Introduction

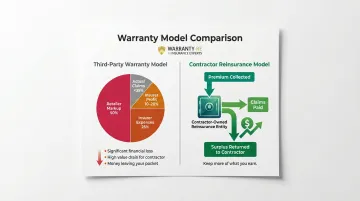

Contractors already offer customer warranties to win jobs and stand behind their work — but when callbacks happen (leaks, system failures, installation issues), those costs come directly out of pocket. Meanwhile, third-party warranty companies collect the premium dollars and keep the underwriting profits, leaving contractors absorbing all the risk with zero upside.

Warranty reinsurance changes this dynamic by enabling contractors to own the company that backs their warranties, capturing profits instead of surrendering them.

This guide covers the best warranty reinsurance companies specifically built for home service contractors, including HVAC, roofing, plumbing, electrical, and general contractors, and what to look for when evaluating them.

TL;DR

- Warranty reinsurance lets contractors own the company that backs their customer warranties, capturing underwriting profits instead of paying third parties

- Top providers handle everything: claims adjudication, compliance, tax filings, and performance reporting—not just initial setup

- Look for admin obligor structure, A-rated insurer backing, no hidden fees, and hands-on onboarding support

- WarrantyRE leads this niche with 30+ years of experience helping contractors nationwide run profitable reinsurance programs

What Is Warranty Reinsurance for Contractors?

The Admin Obligor Model Explained

Warranty reinsurance for contractors operates through an admin obligor structure: the contractor establishes their own reinsurance company that assumes warranty obligations sold to customers, backed by an A-rated fronting insurer. Unlike buying a third-party warranty product, the contractor owns the entity generating the profit.

When customers pay warranty fees (built directly into job pricing), those premiums flow into the contractor's reinsurance company rather than to an outside provider. The funds are held in trust accounts, invested conservatively (typically government bonds), and used to pay claims. Any surplus profit returns to the contractor. Instead of paying a third-party provider, the contractor keeps the surplus.

Financial Benefits and Market Context

The global extended warranty market was valued at $129.65 billion in 2022 and is projected to reach $286.4 billion by 2032 — spanning consumer electronics, automotive, and appliances. For contractors, what matters is where that money actually goes.

In standard third-party warranty models, retailers keep approximately 50% as markup, while insurers retain 25% in expenses plus 10-20% profit, leaving less than 35% allocated to actual claims. Warranty reinsurance redirects that retained margin back to the contractor.

Which Contractors Benefit Most

HVAC, roofing, plumbing, electrical, and general contractors benefit most because they already offer labor warranties competitively and face predictable callback costs. WarrantyRE built this model across 400+ auto dealers before bringing it into the home service space — giving contractors a proven structure for recapturing profits they've long been paying to third-party providers.

Best Warranty Reinsurance Companies for Contractors

Each company below was evaluated on contractor-specific expertise, admin obligor capabilities, service depth, insurer backing, and track record. The list runs from most to least directly relevant for contractors seeking a true contractor-owned reinsurance structure.

WarrantyRE

Founded in 1994 in Southeast Virginia by Tim Byrd, WarrantyRE has over 30 years of reinsurance experience. The company helped 400+ auto dealers build profitable warranty programs before extending its admin obligor model to home service contractors—HVAC, roofing, plumbing, and electrical trades—nationwide.

What sets WarrantyRE apart: Contractors own their admin obligor reinsurance company, backed by A-rated insurers. WarrantyRE handles the full operational load so contractors don't have to:

- Manages all legal filings, tax returns, and compliance

- Handles claims adjudication, bookkeeping, and performance reporting

- Provides staff training and onboarding at no hidden fees

- Operates on a shared-success model — WarrantyRE only profits when contractors do

| Key Feature | Details |

|---|---|

| Admin Obligor Model | Contractor owns the reinsurance company, backed by A-rated insurers |

| Full-Service Administration | Covers training, claims adjudication, compliance, tax filings, bookkeeping, and performance reports |

| Contractor Segments Served | HVAC, roofing, plumbing, electrical, and general contractors nationwide |

Trinity Warranty

Trinity Warranty operates a documented contractor program for HVAC, refrigeration, and plumbing with extended service agreements (ESAs) ranging from 1 to 10 years for residential and commercial equipment. The company provides contractors with labor reimbursement flexibility, allowing them to choose rates of $75, $100, or $125 per hour with annual inflation reviews.

What sets Trinity apart: Trinity offers multi-year coverage terms backed by multiple A-rated insurers and includes large commercial equipment (25+ tons or 2M+ BTUs) in coverage scope. The company provides three-step contractor enrollment and additional services including preventive maintenance programs and indoor air quality solutions.

| Key Feature | Details |

|---|---|

| Program Flexibility | 1-10 year ESA terms; customizable labor reimbursement rates |

| Administration Model | Traditional TPA—Trinity handles administration and insurance backing; contractor does not own reinsurance entity |

| Contractor Segments Served | HVAC, refrigeration, and plumbing (residential and commercial) |

Important distinction: Trinity operates as a third-party administrator (TPA), not a contractor-owned reinsurance structure. Contractors benefit from customer retention and warranty revenue but do not participate in underwriting profits.

NAHG / ServiceGuard

North American HVAC Group (NAHG) offers a contractor-owned warranty company (COWC) model with over 20 years of reinsurance experience. Based in Cumming, Georgia, NAHG enables HVAC contractors and distributors to establish their own warranty entities and participate in back-end profits—the closest match to WarrantyRE's admin obligor concept.

What sets NAHG apart: NAHG's COWC model positions the contractor as the entity that retains underwriting profit and investment income, with DOWC providing administration technology and selling platforms. The company offers compliance portability if the contractor sells the business, annual reimbursement rate reviews for inflation, and formal warranty contracts to customers.

| Key Feature | Details |

|---|---|

| Contractor Ownership | COWC/DOWC model—contractor owns the warranty entity and participates in back-end profits |

| Administration Model | DOWC provides administration technology; compliance managed through partnership framework |

| Contractor Segments Served | HVAC contractors and distributors (no confirmed plumbing, electrical, or roofing programs) |

Trade coverage note: NAHG's documented programs serve only HVAC contractors—no public evidence exists of roofing, plumbing, or electrical coverage.

Fortegra Financial

Fortegra Financial, a subsidiary of Tiptree Inc. (NASDAQ: TIPT), holds an A- (Excellent) AM Best rating and brings 45+ years of warranty industry experience. The company covers home systems including HVAC, plumbing, and electrical through its warranty division and offers profit-sharing options for partners.

What sets Fortegra apart: Fortegra operates as a fronting carrier with dedicated reinsurance capabilities and multiple A-rated insurance entities (Lyndon Southern, Insurance Company of the South, Blue Ridge Indemnity, Fortegra Specialty Insurance, Response Indemnity of California). For contractors whose programs need institutional carrier backing, Fortegra's multi-entity structure can support custom reinsurance arrangements through B2B partnerships.

| Key Feature | Details |

|---|---|

| Financial Strength | A- (Excellent) AM Best FSR; publicly traded parent company (NASDAQ: TIPT) |

| Administration Model | Fronting carrier and reinsurance partner; works through administrators and B2B partnerships |

| Contractor Segments Served | Home systems (HVAC, plumbing, electrical) through partner programs—no confirmed direct contractor reinsurance product |

Important distinction: Fortegra's contractor-specific reinsurance program could not be confirmed from official sources. The company's capabilities suggest it could support contractor programs through custom arrangements, but it does not market an off-the-shelf contractor reinsurance product.

AmTrust Financial Services

AmTrust Financial holds an A (Excellent) AM Best rating and operates warranty programs through its acquired subsidiary Warrantech (purchased 2010). AmTrust's Home Protection division offers warranties covering appliances, electronics, smart home products, and external utility lines.

What sets AmTrust apart: AmTrust provides institutional financial strength with an A (Excellent) rating and extensive warranty infrastructure built over decades. The company's Home Protection products operate through B2B partnerships where partners offer warranties to homeowner customers.

| Key Feature | Details |

|---|---|

| Financial Strength | A (Excellent) AM Best FSR; institutional-scale warranty infrastructure |

| Administration Model | B2B2C model—partners offer warranties to homeowners; AmTrust provides backing and administration |

| Contractor Segments Served | Home Protection division covers appliances and systems—no confirmed contractor-owned reinsurance program |

Important distinction: AmTrust's Warrantech subsidiary focuses on automotive VSCs. No contractor-specific reinsurance program for trades (HVAC, plumbing, electrical, roofing) could be confirmed from official sources. AmTrust serves best as a potential fronting carrier rather than a direct contractor program provider.

How We Chose the Best Warranty Reinsurance Companies for Contractors

Evaluation Framework

Companies were assessed on contractor-specific focus—not just automotive or consumer warranty experience—and the availability of an admin obligor or similarly structured model that allows contractors to own or benefit from the reinsurance entity. We weighted depth of full-service administration: compliance management, claims handling, staff training, and financial reporting.

A common contractor mistake: choosing a provider based on name recognition from automotive or consumer warranty markets without confirming actual contractor program experience. Large carriers like Fortegra and AmTrust have financial strength but may not offer off-the-shelf contractor reinsurance products.

Key Evaluation Criteria

Insurer backing: Programs must be backed by A-rated fronting carriers. An AM Best A- (Excellent) rating signifies excellent ability to meet ongoing insurance obligations—critical for contractor credibility and regulatory compliance across multiple states.

Transparent fee structures: The best providers disclose all costs upfront with no hidden charges. This transparency extends to profit-sharing terms, reserve requirements, and withdrawal conditions.

Onboarding and training quality: Contractors need full staff training on how to sell warranties, handle customer questions, and integrate the program into daily operations. Strong providers offer both online and in-person training with ongoing support.

Compliance track record: Service contract laws exist in approximately 37 states per SCIC, with varying registration, financial security, and disclosure requirements based on the NAIC Service Contracts Model Act. Providers must demonstrate multi-state compliance capability.

Business model alignment: Quality providers should show how programs return profit to contractors as claim reserves accumulate, how premiums are invested for additional ROI, and how the structure supports long-term customer retention.

Scalability and Long-Term Financial Benefit

The best providers show contractors how warranty reinsurance performs over time: premium accumulation, claims payment, reserve growth, and surplus profit distribution. Investment income on reserves — often starting with conservative government bonds, then shifting toward more aggressive positions once reserves exceed 125% of unearned premiums — adds a second profit layer beyond underwriting gains.

Programs should also support customer retention and recurring revenue. When contractors own their warranty structure, one-time installs become the foundation for long-term customer relationships — and a revenue stream that compounds over time.

Conclusion

Choosing the right warranty reinsurance partner means selecting a structure that lets contractors reclaim the profits third-party warranty companies currently pocket. An admin obligor model with full-service administration delivers claims protection, recurring profit, and a genuine customer loyalty tool—built into a single program.

For contractors ready to stop funding third-party warranty companies and start capturing that profit themselves, WarrantyRE offers a full-service admin obligor reinsurance program built specifically for home service contractors. With over 30 years of experience and nationwide support, the program is designed around your trade and customer base. Call WarrantyRE at (804) 824-9533 to find out how it works for your business.

Frequently Asked Questions

What are the best warranty reinsurance companies for contractors?

WarrantyRE leads the contractor-specific reinsurance space with a full admin obligor model for home service contractors. The best providers offer contractor ownership structures, full-service administration, A-rated insurer backing, and proven contractor experience—not generic warranty products.

What is the difference between warranty reinsurance and a third-party warranty provider?

With a third-party provider, underwriting profits leave the business entirely. Warranty reinsurance routes those premium dollars into a contractor-owned entity, letting the contractor capture profits while customers remain protected through A-rated insurer backing.

How does an admin obligor reinsurance program work for contractors?

Customers pay warranty premiums into a reinsurance company the contractor owns. Those funds are held in reserve, invested, and used to pay claims—with surplus profits returning to the contractor. A full-service administrator like WarrantyRE handles all operations, compliance, and claims on the contractor's behalf.

Who are the largest warranty reinsurance companies?

Large institutional reinsurers serve insurance companies, not contractors directly. In the contractor niche, specialized warranty reinsurance program managers like WarrantyRE, NAHG/ServiceGuard, and Trinity Warranty operate with contractor-specific expertise. For contractors, the right question isn't who's largest—it's who has direct experience structuring programs for trades like HVAC, roofing, and plumbing.

Can small or mid-size contractors qualify for a warranty reinsurance program?

Yes—contractor reinsurance programs are not limited to large operations. Providers like WarrantyRE work with contractors of varying sizes to establish right-sized programs, with setup and administration handled by the provider.

What types of contractors benefit most from warranty reinsurance programs?

HVAC, roofing, plumbing, electrical, and general contractors that already sell or plan to sell warranties benefit most. These trades have predictable callback patterns and labor warranties that generate significant recurring revenue and customer loyalty when backed by properly structured reinsurance programs.