When you pay a third-party warranty provider, that company earns underwriting profits from your customers' premiums. The IRS has a specific set of rules that can either keep those profits in your pocket or leave them with someone else — depending entirely on how your reinsurance entity is classified and administered. Get the structure right and you defer significant taxes. Get it wrong and you face back taxes, penalties, or disqualification from favorable treatment entirely.

This article covers how the IRS classifies warranty reinsurance entities, the four methods for taxing premium income, the IRC Section 831(b) election, PATH Act compliance tests, and what a properly administered program looks like in practice.

TLDR: Key Takeaways

- The IRS uses a federal insurance test (risk-shifting and risk-distribution) to determine how your warranty reinsurance entity is taxed — regardless of state law classification

- IRC 831/832 insurance company accounting typically produces the best after-tax result across the four available income recognition methods

- An IRC Section 831(b) election lets qualifying small insurers defer tax on underwriting profits, paying tax on investment income only

- For 2026, Rev. Proc. 2025-32 sets the 831(b) premium threshold at $2,900,000

- The PATH Act's two diversification tests can disqualify a reinsurance company from 831(b) treatment if failed

- IRS Notice 2016-66 carries penalties up to $50,000 per entity per year for non-disclosure

How the IRS Classifies Warranty Reinsurance Entities

The Federal Insurance Standard

Warranty contracts are not classified as insurance products under most state laws. The IRS operates on a separate standard entirely. For federal tax purposes, classification depends on case law — specifically the risk-shifting and risk-distribution requirements established in Helvering v. LeGierse, 312 U.S. 531 (1941).

A warranty entity that satisfies the federal insurance test gains access to favorable accounting methods, deduction timing, and the Section 831(b) election. One that doesn't is taxed as an ordinary service company or corporation — without loss reserve deductions or any of the insurance-specific tax treatment.

The IRS has ruled favorably for warranty structures that clear the bar:

- PLR 201419007 (2014) — certain extended warranties constituted insurance contracts for federal tax purposes

- PLR 201732021 (2017) — vehicle service contracts qualified as insurance where they involved genuine risk-shifting and distribution across multiple end consumers

One important caveat: private letter rulings apply only to the taxpayer who requested them and are not binding precedent. The IRS has also ruled against warranty structures (see TAM 200827006), so the facts of each arrangement matter.

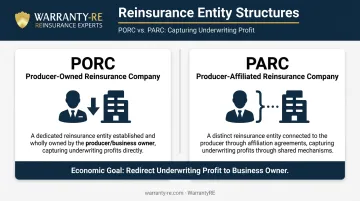

Entity Structures: PORCs and PARCs

How an entity is classified also determines which structure makes sense. Two primary reinsurance structures place the business owner in the role of reinsurer:

- Producer-Owned Reinsurance Companies (PORCs) — the business owner directly owns the reinsurance entity, capturing underwriting profit on warranties sold through their operations

- Producer-Affiliated Reinsurance Companies (PARCs) — ownership is through an affiliated but separately structured entity

In both structures, the economic goal is identical: redirect underwriting profit away from third-party insurers and back to the business owner's balance sheet.

Foreign Domicile and the 953(d) Election

Many warranty reinsurance companies are formed in foreign domiciles — not for tax advantages, but to avoid the capital requirements and regulatory burdens of U.S. state insurance law. Turks and Caicos is one example of a common offshore domicile.

There is no inherent tax benefit to going offshore. What matters is that IRC Section 953(d) allows a foreign-domiciled insurance company to elect to be treated as a domestic U.S. taxpayer for federal tax purposes. That election is made when the company files its first federal income tax return — and missing that window is an expensive mistake.

WarrantyRE coordinates the 953(d) election as part of its standard program setup, ensuring the election is filed correctly and on time alongside the company's first Form 1120-PC. All client funds remain in U.S. trust accounts regardless of the offshore domicile.

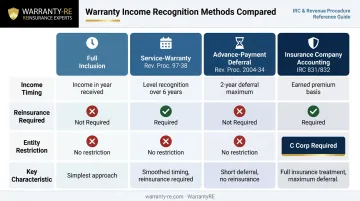

The Four Methods for Taxing Warranty Premium Income

Warranty entities have four recognized methods for reporting premium income to the IRS. Which one applies — or which one you choose — determines when tax hits, how much deferral you get, and what entity structure you need.

Method 1: Full Inclusion

All premium income is recognized in the year received. Reinsurance expense is amortized over the contract term. Simple to administer, but it front-loads taxable income on multi-year contracts, which is why most warranty operators avoid it.

Method 2: Service-Warranty Income Method (Rev. Proc. 97-38)

Available to manufacturers, wholesalers, and retailers of motor vehicles or durable consumer goods selling multi-year service-warranty contracts. Key requirements:

- The taxpayer must purchase reinsurance from an unrelated third party within 60 days of premium receipt

- Income is recognized on a level basis over the shorter of the contract term or six years

- Available to S corporations, LLCs, and partnerships — no mandatory C corp requirement

- An imputed income component can exceed the actual premium received, which can push taxable income above actual cash received

Method 3: Advance-Payment Deferral (Rev. Proc. 2004-34)

Accrual-basis taxpayers can defer income attributable to services performed in the next succeeding tax year — creating a two-year deferral window. No reinsurance purchase required, though the deferral is shallower than what the service-warranty method produces.

Method 4: Insurance Company Accounting (IRC Sections 831 and 832)

When a warranty entity qualifies as an insurance company:

- Premium income is recognized based on earned premium calculations under IRC Section 832 (gross premiums written, adjusted by 80% of beginning and ending unearned premium reserves)

- Acquisition costs are fully deductible in the current period

- Income spreads naturally over the policy life

This method historically produces the highest net present value of after-tax cash flows among the four options. The trade-off is mandatory C corporation status, which exposes distributions to a second level of tax.

That double-taxation cost needs to be weighed against the NPV advantage from earned premium deferral. In most cases, pairing Method 4 with a Section 831(b) election closes the gap — but the math should be run before committing to the structure.

Quick Comparison:

| Method | Income Timing | Reinsurance Required | Entity Restriction |

|---|---|---|---|

| Full Inclusion | Year received | No | None |

| Service-Warranty (Rev. Proc. 97-38) | Level over contract term (max 6 yrs) | Yes — unrelated third party within 60 days | None (S corp, LLC, partnership eligible) |

| Advance-Payment Deferral (Rev. Proc. 2004-34) | Up to 2-year deferral | No | Accrual-basis taxpayers only |

| Insurance Company Accounting (IRC 831/832) | Earned premium basis over policy life | No | C corporation required |

IRC Section 831(b): The Small Insurance Company Election

What the Election Does

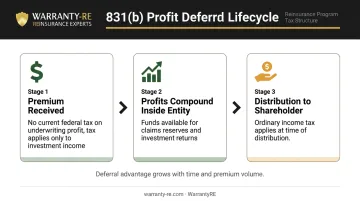

An IRC Section 831(b) election allows a qualifying small property and casualty insurance company to exclude net premium income — underwriting profits — from federal income taxation at the entity level. The company pays tax only on taxable investment income.

To be clear: underwriting profits are not permanently exempt. They become taxable when distributed to shareholders. The advantage is deferral — profits compound inside the reinsurance entity, available to pay claims or generate investment returns, before any distribution-level tax applies.

Premium Threshold

The 831(b) election is only available to companies below the annual premium ceiling. Per Rev. Proc. 2025-32, the inflation-adjusted limit for taxable years beginning in 2026 is $2,900,000. The statutory base of $2,200,000 (set by the PATH Act) is adjusted annually for inflation and rounded down to the next $50,000 increment.

For most HVAC contractors, roofing companies, and dealerships operating warranty reinsurance programs, this threshold accommodates their annual premium volume.

How the Election Is Filed

The 831(b) election is made by checking the appropriate box on Form 1120-PC when filing the company's initial income tax return. Key procedural points:

- Foreign-domiciled entities must file the 953(d) election first to be treated as U.S. taxpayers before 831(b) treatment applies

- Once made, the election can only be revoked with the consent of the IRS Secretary

- Missing the initial filing window is a costly administrative error — there is no simple catch-up mechanism

WarrantyRE handles both the 953(d) and 831(b) elections as part of standard program administration. An insurance tax specialist prepares all returns, with filings coordinated alongside entity formation so the election is captured on the first return — as required. Getting this right from the start is what makes the deferral benefit available from day one.

The Dual-Tax Reality

The "no tax on underwriting profits" framing is accurate but incomplete. The full picture looks like this:

- Inside the entity: No current federal income tax on underwriting profits — only tax on investment income

- Upon distribution: Profits are taxed as ordinary income to the shareholder

The long-term advantage comes from compounding. Funds inside a properly structured 831(b) reinsurance company are available to pay claims, invest, and grow before the distribution tax is ever triggered.

For a contractor running $500,000 or more in annual warranty premiums, even a few years of tax-deferred compounding inside the entity can meaningfully outpace the economics of paying a third-party provider and receiving nothing back.

Compliance Risks: PATH Act Diversification Tests and IRS Notice 2016-66

Diversification Tests Under the PATH Act

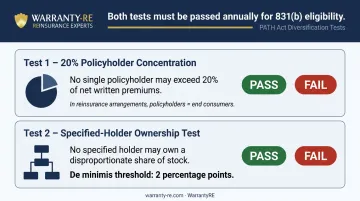

The Protecting Americans from Tax Hikes (PATH) Act introduced two diversification tests that determine whether an entity qualifies for 831(b) treatment. Failing both tests disqualifies the company for that tax year.

Test 1: 20% Policyholder Concentration Test (IRC §831(b)(2)(B)(i)(I)) No single policyholder can account for more than 20% of net written premiums (or direct written premiums, whichever is greater). Related policyholders are treated as one.

For warranty reinsurance, IRC Section 831(b)(2)(D) provides that in reinsurance or fronting arrangements, the term "policyholder" means each policyholder of the underlying direct written insurance — meaning end consumers, not the dealership or contractor. This is favorable for operators writing warranties across a broad customer base.

Test 2: Specified-Holder Ownership Test (IRC §831(b)(2)(B)(i)(II)) No person with an interest in the insurance company can hold a more than de minimis ownership stake that exceeds their proportional interest in the insured business. The IRS defines de minimis as 2 percentage points or less.

Entities that are identically or nearly identically owned (the insured business and reinsurance company owned by the same person at the same percentage) satisfy this safe harbor.

The PATH Act's diversification requirements were designed to prevent reinsurance entities from functioning primarily as wealth transfer or estate-planning vehicles rather than genuine risk distribution mechanisms. Warranty and GAP reinsurance programs that write risk across a large population of end consumers generally align with the legislative intent — but annual verification matters.

Passing those tests annually is only part of the compliance picture. Separate disclosure obligations under IRS Notice 2016-66 carry their own penalty exposure — and recent regulatory changes have raised the stakes.

IRS Notice 2016-66 and Disclosure Requirements

IRS Notice 2016-66 designated certain Section 831(b) micro-captive and reinsurance arrangements as "transactions of interest," triggering Form 8886 disclosure obligations. The penalty for non-disclosure under IRC Section 6707A:

- $50,000 per entity per year for non-natural persons

- $10,000 per year for natural persons

Multiple parties connected to a single arrangement — the reinsurance company, the operating business, shareholders, and potentially material advisors — each face separate disclosure obligations. A single non-compliant program can generate hundreds of thousands of dollars in aggregate penalties.

A practical nuance: Notice 2016-66 targeted arrangements with characteristics of tax shelters (low loss ratios, unusual risk types, estate-planning features) rather than warranty and mechanical breakdown reinsurance programs with genuine risk. The notice language is broad enough, however, that many tax advisors have recommended precautionary disclosure as a conservative measure while further guidance develops. In January 2025, the IRS published final regulations (T.D. 10029) identifying certain micro-captive transactions as listed transactions — a designation that increases penalty exposure and makes proactive compliance monitoring essential.

WarrantyRE's internal position, based on its client materials, is that properly organized and administered reinsurance programs have historically come through IRS review compliant. The company coordinates with CPAs and legal counsel to ensure all required filings are handled appropriately.

How to Structure Your Warranty Reinsurance Program for Tax Compliance

Proper tax treatment begins at formation. Errors made during setup — wrong entity type, missed election windows, inadequate records — are expensive to unwind and can cost years of favorable tax treatment.

Formation Decisions That Set the Course

- Entity type: C corporation status is required for 831(b) treatment under the insurance company accounting method

- Domicile selection: Foreign domicile (for regulatory flexibility) requires a timely 953(d) election

- Election timing: Both the 953(d) and 831(b) elections must be made on the company's first tax return — there is no second chance

- Record-keeping: Each policy sold must be documented accurately to support premium calculations and diversification test compliance

Ongoing Compliance Requirements

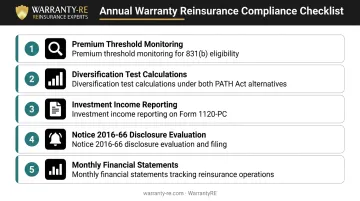

Annual administration isn't optional — it's where most compliance failures occur. A properly run warranty reinsurance program requires:

- Premium threshold monitoring to confirm 831(b) eligibility each year

- Diversification test calculations under both PATH Act alternatives

- Investment income reporting on Form 1120-PC

- Notice 2016-66 disclosure evaluation and filing where warranted

- Monthly financial statements tracking all reinsurance operations activity

The IRS LB&I division maintains an active micro-captive insurance examination campaign, and the agency has mailed settlement offers to taxpayers under audit for micro-captive arrangements. Operators running compliant, well-documented programs are in a fundamentally different position than those running poorly structured shelters — but documentation is what makes that difference demonstrable.

Working With a Program Administrator

That audit exposure is precisely why administration matters. Managing these requirements while running a contracting business or dealership is impractical for most owners, and the compliance failures that attract IRS scrutiny typically stem from administrative gaps — missed elections, undocumented policies, inadequate diversification records — not intentional abuse.

WarrantyRE handles program administration from entity formation through annual compliance reporting — covering legal filings, 953(d) and 831(b) elections, claims adjudication, and tax return preparation by insurance tax specialists. WarrantyRE's admin obligor structure means clients' reinsurance companies are backed by A-rated carriers, so if claim reserves prove inadequate, the direct writing insurance company carries the ultimate obligation, not the client. Clients own their reinsurance company and keep the underwriting profits; WarrantyRE keeps the program running cleanly.

Frequently Asked Questions

Is reinsurance an asset or liability?

From the reinsurance company's balance sheet, it's both: premiums received are a liability (unearned premium reserves) until earned, while investment holdings and recoverables are assets. For the business owner, the equity accumulated inside the reinsurance entity — underwriting profits net of claims — is a growing asset.

Are warranty expenses tax deductible?

Warranty-related expenses — including claims paid and reinsurance premiums paid to an unrelated third-party insurer — are generally deductible business expenses. Timing and deductibility method depend on the company's accounting method (cash vs. accrual) and whether it qualifies as an insurance company for federal tax purposes.

Are extended warranties included in tax basis?

For the warranty seller, revenue from service contracts is not added to the tax basis of any underlying property — it's recognized as income under the seller's accounting method and entity classification. How quickly that income is recognized depends on whether the seller qualifies as an insurance company for tax purposes and which revenue recognition rules apply.

What is IRC Section 831(b) and how does it apply to warranty reinsurance?

IRC Section 831(b) allows qualifying small property and casualty insurance companies to exclude net premium income from federal taxation, paying tax only on investment income. Warranty reinsurance companies that meet the eligibility requirements — including the annual premium threshold and PATH Act diversification tests — can elect this treatment to defer tax on underwriting profits.

What disclosure requirements apply under IRS Notice 2016-66?

Notice 2016-66 requires participants in certain 831(b) micro-captive arrangements designated as "transactions of interest" to file Form 8886 disclosures. Failure to comply carries a $50,000 penalty per entity per year for non-natural persons. Many warranty reinsurance operators have filed disclosures as a precaution, even where their specific risk types (mechanical breakdown, GAP) may not squarely fall within the notice's primary targets.

How are underwriting profits from warranty reinsurance taxed?

For 831(b)-electing companies, underwriting profits accumulate inside the reinsurance entity without current federal income tax, then are taxed when distributed to the owner. This deferral allows profits to compound inside the entity — funding claims reserves and generating investment returns — before any distribution-level tax applies.