A contractor reinsurance program changes that equation entirely. Instead of paying out, contractors own the entity that receives premiums, holds reserves, pays claims, and retains what's left over.

This article covers what contractors need to evaluate before setting one up: how the financial structure works, what the administrator-obligor model actually means, compliance obligations, operational requirements, and how to choose the right program partner.

TL;DR

- Contractor reinsurance programs capture warranty underwriting profits that would otherwise go to third-party providers

- The administrator-obligor structure makes the contractor the risk-bearing entity, backed by an A-rated carrier

- A program administrator handles compliance, claims adjudication, tax filings, and financial reporting on the contractor's behalf

- Program viability depends on having sufficient annual warranty volume to build meaningful reserves

- Partner selection drives program success: experience, compliance rigor, and full-service administration are the deciding factors

What Is a Contractor Reinsurance Program?

In plain terms: the contractor forms their own reinsurance company. That entity accepts warranty premiums collected from customers, holds reserves, pays claims when they arise, and keeps the surplus — the underwriting profit — that would otherwise flow to a third-party warranty company.

This is structurally different from simply selling a warranty. When a contractor sells a third-party warranty product, they act as a distribution channel for someone else's financial arrangement. The premium leaves, the profit leaves — and the contractor has no input on claims handling or coverage terms.

With a reinsurance structure, the contractor becomes the risk-bearing entity. An A-rated insurance carrier provides the backstop: if claims exceed reserves unexpectedly, the carrier absorbs the excess. That coverage is what keeps the model financially disciplined, not speculative.

Which contractors does this model suit?

- HVAC contractors reinsuring labor warranties on furnace, AC, heat pump, and mini-split installations

- Roofing and exterior contractors covering workmanship warranties with warranty fees built into every job

- Plumbing contractors whose service work — water heater replacements, repiping, fixture installs — generates natural warranty exposure

- Electrical contractors covering panel installations, wiring, and fixture connections

- General contractors with recurring, high-ticket installation or service work

The common thread is recurring, high-ticket work with a natural warranty component. Consistent premium flow is what allows a reinsurance entity to build meaningful reserves over time.

Key Financial Considerations Before Setting Up Your Program

Underwriting Profit and Cash Flow

Underwriting profit is the surplus remaining after claims are paid from premium reserves. In a third-party arrangement, that surplus belongs to the warranty company. In a contractor-owned reinsurance structure, it stays inside the contractor's entity.

The actual margin depends on claims frequency, claims severity, premium pricing accuracy, reserve adequacy, and administrative costs. No reliable public benchmark exists for contractor-specific warranty programs — any provider quoting a guaranteed percentage without an actuarial feasibility study is not a credible source. What matters is that the program is priced correctly and administered consistently.

One cash flow mechanism worth understanding is the Net-Net remittance approach: warranty repairs performed by the contractor are deducted directly from premiums due before remittance. The repair cost offsets what's owed — no separate claim check required — keeping cash flow positive and reducing out-of-pocket costs.

Investment Income on Reserves

Premium reserves held within the reinsurance entity don't sit idle. Those funds can be invested — typically in conservative government instruments — generating returns on top of underwriting profits.

This is a second income stream that most contractors never access under a third-party arrangement. Under WarrantyRE's program, investment income earned on reserve funds belongs to the contractor's reinsurance company. As the reserve balance grows beyond required levels, excess funds may be invested more aggressively at the direction of the ownership.

Tax Planning and Startup Considerations

Contractor-owned reinsurance structures can offer meaningful tax planning advantages, including potential for tax-deferred wealth accumulation — a frequently cited benefit among accounting advisors in the dealer and contractor reinsurance space.

That said, small captive and 831(b) structures carry specific IRS scrutiny. The Federal Register's January 2025 final regulations classify certain micro-captive arrangements as listed transactions requiring disclosure. Consult a qualified tax professional before treating tax benefits as a primary driver.

On the practical side, program viability depends on scale. Before moving forward, contractors should weigh:

- Utah's Insurance Department guidance suggests pure captives generally need at least $750,000 in annual premium to be operationally viable

- Programs undersized relative to their administrative cost structure may not generate enough reserve to be financially meaningful

- WarrantyRE evaluates each contractor's volume, claims history, and business profile individually — there's no rigid universal threshold, but sufficient warranty volume is a prerequisite

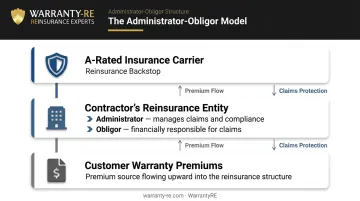

Structural Considerations: Understanding the Administrator-Obligor Model

How the Structure Works

The administrator-obligor model has a specific legal meaning. The contractor's reinsurance entity acts as:

- The administrator — managing the program, handling claims adjudication, and maintaining regulatory compliance

- The obligor — the entity financially responsible for honoring warranty claims

An A-rated insurance carrier sits behind the structure as the reinsurance backstop. If the contractor's reserves are insufficient to cover a spike in claims, the carrier's obligation activates. This limits the contractor's financial exposure to their formation costs plus accumulated earnings , not open-ended liability.

Contrast that with the traditional third-party model, where the contractor has no control over claims decisions, coverage terms, or profit retention. The third-party company decides whether to pay, how much to pay, and keeps whatever premiums they didn't spend on claims.

The Sensible Home Warranty liquidation in 2015 illustrates the downside of third-party dependency: the company went into receivership, Florida's guaranty association provided no coverage, and Class 2 loss claimants ultimately received a pro-rata distribution of just 15.3 cents on the dollar. Contractors relying on that administrator had no claim to the reserves , because the reserves weren't theirs.

Risk Management and Carrier Backing

Under the administrator-obligor model, premium reserves are held within the contractor's own entity. The contractor always has access to their reserve funds , which eliminates exposure to a third-party provider's solvency risk.

The A-rated carrier's role is what converts the arrangement from self-insurance (which most contractors aren't licensed to operate) into a compliant reinsurance structure. That compliance layer also opens the door to meaningful customization. Contractors can tailor:

- What work is covered under the warranty

- How claims are submitted and adjudicated

- How disputes are handled and resolved

Each of those decisions directly affects profitability and customer satisfaction.

Compliance and Legal Considerations for Contractors

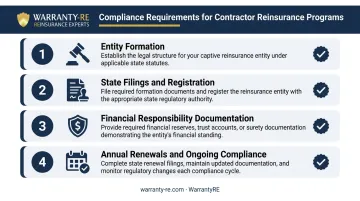

Forming a reinsurance company isn't a paperwork-free process. Requirements include:

- Entity formation under the chosen domicile's insurance law

- State filings for service contract provider or administrator registration (requirements vary significantly — New York, Washington, Oklahoma, and Texas each have distinct rules)

- Financial responsibility documentation — typically a reimbursement insurance policy or funded reserve meeting state minimums

- Annual renewals and ongoing regulatory compliance

The NAIC Service Contracts Model Act provides the foundational framework, but state-level interpretation varies. An experienced program administrator is essential here — state-level variation in interpretation makes independent navigation genuinely risky.

Compliant warranty contract language, claims procedures, and financial reporting are also legally required. Errors in these areas create regulatory liability, not just paperwork delays. An experienced program administrator handles these filings on the contractor's behalf and ensures the program operates within applicable law.

Tax compliance adds another layer. The reinsurance entity files separately from the contractor's main business financials — as a property and casualty insurance company using Form 1120PC, which requires specialized insurance tax expertise. WarrantyRE manages all legal forms, filings, tax returns, and renewals, including coordination with insurance tax experts who prepare the annual returns.

Operational Considerations: What Running the Program Actually Involves

The day-to-day operational picture for a well-structured program looks like this:

| Task | Who Handles It |

|---|---|

| Tracking warranty sales | Program administrator |

| Collecting and remitting premiums | Contractor + administrator |

| Claims adjudication | Program administrator |

| Monthly financial statements | Program administrator |

| Annual tax returns | Insurance tax expert via administrator |

| State filings and renewals | Program administrator |

In a properly structured program, the contractor's internal team is not running the reinsurance company. The program administrator carries that operational weight.

Staff training is one of the most overlooked pieces of the setup. Technicians, project managers, and office staff who present warranties to customers need to understand what they're selling well enough to explain it confidently. Weak presentations at the point of sale reduce attachment rates — and lower attachment means less premium volume and slower reserve accumulation.

WarrantyRE provides both online and in-person training so contractor teams can present programs accurately and answer customer questions without hesitation.

Performance reporting is the other operational pillar. Contractors should receive regular reports showing:

- Reserve balances

- Claims ratios

- Underwriting profit accumulation

- Investment returns

These reports are how a contractor evaluates program health and determines whether coverage adjustments are warranted. If a program administrator can't provide this visibility, that's a problem.

How to Evaluate a Contractor Reinsurance Program Partner

Choosing the right program administrator is where most contractor reinsurance decisions succeed or fail. The administrator structures the deal, keeps the program compliant, manages claims, handles the finances, and ensures the contractor doesn't inadvertently create regulatory exposure.

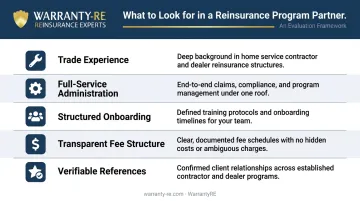

Criteria that separate experienced administrators from the rest:

- Documented history with HVAC, roofing, plumbing, and electrical programs — not just general captive management

- Full-service administration covering entity formation, claims adjudication, compliance filings, bookkeeping, and tax returns

- Structured onboarding that prepares contractor staff to sell and explain the warranty product confidently

- Fee structures with no hidden costs, aligning administrator incentives with contractor success

- Verifiable references across multiple trades, with evidence of handling compliance changes, claims disputes, and program edge cases

An administrator who has only been in the space a few years hasn't encountered the scenarios that matter most: a state regulatory change mid-program, an unusual claims spike, a coverage dispute that tests contract language. Ask any candidate how they've handled those situations — and verify the answers.

WarrantyRE has been guiding contractors through this process since 1994. Administration covers entity formation, claims adjudication, compliance filings, staff training, financial reporting, and tax returns. The underlying philosophy is straightforward: contractor profitability is the measure of success, and the program is built to reflect that.

Frequently Asked Questions

What are the benefits of a contractor reinsurance program?

A reinsurance program shifts warranty economics in the contractor's favor. Instead of paying surplus to a third-party provider, contractors capture underwriting profits, control claims decisions, earn investment income on reserves, and build a recurring revenue stream funded by their own customer base.

How does a contractor reinsurance program differ from a standard warranty?

A standard warranty routes premiums to a third-party company that retains the surplus after claims. A contractor reinsurance program routes those same premiums into a contractor-owned entity — the surplus after claims stays inside the contractor's reinsurance company.

What types of contractors can set up a reinsurance program?

HVAC, roofing, plumbing, electrical, and general contractors can all establish contractor reinsurance programs. The primary requirement is enough annual warranty volume to build adequate reserves and cover the program's administrative cost structure.

What is an administrator-obligor structure in reinsurance?

In an administrator-obligor structure, the contractor's reinsurance entity serves two roles: program administrator (managing claims and compliance) and obligor (financially responsible for claims). An A-rated carrier provides a reinsurance backstop that caps exposure if claims spike unexpectedly.

How long does it take to see profits from a contractor reinsurance program?

Profit timelines depend on premium volume and claims experience. Underwriting profits typically begin accumulating in the first year as reserves build, with returns growing more substantial as premium volume increases and claims patterns stabilize.

Does a contractor need to manage the reinsurance company themselves?

No. A full-service program administrator handles entity formation, compliance, claims adjudication, financial reporting, and tax returns. Contractors don't need specialized insurance or legal expertise — the administrator manages all of it.