Introduction

Most contractors selling warranties don't realize they're handing their profit margins to a third party. Every warranty sold represents potential profit that either flows into your business or enriches someone else's. The difference depends entirely on how your program is designed and who controls it.

Choosing or staying in the wrong program affects profitability, claim control, and long-term financial growth. This isn't a one-deal decision. It compounds across every installation or service contract sold — accumulating into hundreds of thousands, sometimes millions, in diverted profits over time.

Here's what to evaluate so you can tell whether your program is actually working for you — or for someone else.

TL;DR

- A well-structured warranty reinsurance program lets contractors own their warranty company and capture underwriting profits instead of funding third parties

- The five most important evaluation factors are fee transparency, reserve methodology, reporting quality, ownership and control, and ongoing administrative support

- Watch for unclear fee breakdowns, vague reserve assumptions, annual-only reporting, and limited contractor input

- The structure, the administrator, and your level of control determine whether you profit or just participate

What Is a Warranty Reinsurance Program for Contractors?

A warranty reinsurance program in the contractor context allows you to establish your own reinsurance entity—typically in an admin obligor structure—that assumes warranty risk and captures profits when claims come in below the premium collected. Instead of paying premiums to a third-party warranty company and losing underwriting profit, you own the structure that collects those premiums.

Here's how the model works for home service contractors:

- Your customer pays for a warranty or service agreement as part of the job

- A portion of that premium flows into your own reinsurance company

- Reserves are set aside for claims

- The remaining profit is yours to keep—not a third party's

This is fundamentally different from traditional third-party arrangements, where the warranty provider retains all underwriting income regardless of actual claim costs.

Why Contractors Are Leaving Money on the Table

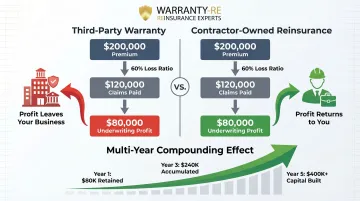

Most HVAC, roofing, plumbing, and electrical contractors use third-party warranty providers without realizing those providers keep the underwriting profit. The US service contract industry generated approximately $49 billion in revenue in 2019, with projections reaching $59 billion by 2028. A significant portion of that revenue flows to third-party administrators rather than the contractors who generate the business.

Every year a contractor stays in a third-party arrangement, underwriting profits accumulate for someone else. For a mid-sized HVAC contractor writing $200,000 in annual warranty fees with a typical 60% loss ratio, that's $80,000 in annual underwriting profit leaving the business every single year.

That gap compounds quickly. Understanding how reinsurance programs work—and what separates a well-structured one from a poor fit—is where evaluation has to start.

Key Factors to Evaluate a Warranty Reinsurance Program

Reinsurance evaluation for contractors isn't just about the headline profit-share percentage. It's about understanding the mechanics behind how and when profits are actually generated, retained, and distributed.

Fee Transparency and Total Cost Structure

Fee transparency is the foundational factor. Every dollar deducted before underwriting profit is calculated—administrative fees, ceding fees, claims adjudication costs, and program overhead—directly reduces what you actually earn.

What clear fee disclosure looks like:

- Single, documented percentage or flat fee covering all services

- No separate line items for claims processing, monthly management, or hold-back fees

- Upfront documentation of any fronting fees charged by the backing insurer

What layered or hidden fee structures look like:

- Multiple deductions at different stages—inflated premium tax adders (1-2%), ceding fees (up to 10%), hold-back fees (1%), monthly management fees (2%), and per-claim fees

- Vague language like "standard administrative costs" without dollar amounts

- Fees disclosed only after you ask directly

Contractors should be able to trace every premium dollar from collection to distribution before signing or staying in any program. If an administrator can't provide a simple flow chart showing exactly where each dollar goes, that's a problem.

Reserve Methodology and Claims Control

Reserves are funds set aside to pay future warranty claims. The assumptions used to calculate them directly affect how much profit is recognized and when it becomes distributable to you.

NAIC Model 685 establishes minimum reserve standards requiring at least 40% of gross consideration received, less claims paid, for service contract providers using the reserve method. But programs can—and do—set reserves higher than this regulatory minimum.

Two failure modes exist:

Overly conservative reserves delay profit recognition for years. If your administrator holds 75% of premium in reserves when actual claims run 50%, you're waiting unnecessarily for your own money.

Overly aggressive reserves create volatility and unpredictable cash flow. If reserves are set at 35% but claims spike to 55%, you'll face capital calls or distribution clawbacks.

Ask these questions:

- Who sets reserve assumptions—the fronting insurer, the administrator, or an independent actuary?

- How often are reserves reviewed and adjusted based on actual claims experience?

- What loss ratio assumptions drive current reserve levels, and do they reflect your actual claim history?

If the administrator can't explain their reserve methodology or deflects with "that's handled by the insurer," you have no reliable way to know when—or whether—your profits will materialize.

Reporting Quality and Financial Visibility

Monthly reporting—not annual summaries—is the minimum standard for a well-run contractor warranty reinsurance program. You should be able to see claims activity, reserve changes, expense deductions, and underwriting results on a regular basis.

Captive insurers must undergo certified annual audits, but that's a compliance floor, not a management ceiling. Effective program oversight requires:

- Monthly financial statements showing premium collected, claims paid, reserves held, and expenses deducted

- Claims detail by product type or coverage line (not just blended totals)

- Reserve movement explanations when adjustments occur

- Year-over-year performance comparisons

Why product-level reporting matters: If you offer both equipment breakdown coverage and labor warranties, one may be profitable while the other drains the program. Blended reporting hides this. You need granular visibility to identify which warranty products are performing well versus which are eroding profitability.

Annual-only reporting is a red flag. It typically means the administrator either lacks the infrastructure to produce regular reporting or prefers you don't look too closely at the numbers.

Program Ownership and Contractor Control

There's a critical difference between "participating in" a reinsurance program and truly owning the reinsurance entity.

Real ownership means:

- You control reserve investment decisions (within regulatory guidelines)

- You set claim handling preferences

- You retain the legal right to distributions when reserves exceed requirements

- You decide whether to continue, modify, or exit the program

Participation arrangements often mean:

- The administrator controls all decisions

- Your "profit share" is calculated by formulas you don't control

- Distribution timing is entirely at the administrator's discretion

- Exiting the program forfeits accumulated reserves

Fronting arrangements typically require 125-150% collateral of projected loss funds, with the contractor's capital at risk. That's appropriate—but only if the contractor actually controls that capital and receives the investment income it generates.

Key questions:

- Who legally controls the money in the program?

- Who makes investment decisions on reserves?

- How rigid or flexible is the program structure as your business grows?

- Can you modify coverage terms, premium structures, or service standards?

Contractors who own their reinsurance entity can adjust coverage terms, retain investment income on reserves, and exit on their own terms. Those who merely participate in someone else's program can do none of those things.

Ongoing Support and Full-Service Administration

The most profitable reinsurance programs are not self-managing. They require active compliance monitoring, claims adjudication, staff training, performance analysis, and legal/tax filings.

These services should be fully included or clearly accounted for:

- Claims administration from first call to final resolution

- Compliance monitoring for IRS Code 831(b) requirements and state regulations

- Staff training on warranty sales and program mechanics

- Monthly financial reporting and performance analysis

- Annual tax return preparation coordination

- Legal entity maintenance and regulatory filings

Robust support versus passive administration:

Programs that provide robust post-setup support actively optimize product mix, analyze claim patterns, adjust premium structures based on performance, and train your team as turnover occurs. Passive programs onboard you, then disappear until you call with a problem.

Before committing to any administrator, ask for a specific list of what they do after your program launches—not just during setup.

Red Flags That Signal a Problem with Your Program

When contractors ask direct questions about program performance, three warning responses frequently surface:

"We don't have that report." If an administrator can't produce monthly financial statements, product-level claim summaries, or reserve movement documentation, their systems are either inadequate or they're deliberately withholding information.

"Trust the administrator." This deflection appears when you ask who sets reserves, how fees are calculated, or why distributions are delayed. Trust is earned through transparency, not demanded in its absence.

"That's just how our program works." Push back when you hear this about fee structures, reserve assumptions, or control limitations. An administrator who can't — or won't — explain the reasoning doesn't inspire confidence in either direction.

The Paper Profit Problem

A program that shows surplus on reports but generates little or no actual distribution to the contractor is usually the result of excessive reserve holds, layered fees, or delayed distribution schedules. This is one of the clearest signals that the program isn't performing as promised.

Example scenario:

- Year 1: $200,000 premium collected, $80,000 claims paid, reports show $40,000 "profit"

- Year 2: $220,000 premium collected, $90,000 claims paid, reports show $50,000 "profit"

- Distribution to contractor after two years: $0

Explanation: Reserves held at 60% of premium, plus 15% in layered fees, means no distributable surplus despite reported "profit." The contractor owns the paper profit but can't access it.

When Switching Programs Makes Sense

Not every problem requires a full exit. The right move depends on where the breakdown is occurring:

- Execution or reporting gaps: A sound structure with weak administration may only need a new administrator, revised fee agreement, or enhanced reporting requirements

- Excessive fees, misaligned ownership, or no transparency: These are structural defects — optimization won't fix them, and switching programs becomes the only real path forward

How WarrantyRE Helps Contractors Build and Evaluate Their Programs

WarrantyRE has spent over 30 years helping business owners establish and manage their own admin obligor reinsurance companies. The company moved from the automotive dealer market into home service contracting—HVAC, roofing, plumbing, and electrical—bringing proven reinsurance infrastructure to a sector that has historically overpaid third-party warranty providers.

All programs are backed by A-rated insurers, ensuring financial stability and regulatory compliance while contractors retain 100% of underwriting profits their customer base generates.

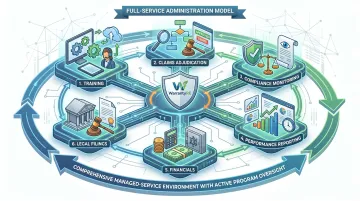

Full-Service Administration Model

WarrantyRE provides comprehensive administration covering the operational complexity contractors want to avoid:

- Training – onboarding and ongoing staff education on warranty sales and program mechanics

- Claims adjudication – full claims management from first call to final resolution

- Compliance – monitoring for IRS Code 831(b) requirements and state regulations

- Performance reporting – monthly financial statements and analysis

- Financials – bookkeeping, accounting records, and annual report preparation

- Legal filings and renewals – all entity maintenance, tax returns, and regulatory submissions

All of this is covered under transparent, flat-fee pricing — no surprise costs as the program grows.

Key Program Benefits

Beyond administration, contractors gain structural advantages that compound over time:

- Fast company setup with minimal burden on the contractor's team

- Onboarding and staff training for a smooth rollout

- Expert business analysis to identify profitability gaps early

- Reserve investment for additional ROI as the program matures

- Tax planning advantages under IRS Code 831(b) for qualifying small insurance companies

- Stronger customer retention through warranty programs contractors control

- Shared-success model: WarrantyRE earns only when contractors are actively writing warranty business

That last point matters when evaluating any reinsurance partner. A provider whose fees depend on your program's activity has a direct reason to help you grow it — not just set it up and step back.

Conclusion

A thorough warranty reinsurance evaluation comes down to one question: is this program structured to serve your financial interests, or the administrator's?

The five evaluation factors—fee transparency, reserve methodology, reporting quality, ownership and control, and ongoing support—provide the framework for assessment. Red flags like vague fee disclosures, annual-only reporting, and deflective answers to direct questions signal structural problems that won't resolve with time.

Those problems are also why evaluation shouldn't stop at onboarding. As claim volumes grow, product mixes shift, and business goals change, contractors should revisit whether their program still fits their business trajectory — not just when something goes wrong, but as a standard part of managing the program.

Frequently Asked Questions

What is a 2-risk warranty in reinsurance?

A 2-risk (or two-risk) warranty in reinsurance refers to an arrangement where the risk of warranty claims is shared between two parties—typically the fronting insurer and the reinsurer. In a contractor warranty context, the fronting insurer issues the policy while the contractor's reinsurance company assumes the actual claim risk.

What are the 4 functions of reinsurance?

According to the Insurance Information Institute, reinsurance serves four core functions:

- Risk transfer — shifts claims liability from the fronting insurer to the reinsurer

- Capacity expansion — allows more contracts to be written

- Financial stabilization — absorbs large or unexpected claims

- Profit participation — enables the contractor or dealer to capture underwriting income

What is an admin obligor model in contractor reinsurance?

In an admin obligor structure, the contractor's own reinsurance company is the administrator and obligor on the warranty contract, backed by an A-rated insurer. This means the contractor retains control, keeps profits, and is not solely dependent on a third-party warranty provider for program performance.

What is the difference between a third-party warranty and a contractor-owned reinsurance program?

With a third-party warranty, the contractor sells coverage but all underwriting profit stays with the provider. A contractor-owned reinsurance program flips that equation—the contractor captures that profit directly while still offering customers full warranty protection, turning warranty from a cost center into a revenue stream.

Can small or mid-sized contractors qualify for a warranty reinsurance program?

Volume thresholds vary by program structure and administrator, so contractors should verify that administrative costs are proportionate to their current warranty volume. Some programs are designed to scale with the contractor from early stages, with no prohibitive minimums.

How long does it take to set up a contractor warranty reinsurance program?

Timelines depend on legal entity formation, state compliance requirements, and the administrator's process. Full-service programs typically complete setup within 4–12 weeks, depending on jurisdiction and how quickly the contractor can provide required documentation.