Get the documents right and you own a profitable, compliant company. Get them wrong and you face IRS scrutiny, regulatory penalties, or an inability to pay claims.

This guide covers the complete document picture: formation paperwork, the reinsurance agreement and fronting carrier contracts, regulatory filings, and the ongoing operational records that keep a program running profitably over time.

TL;DR

- A warranty reinsurance program requires two categories of documents: setup/formation and ongoing operational

- Formation documents include entity paperwork, EIN, IRS tax election forms, and state registrations

- The reinsurance agreement itself governs premium flow, cession, claims handling, and trust account rules

- Ongoing records (cession statements, claims files, financials) are required for both compliance and profitability

- Missing or outdated documents can trigger IRS penalties, regulatory violations, or a lost fronting carrier relationship

What Is a Warranty Reinsurance Agreement and Why Do Documents Matter?

In a standard third-party warranty arrangement, a contractor or dealer sells coverage and sends the premium to someone else's company. That company pays claims and keeps the underwriting profit.

A warranty reinsurance program flips that model. The contractor or dealer forms their own company (the admin obligor) which acts as the reinsurance entity on those same warranty products. An A-rated fronting insurer underwrites and issues the policy to the end customer, then cedes the risk back to the owner's company. According to the NAIC, fronting means a primary insurer issues the policy of record and passes the entire risk to a reinsurer for a commission. The contractor's company captures what was previously someone else's profit.

Why Documentation Is Non-Negotiable Here

This structure involves a regulated insurance entity, IRS-recognized tax elections, trust accounts, and ongoing state compliance obligations. That's a different category of commitment entirely from signing a vendor contract.

Missing or incomplete documents create real exposure:

- Tax risk — improper or late IRS filings for the 831(b) election can invalidate the tax treatment

- Regulatory violations — state insurance departments impose fines for late or missing filings; Hawaii, for example, levies fines up to $500 per day, capped at $10,000 per violation

- Claims exposure — if trust account documentation is incomplete, the program may not be able to satisfy its reserve requirements

Every contractor entering this structure needs to track two distinct phases: setup/formation documents required before launch, and ongoing operational documents that keep the program compliant and profitable long-term.

Business Formation Documents for Your Reinsurance Company

Before a single warranty premium flows into your reinsurance company, the entity must be properly formed and documented. These are the foundational records.

Articles of Incorporation or Organization

This document legally establishes your reinsurance entity — its name, state of domicile, registered agent, and ownership structure. The specific entity form (LLC, corporation, or other) depends on the chosen structure. WarrantyRE helps clients establish admin obligor reinsurance companies that can be domiciled domestically or offshore, with all assets held in US custodial accounts.

Popular captive domiciles include Vermont, Delaware, Tennessee, South Carolina, and Hawaii, each with different capital requirements and filing schedules.

Operating Agreement or Corporate Bylaws

These internal governance documents define how the company is managed, how profits are distributed, who has signing authority, and how decisions are made. They're critical for legal protection during audits and for establishing clear ownership rights at distribution time.

EIN and IRS Tax Election Forms

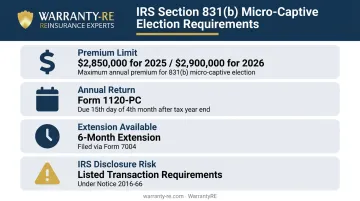

Your reinsurance entity needs its own federal Employer Identification Number. If the program is structured under IRS Section 831(b), a timely tax election must be filed.

Key 831(b) details:

- Premium limit is $2,850,000 for 2025 and $2,900,000 for 2026

- The annual return filed is Form 1120-PC, due the 15th day of the 4th month after tax year end

- A 6-month extension is available via Form 7004

- IRS Notice 2016-66 and 2025 final regulations identify certain micro-captive structures as listed transactions requiring disclosure — proper documentation is essential

State Registration and Business Licenses

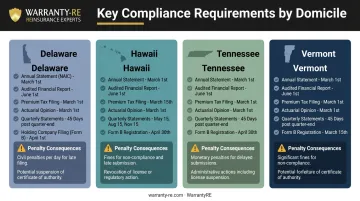

Depending on the domicile and structure, the reinsurance company may need a certificate of authority, state registration, and applicable business licenses. Filing deadlines vary by state. For example, Delaware's captive program requires:

- Corporate annual report by March 1

- Premium taxes by April 15

- Audited financials by June 30

Tennessee typically processes complete applications in about 30 days. WarrantyRE manages all legal forms, filings, tax returns, and renewals for clients — from initial setup through ongoing compliance.

The Reinsurance Agreement Itself: Key Documents and Terms

Once the entity is formed, the contractual layer of the program gets documented through a set of interconnected agreements. These documents govern how money flows, how risk is shared, and who handles claims.

The Reinsurance Treaty

This is the master contract between your reinsurance company and the fronting insurance carrier. It specifies:

- Which warranty products are being reinsured

- What percentage of risk is ceded

- How premiums flow into the trust account

- How claims are handled and approved

The treaty's terms directly determine how profitable the program is. It's a negotiated document, not a standard form, and the specifics carry real financial weight.

Fronting Carrier Agreements and CLIP Policies

The fronting insurer underwrites the warranty product, issues the policy to the end customer, and then cedes risk back to the contractor's reinsurance company. For dealer-owned warranty programs, this often includes a Contractual Liability Insurance Policy (CLIP) — a reimbursement policy that backstops the obligor's ability to pay claims.

Washington State's service-contract application identifies the CLIP as the instrument used to satisfy reimbursement insurance requirements. Texas similarly regulates CLIPs covering service contract and vehicle protection product obligations.

WarrantyRE's admin obligor structure is backed by A-rated insurers. If the reinsurance company cannot meet its obligations, ultimate liability rests with the direct writing insurance company.

Trust Account Documents

Unearned premium reserves must be held in a regulated trust account. The Trust Agreement is executed between three parties: the direct underwriting insurance company, the reinsurance company (owned by the contractor), and the Trust Company.

Key trust account rules:

- Funds are held at a US Trust Company — no funds go offshore

- Withdrawals are permitted for only four purposes: claim payments, limited professional fees, income taxes, and excess reserves above required levels

- Any withdrawal requires the underwriting insurance company's approval

- Once the account exceeds 125% of unearned premiums, excess funds may be invested more aggressively at the owner's direction

NAIC Model 685 requires a funded reserve account of at least 40% of gross consideration received, less claims paid, plus a security deposit of at least 5% of gross consideration with a $25,000 minimum.

Third-Party Administrator Agreement

WarrantyRE acts as the full-service administrator for its clients' programs, handling pricing, contracting, premium collection, cancellations, and claims adjudication. The administration agreement defines:

- Scope of services

- Fee structure

- Reporting obligations and frequency

- Data ownership

Clients receive full administrative coverage — WarrantyRE handles adjusters, claims paperwork, and program reporting so owners stay focused on running their business.

Regulatory Filings and Compliance Documentation

State Insurance Department Filings

Requirements vary significantly by domicile and structure type:

| Domicile | Key Deadlines | Penalties |

|---|---|---|

| Delaware | March 1, April 15, June 30 | Immediate upon missed deadline |

| Hawaii | March 1, April 1, 6 months after FY end | Up to $500/day, max $10,000/violation |

| Tennessee | March 15 annual report | Minimum capital via LOC or SACA |

| Vermont | March 1 financial condition report | Class-specific capital minimums |

Missing these deadlines does more than generate fines. It can jeopardize the fronting carrier relationship and the program's legal standing entirely.

Annual Tax Returns and Financial Statements

The reinsurance entity files its own annual tax return (Form 1120-PC) prepared by an insurance tax expert. Financial statements serve two purposes:

- IRS compliance — satisfying annual tax reporting requirements

- Proof of solvency — required by state regulators and fronting carriers

WarrantyRE prepares monthly financial statements and annual reports, coordinating with appointed tax preparers.

Compliance Calendar and Renewal Filings

Registrations, licenses, and fronting carrier appointments require annual renewal. A missed filing can create a lapse in the program's legal standing, often without any immediate notice. That silent exposure is why compliance calendar management is the most commonly overlooked risk in reinsurance administration.

WarrantyRE manages this calendar internally. Clients don't track their own compliance deadlines.

Ongoing Operational and Financial Records

Cession Statements and Performance Reports

These reports — typically generated monthly — show premiums collected, claims paid, reserves held, and surplus earned. They're required for tax filing, regulatory compliance, and monitoring program health. WarrantyRE prepares monthly financial statements detailing all reinsurance operations activity and meets with program owners quarterly to review performance trends and financial positioning.

Claims Adjudication Records

Every claim processed must be documented. Required records include:

- Service request and diagnosis documentation

- Parts and labor costs

- Approval or denial records and reasoning

- Payment confirmation

NAIC Model 685 requires claim files to be retained for at least 3 years after coverage expires. WarrantyRE handles claims from first call to final resolution — no extra paperwork for the contractor.

Premium Collection and Cancellation Records

As contracts are sold, renewed, or cancelled, accurate records of premium inflows and pro-rata refunds must be maintained. These feed directly into unearned premium reserve (UPR) calculations and trust account balances. Miscalculations here can throw off reserve balances and trigger compliance gaps at audit time.

Claims Administration Documents

What Documents Are Needed for a Warranty Claim?

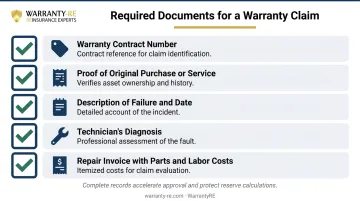

Your reinsurance program needs clean, consistent claim records from every service event. When a customer files a warranty claim, the program must collect:

- Warranty contract number from the original sale

- Proof of original purchase or service (invoice or installation record)

- Description of the failure and when it occurred

- Technician's diagnosis documenting the defect

- Repair invoices showing parts and labor costs

The completeness of these records determines how quickly claims are approved. Incomplete documentation slows adjudication and puts trust account reserve calculations at risk.

Organized claims records also serve a second purpose for your program: they give WarrantyRE the data needed to track loss ratios, flag patterns of miscoding or abuse, and keep reserve calculations accurate — directly protecting your profitability over the life of the program.

Frequently Asked Questions

What documents are needed for a warranty claim?

Within a contractor-owned reinsurance program, claims typically require the original service agreement, a documented repair record or technician report, and the corresponding invoice submitted to the program administrator. Requirements vary by program structure and the type of warranty product — your administrator specifies the exact process during setup.

What is the difference between a warranty reinsurance agreement and a standard warranty contract?

A warranty contract is the consumer-facing coverage document given to the homeowner or vehicle buyer. A reinsurance agreement is a business-to-business contract between the contractor's or dealer's reinsurance company and the fronting insurer, governing how risk and profit are shared at the company level.

Do I need an attorney to set up a warranty reinsurance company?

An attorney familiar with insurance structures is advisable for reviewing key agreements. Contractors working with a full-service administrator like WarrantyRE find that legal filings, entity formation, and ongoing compliance are handled directly, reducing reliance on outside counsel for day-to-day operations.

How long does it take to complete the documentation for a warranty reinsurance program?

Timelines vary by structure and state of domicile. Tennessee typically processes complete applications in about 30 days; Delaware offers conditional certificates on an expedited basis. A full-service administrator with established templates and filing processes compresses that timeline further.

What happens if my reinsurance documentation is incomplete or out of compliance?

Gaps in documentation can lead to regulatory fines, loss of the fronting carrier relationship, inability to pay claims from the trust account, or IRS scrutiny of the tax election. Accurate, current records are what keep the structure legally and financially intact throughout the program's life.

Can a contractor in any state set up a warranty reinsurance company?

Reinsurance programs are available nationwide, but the specific entity structure, state of domicile, and regulatory requirements vary. The reinsurance company itself may be domiciled in a different state than where the contractor operates. Working with a partner who understands multi-state compliance ensures the domicile election, filing requirements, and ongoing obligations stay aligned — regardless of where the contractor operates.