This guide covers the U.S. regulatory framework for warranty reinsurance, the specific compliance requirements for contractor-owned programs, common mistakes that create costly problems, and how the admin-obligor structure simplifies the compliance picture considerably.

Written for HVAC companies, roofing contractors, plumbing and electrical contractors, auto dealers, and any business owner running or evaluating a contractor-owned warranty reinsurance structure.

TL;DR

- Warranty reinsurance in the U.S. is regulated at the state level, with your domicile state holding primary compliance authority

- Contractor-owned programs must meet licensing, capitalization, filing, and solvency requirements to stay in good standing

- The admin-obligor structure reduces direct licensing burden by anchoring your program to a licensed, A-rated insurer

- Non-compliance can trigger loss of reinsurance credit, fines, and forced restructuring

- WarrantyRE manages your filings, tax returns, renewals, and compliance — so your program stays current without the administrative burden

What Is Warranty Reinsurance Compliance?

Warranty reinsurance compliance is the set of legal, financial, and administrative obligations a warranty reinsurance entity must fulfill to legally operate in the United States. Those obligations span entity formation, licensing, capitalization, ongoing reporting, and solvency standards.

The regulatory focus here differs from traditional consumer insurance. Because the contract sits between your reinsurance entity and a ceding insurer (not directly with a homeowner or car buyer), regulators concentrate primarily on financial solvency and proper entity structure rather than consumer-facing policy terms.

Two distinct compliance layers apply here:

- Provider/obligor compliance — governed by state service contract laws, covering the entity that is contractually obligated to the warranty holder

- Reinsurance compliance — governed by credit for reinsurance rules, covering whether the ceding insurer can record a statutory accounting benefit from the reinsurance arrangement

Confusing these two layers is one of the most common mistakes business owners make when setting up contractor-owned programs.

Getting the structure right is only half the equation. Compliance is an ongoing obligation, not a one-time setup task. Initial requirements — entity formation, capitalization, domicile registration — are followed by annual obligations: financial statement filings, tax returns, renewal submissions, and performance reporting. The structure you choose and the states where you operate determine exactly what those obligations look like.

How the U.S. Regulatory Framework Applies to Warranty Reinsurance

No Federal Regulator — State Law Controls

The U.S. has no single federal regulator for reinsurance. The McCarran-Ferguson Act of 1945 established that insurance — including reinsurance — is primarily regulated by the states, with each state maintaining its own insurance department and compliance standards.

A federal layer was added through the Dodd-Frank Act's Non-Admitted and Reinsurance Reform Act (NRRA), which clarified a key rule: a reinsurer's domiciliary state is the sole regulator of its solvency when that state is NAIC-accredited or substantially similar. For contractors operating across multiple states, this means the state where you form your reinsurance company governs its solvency supervision. Domicile selection is a strategic decision with real compliance consequences.

The NAIC's Role

The National Association of Insurance Commissioners (NAIC) doesn't hold direct regulatory authority, but its model laws are widely adopted by states and effectively set the national baseline.

As of October 2022, the 2019 revisions to NAIC Credit for Reinsurance Models #785 and #786 have been implemented across all 56 U.S. jurisdictions. These standards are the practical compliance floor for any warranty reinsurance structure operating in the U.S.

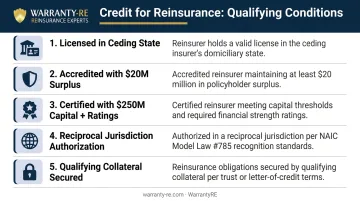

Credit for Reinsurance: The Gatekeeper Mechanism

Model Law #785 — one of those adopted standards — defines the most operationally important compliance concept: credit for reinsurance. A ceding insurer can only record the financial benefit of a reinsurance arrangement on its statutory books when the assuming reinsurer meets one of the following conditions:

- Licensed in the ceding insurer's state

- Accredited (with policyholder surplus of at least $20 million)

- Certified (requiring at least $250 million in capital and surplus plus ratings from two acceptable agencies)

- Authorized under a reciprocal jurisdiction arrangement

- Secured with qualifying collateral (cash, NAIC-listed securities, or letters of credit)

If your reinsurance entity doesn't satisfy one of these conditions, the ceding or reimbursement insurer cannot take credit — which eliminates the financial accounting benefit of the entire arrangement.

Key Compliance Requirements for Contractor-Owned Warranty Programs

Licensing and Entity Formation

Forming a contractor-owned warranty reinsurance company starts with establishing a legal entity and meeting the domicile state's requirements. Requirements vary considerably by structure:

- Dealer-Owned Warranty Company (DOWC) — operates as a non-licensed obligor, with financial responsibility typically backed by a reimbursement insurance policy

- Controlled Foreign Corporation (CFC) — a foreign reinsurer majority-owned by a U.S. shareholder, subject to specific IRS Subpart F income rules

- Admin-obligor structure — the contractor's entity serves as administrator and obligor, backed by a licensed A-rated carrier that absorbs the primary licensing obligations

Domicile state capital minimums vary. Published statutory figures from verified state sources include:

| State | Pure Captive Minimum | Notes |

|---|---|---|

| Arizona | $250,000 | ARS §20-1098.03 |

| Montana | $250,000 | MCA §33-28-104 |

| South Carolina | $250,000 | Title 38, Chapter 90 |

These are captive-insurer minimums, not universal warranty reinsurance thresholds — your specific structure and domicile will determine the exact figure.

Ongoing Filing and Reporting Obligations

Standard recurring obligations for a reinsurance entity include:

- Annual statutory financial statements (NAIC Property/Casualty Annual Statement Blank format where applicable)

- Actuarial opinions where required by domicile state

- Premium tax returns (Montana-domiciled captives, for example, must file by March 1 each year)

- Audited financial statements (Montana requires submission by June 30 for non-RRG captives)

- Renewal of registrations and entity standing

Missing these deadlines can result in loss of credit for reinsurance status, state fines, or administrative dissolution of the reinsurance entity.

Tax Compliance

Filing obligations are only part of the picture. Warranty reinsurance structures — particularly CFCs and offshore entities — carry federal tax obligations that catch many contractors off guard:

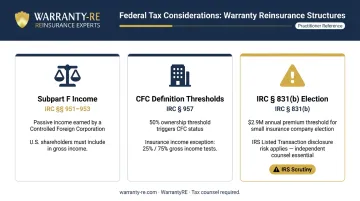

- Subpart F income rules (IRC §§951-953) require U.S. shareholders of controlled foreign corporations to include insurance income in gross income, even if not distributed

- A CFC is generally defined under IRC §957 as a foreign corporation where U.S. shareholders own more than 50% — though a special insurance income rule applies at 25% ownership when more than 75% of gross premiums are from insurance or reinsurance

- IRC §831(b) allows P&C insurers with under $2.9 million in annual net premiums to elect taxation on investment income only — but IRS final regulations (January 14, 2025) classify certain micro-captive arrangements as listed transactions that require disclosure

Tax counsel with insurance company experience is a required part of running these structures, not an optional add-on.

Common Compliance Mistakes That Can Cost You

Choosing the Wrong Structure

Selecting a program structure without evaluating your state's requirements, your warranty contract volume, your loss ratios, and your tax situation creates compliance gaps that are expensive to fix after formation. A structure that works well for a high-volume auto dealer may be wrong for a regional HVAC company — and restructuring after the fact typically costs more than getting it right at the start.

Missing Annual Deadlines

Annual filings, premium tax returns, license renewals, and financial disclosures all carry hard deadlines. A single missed filing can:

- Eliminate the ceding insurer's ability to take credit for reinsurance

- Trigger state fines or penalties

- Result in administrative dissolution of the reinsurance entity

There is no grace period for "we didn't know." The obligation exists from the moment the entity is formed.

Underestimating Multi-State Complexity

Contractors operating across multiple states face layered obligations. Each state where a warranty product is sold may impose its own service contract registration requirements, financial responsibility rules, or reimbursement insurance mandates — separate from where your reinsurance entity is domiciled.

State-level requirements vary significantly. For example:

- New York requires service contract providers to register with DFS before selling a single contract

- California requires a Vehicle Service Contract Provider license

- Washington has its own financial reporting requirements for service contract providers

These obligations stack on top of your reinsurer's domicile compliance — not in place of it. Missing either layer creates exposure.

The Admin-Obligor Structure: Built-In Compliance Advantages

The admin-obligor structure is the compliance-friendliest path for most contractors and dealers entering warranty reinsurance for the first time.

Here's how it works: the contractor's reinsurance entity serves as both the administrator and the obligor of the warranty contract. An A-rated, licensed insurance carrier backs the program and carries the primary regulatory and solvency obligations. The contractor captures the underwriting profits; the carrier provides the regulatory foundation.

Why this matters for compliance:

- The A-rated carrier is already licensed and compliant in applicable states, so the contractor's entity doesn't need to independently satisfy every state's full licensing framework

- The carrier's authorization satisfies the reimbursement insurance requirement under service contract laws like NAIC Model #685

- Credit for reinsurance mechanics are built into the structure rather than requiring independent certification or collateral arrangements

The A-rated carrier backing is a structural compliance mechanism, not just a financial buffer. The carrier's authorization is what allows the reimbursement insurance relationship to function under state service contract laws. The ceding relationship between the carrier and the contractor's reinsurance entity is what governs credit for reinsurance treatment.

WarrantyRE's admin-obligor model is built around this architecture. The contractor owns the profits and controls the program. The insurer partnership provides the regulatory foundation, while WarrantyRE's administration handles the ongoing compliance work: filings, tax returns, renewals, claims adjudication records, and financial reporting.

Managing Ongoing Compliance Without Losing Focus on Your Business

What Ongoing Compliance Actually Looks Like

For a contractor-owned warranty reinsurance company, recurring compliance obligations across a program year typically include:

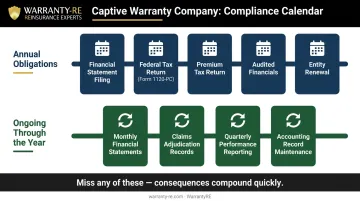

Annual obligations:

- Annual financial statement preparation and filing with the domicile state regulator

- Federal income tax return (Form 1120-PC for property and casualty insurance companies)

- Premium tax return filing (deadline varies by domicile — March 1 in Montana)

- Audited financial statements where required

- Entity renewal and registration maintenance

Ongoing through the year:

- Monthly financial statement preparation covering all reinsurance activity

- Claims adjudication records and documentation

- Quarterly performance reporting and analysis

- Maintenance of accounting records sufficient to support annual filings

Miss any of these, and the consequences compound quickly. A late premium tax filing can trigger fines. An incomplete financial statement creates problems with your domicile regulator. Gaps in claims documentation create exposure in an audit.

The Case for Full-Service Administration

That compliance burden falls squarely on contractors — HVAC companies, roofers, auto dealers — for whom insurance regulatory work sits well outside their daily operations. Tracking deadlines, preparing filings, and maintaining clean records can consume dozens of hours per year. More importantly, errors and missed deadlines put the entire program at risk.

A qualified reinsurance administrator handles those obligations so contractors don't have to. WarrantyRE has managed full-service compliance administration for contractor-owned and dealer-owned programs since 1994, handling all legal forms, filings, tax returns, and renewals on behalf of program owners. Their team works with specialized CPAs and legal counsel who understand insurance company taxation and state regulatory requirements specifically — professionals with direct experience in reinsurance structures, not general business accountants learning on the job.

That means contractors stay focused on installations, service calls, and customer relationships — while the filing deadlines, tax returns, and regulatory reporting get handled by people who do this every day.

Frequently Asked Questions

What is a warranty in reinsurance?

In contractor warranty reinsurance programs, a "warranty" describes the arrangement where the contractor's reinsurance entity assumes the financial risk of warranty obligations sold to customers. Instead of paying underwriting profit to a third-party provider, the contractor retains it through their own structure.

What states regulate warranty reinsurance companies?

All U.S. states regulate reinsurance at the state level, but the domiciliary state of the reinsurance entity carries the primary compliance authority. The state where your reinsurance company is formed governs its solvency standards, filing requirements, and capital minimums — making domicile selection one of the most consequential decisions in program setup.

Do I need a license to run my own warranty reinsurance company?

Licensing requirements depend on the structure chosen. The admin-obligor model allows a contractor to operate within the regulatory umbrella of an A-rated carrier, significantly reducing independent licensing obligations. Other structures — such as a CFC or directly licensed domestic reinsurer — require independent licensing and capitalization through the domicile state. A thorough program analysis is the only reliable way to determine which path fits your situation.

What is the admin-obligor warranty structure?

The admin-obligor structure is a warranty reinsurance model where the contractor's company serves as both administrator and obligor, backed by a licensed insurance carrier. The carrier provides the regulatory and solvency foundation, allowing the contractor to capture underwriting profits with a reduced direct licensing burden.

What happens if my warranty reinsurance company falls out of compliance?

Non-compliance can trigger loss of credit for reinsurance accounting, state regulatory fines, program non-renewal, and in serious cases, forced dissolution of the reinsurance entity. Each outcome puts the contractor's warranty program and revenue at risk. Proactive compliance management costs a fraction of what remediation does.

How do I know which warranty reinsurance structure is right for my business?

The right structure depends on your business volume, loss ratios, tax situation, succession goals, and operating states. WarrantyRE conducts a thorough business analysis with every prospective client to match structure to circumstances before any commitments are made.