 72 hours of occurrence or discovery. Missing this window can give the reinsurer grounds to deny or reduce reimbursement for that claim, depending on the contract wording and applicable jurisdiction.

What is the 60-day premium warranty clause in reinsurance contracts?

Premiums must be remitted to the reinsurer within 60 days of the policy effective date. Non-compliance can result in the reinsurer terminating coverage for affected policies or denying reinsurance recovery for that period.

What happens if a warranty reinsurance agreement is terminated early?

Early termination typically triggers a run-off period during which the reinsurer remains obligated for in-force claims, but new policies may no longer qualify for coverage. The termination clause governs how remaining reserves are held or distributed and who bears responsibility for the claims tail.

What is a cession in a warranty reinsurance agreement?

A cession is the formal transfer of a specified portion of warranty risk, along with the associated premium, from the ceding company to the reinsurer. The cession percentage determines how much of each premium dollar flows into the contractor or dealer's reinsurance trust — and how much risk transfers away from the business owner.