Understanding reinsurance terminology is the first step toward evaluating whether a contractor-owned warranty structure makes sense for your business. These aren't terms reserved for insurance professionals. They're the vocabulary you need to ask better questions, evaluate program options, and recognize the financial opportunity sitting inside your existing warranty program.

This guide translates the most important reinsurance and warranty program terms into plain language—specifically for contractors in HVAC, roofing, plumbing, and electrical who want to understand how these programs work before making a strategic decision.

TLDR: Quick Reference for Contractors

- Reinsurance transfers risk from one insurance company to another. Owning your own reinsurer means keeping the underwriting profits a third party would otherwise collect.

- The entity passing risk is the ceding company; the entity accepting it is the reinsurer.

- Treaty reinsurance covers a portfolio automatically; facultative covers individual risks one at a time.

- An administrator obligor structure means you own and control the warranty company, backed by an A-rated insurer.

- Key financial metrics to know: subject premium, ceding commission, underwriting profit, and loss ratio.

Reinsurance Fundamentals: What Every Contractor Should Understand

Reinsurance and Risk Transfer

Reinsurance, as defined by Swiss Re, is essentially insurance for insurance companies — a transaction where one insurer pays a premium to transfer all or part of its risk to another entity. For contractors, the practical translation is straightforward: your warranty company issues warranties, collects premium, and passes catastrophic risk to a backing insurer.

The underwriting profit on claims that never occur — or fall below a defined threshold — stays with you.

Risk transfer is the core concept. When risk moves from your entity to a reinsurer, your exposure is capped. You know what you're on the hook for, and anything above that limit is someone else's problem.

Cede/cession refers to the act of transferring that risk. When you cede exposure to a reinsurer, you're handing off the financial liability — but you keep the customer relationship and a share of the economics. For most contractors, that's the part worth paying attention to.

Retention

Retention is the portion of risk your company keeps before reinsurance kicks in — defined by the Reinsurance Association of America as what the ceding company does not transfer.

Two related terms worth knowing:

- Gross line — your total risk exposure before any reinsurance applies

- Net retained liability — what remains on your books after reinsurance recoveries

Setting the right retention level is one of the key decisions in structuring a contractor-owned program. Too low, and you give away too much of the economics. Too high, and you're absorbing more loss than the program was designed to handle. WarrantyRE works through this calculation during program setup, modeling retention against your claims history and warranty volume to find the right fit.

Underwriting and Underwriting Profit

Underwriting is the process of evaluating, accepting, and pricing risk. In a contractor warranty context, underwriting determines what warranties can be issued, at what price, and under what conditions.

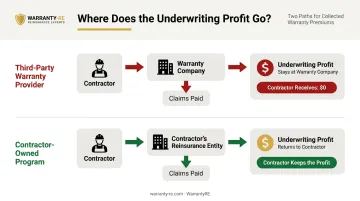

Underwriting profit is what remains from collected premiums after paying claims and expenses. Right now, if you're using a third-party warranty provider, that profit flows to them. The entire logic behind a contractor-owned program is redirecting it back to you.

The Key Players in a Contractor Reinsurance Program

The Ceding Company (Cedent)

The ceding company (also called the cedent) is the entity that originally issues the warranty contract to your customer and then transfers a portion of that risk to a reinsurer. In a contractor warranty program, this is typically the contractor-owned warranty entity.

When you own this entity rather than hand it to a third party, the economics shift in your favor. The cedent collects premiums, controls the customer relationship, and decides which risks to cede — keeping the underwriting profit inside your company instead of sending it elsewhere.

The Reinsurer

The reinsurer is the entity that accepts transferred risk from the ceding company in exchange for a reinsurance premium. In contractor warranty programs, the reinsurer is typically an A-rated insurer that provides financial strength and regulatory standing behind your company.

The reinsurer doesn't interact with your customers. They're a financial backstop. What matters is their creditworthiness — an A-rated backing insurer means the program can pay claims even if your entity faces an unusual loss year.

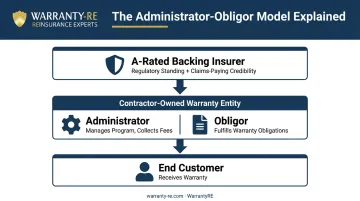

The Administrator Obligor Structure

The administrator obligor structure is the arrangement that most contractor reinsurance programs use. In this structure, you — the contractor — own and operate your own warranty company that serves as both:

- Administrator — managing the program, collecting fees, overseeing operations

- Obligor — responsible for fulfilling the warranty obligations to your customers

This is backed by a licensed, A-rated insurer. That insurer's support is what gives the program regulatory standing and claims-paying credibility.

The financial contrast with a third-party warranty arrangement is straightforward: in a third-party setup, unused premium — the money not spent on claims — stays with the warranty company. In an administrator obligor structure, that money stays in your company. WarrantyRE specializes in helping contractors establish this type of structure, handling everything from company formation to ongoing compliance.

The fronting insurer plays a supporting role in some states. A licensed insurer issues the warranty policy to end customers while your company reinsures most of the risk back to itself. This arrangement — called fronting — allows the program to meet state regulatory requirements while the economics flow through the entity you own. As IRMI defines it, a fronting arrangement involves a licensed, admitted insurer issuing a policy on behalf of a self-insured organization or captive without bearing the underlying risk.

Types of Reinsurance Contracts You Will Encounter

Treaty vs. Facultative Reinsurance

Treaty reinsurance is a standing agreement that automatically covers a defined class or portfolio of risks. Once the program parameters are set, warranties issued within those parameters are covered—no individual approval required per transaction. Most contractor warranty programs operate on a treaty basis.

Facultative reinsurance is negotiated individually for specific risks. The reinsurer reviews each submission and can accept or decline. This approach is less common in contractor warranty programs but may apply for unusual or high-value situations.

For most HVAC, roofing, plumbing, and electrical contractors, treaty reinsurance is the relevant structure. The program is set up once, and it runs automatically within the defined terms.

Proportional Reinsurance: Quota Share

Quota share reinsurance (also called pro rata or proportional reinsurance) is the structure where the reinsurer accepts a fixed percentage of every risk ceded and receives that same percentage of the premium—sharing losses in the same proportion.

In a contractor warranty program, this means:

- Premiums collected are split proportionally between your entity and the backing reinsurer

- Claims are shared in the same proportion

- The arrangement is predictable, which is why quota share structures are commonly used in contractor warranty reinsurance

The predictability matters. Contractors can model their expected economics without relying on complex actuarial projections.

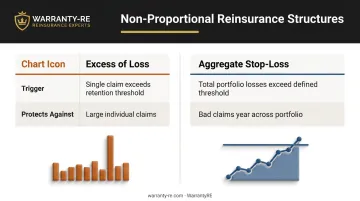

Non-Proportional Reinsurance: Excess of Loss and Stop-Loss

Unlike quota share, excess of loss reinsurance only pays when a loss exceeds a specified retention amount. Your entity absorbs losses up to that retention; the reinsurer covers amounts above it up to a defined limit. This protects against large or unexpected individual claims.

Aggregate stop-loss (also called excess of loss ratio reinsurance) operates at the portfolio level. It triggers when your total losses over a defined period exceed a specified dollar amount or loss ratio threshold—acting as a backstop for an unusually bad claims year, not just a single large claim.

Here's how the two non-proportional structures compare:

| Structure | What Triggers It | What It Protects Against |

|---|---|---|

| Excess of Loss | Single claim exceeds retention | Large individual claims |

| Aggregate Stop-Loss | Total losses exceed threshold | Bad claims year across the portfolio |

Smaller operations often start with excess of loss coverage. Contractors with larger warranty portfolios may layer in aggregate stop-loss as an additional safeguard against portfolio-wide volatility.

Key Financial and Premium Terms

These terms appear in every program financial report. Understanding them lets you evaluate whether your program is performing.

Subject premium (also called base premium or underlying premium) is your collected premiums that serve as the basis for calculating the reinsurance premium. It's the starting number from which commissions, reinsurer share, and profit analysis all flow.

Ceding commission is an allowance paid by the reinsurer back to your entity to help offset acquisition costs, overhead, and administrative expenses. This is one of the revenue streams that makes owning your program more profitable than paying fees to a third-party administrator — and captures those economics for the contractor rather than the administrator.

Loss ratio is claims incurred expressed as a percentage of earned premiums. The NAIC defines it simply as incurred losses as a percentage of earned premiums.

Tracking this number matters because:

- A lower loss ratio means more underwriting profit stays in your company

- A consistently high loss ratio signals a claims management problem, a pricing issue, or both

- Monthly financial statements from your program administrator let you catch either trend early

Claims, Loss, and Risk Terms

Loss Reserves and IBNR

A loss reserve is an estimate set aside to cover claims that have occurred but haven't been fully paid yet. Proper reserve management is a compliance requirement for any entity that owns a reinsurance program.

Incurred But Not Reported (IBNR) is an actuarial estimate of losses that have already occurred but haven't been reported yet. It explains why your program financials may show reserves even when no claims have been filed — a normal part of how reinsurance programs are structured and monitored.

Loss Adjustment Expense

Loss adjustment expense (LAE) covers the costs of investigating and settling claims—adjuster fees, legal costs, and related overhead. Two subcategories:

- Allocated LAE (ALAE) — expenses tied to a specific claim

- Unallocated LAE (ULAE) — general claims-handling overhead not assigned to individual claims

In contractor warranty programs administered by WarrantyRE, claims adjudication is built into the full-service package. WarrantyRE handles every claim from first notice to final resolution, so contractors aren't separately managing these costs — they're embedded in the program structure.

Frequently Asked Questions

What are the key reinsurance terms contractors should know?

The foundation is: reinsurance, ceding company, retention, treaty, quota share, excess of loss, underwriting profit, loss ratio, and administrator obligor. These terms let contractors evaluate any warranty reinsurance program independently—without relying on a third party to explain the economics.

What is the difference between treaty and facultative reinsurance?

Treaty reinsurance automatically covers an entire portfolio of defined risks under a standing agreement. Facultative reinsurance is negotiated individually, with the reinsurer accepting or declining each submission. Most contractor warranty programs use treaty arrangements, set up once and then running automatically within defined parameters.

What is the difference between a ceding company and a reinsurer?

The ceding company issues warranties to customers and transfers a portion of risk to the reinsurer. The reinsurer accepts that transferred risk and provides financial backing. In a contractor-owned program, your entity serves as the ceding company, which is what keeps underwriting profits in your hands instead of a third party's.

What does "administrator obligor" mean for a contractor?

It means you own and control your warranty company—serving as both administrator and obligor—backed by a licensed, A-rated insurer. The practical result is that underwriting profits stay in your company instead of flowing to a third-party warranty provider.

What is underwriting profit and why does it matter?

Underwriting profit is what remains from collected premiums after paying claims and expenses. Third-party warranty providers keep this profit under traditional arrangements. In a contractor-owned reinsurance structure, that profit stays in your reinsurance entity rather than flowing to a third party.

What is a loss ratio and how should contractors track it?

Loss ratio is claims paid divided by premiums earned, expressed as a percentage. A lower ratio means more profit retained in your entity. WarrantyRE provides monthly statements and performance reports so contractors can track this number month over month.