Introduction

Roofing contractors focus hard on crew efficiency, installation quality, and project volume. But one decision shapes long-term profitability just as much: how you structure your warranty program.

Choose the wrong structure, and your labor guarantees become a cost center — absorbing claims costs with no return. Choose the right one, and every job you close generates recurring income, supports higher pricing, and builds the referral engine that grows your business.

Most roofing contractors already offer workmanship warranties to win jobs and stand behind their work. The strategic question isn't whether to offer warranties—it's who profits from them.

TL;DR

- Your warranty program structure directly affects profit margins, claims exposure, and customer loyalty

- Four main models exist: basic contractor workmanship, manufacturer-backed extended warranties, third-party programs, and self-funded reinsurance

- Third-party programs shift claims risk off your plate — but hand underwriting profits to someone else

- Self-funded reinsurance keeps those profits inside your own tax-advantaged company instead

- Evaluate programs on profitability potential, claims control, administrative burden, customer experience, and scalability

What Is a Warranty Program for a Roofing Business?

A roofing warranty program is the formal structure through which your business commits to standing behind its work—covering defects in materials, installation errors, or both—and determines who bears the financial risk when a claim arises. It's not just a document you hand customers; it's a business system that defines how claims are funded, who administers them, how the program is priced into jobs, and whether you retain profits or pay a third party.

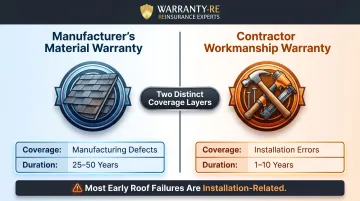

Every roofing contractor must address two underlying warranty layers:

- Manufacturer's material warranty – issued by shingle brands (GAF, Owens Corning, CertainTeed), covering product defects

- Workmanship warranty – issued by the contractor, covering installation errors

Most roof failures in the first decade are installation-related, making workmanship coverage the more financially consequential layer for your business to manage. According to the National Roof Certification and Inspection Association (NRCIA), "a roof's lifespan is often determined by its installation," with one case study documenting 14 critical installation errors on a single failed roof.

CertainTeed draws the line clearly: "Contractors warrant their workmanship. Manufacturers warrant the roofing material against defects in manufacturing."

The real decision isn't just "how long" to warrant your work. It's what structure to use, who manages the claims, and who captures the profits.

Types of Roofing Warranty Programs Contractors Can Offer

If you're operating with no formal program or relying solely on manufacturer coverage, you're likely leaving money on the table while taking on unmanaged risk. Here are the four primary program models to evaluate against your business goals.

Basic Contractor Workmanship Warranty

This is the entry-level model: you self-issue a written guarantee (typically 1-10 years) covering installation errors at your own expense, with no third-party backing. Low-cost to set up, yes — but this model exposes you to unpredictable out-of-pocket claim costs with no mechanism to generate revenue from the warranty itself.

Duration range:

- CertainTeed states contractor workmanship warranties are "typically one to five years"

- NRCIA cites a broader 2-to-10-year range

- California mandates a 4-year minimum on installed items

Financial exposure: Every callback comes directly out of your pocket—truck roll costs, labor for rework, material replacement, and potential consequential damage liability. With roofing business failure rates at approximately 80-85% by year 3, uninsured claim exposure compounds cash flow strain and operational disruption.

Manufacturer-Backed Extended Warranty

Top-tier manufacturer certification programs allow contractors to register enhanced warranties combining material and workmanship coverage—backed by the manufacturer. This gives customers a named manufacturer standing behind the warranty, separating you from contractors offering standard coverage only, but coverage is tied to keeping your certification active, using full manufacturer system components, and following strict installation protocols.

Certification exclusivity:

- GAF Master Elite represents the top 2% of roofers

- CertainTeed SELECT ShingleMaster is available to approximately the top 1%

- Both require annual renewal, insurance minimums, and production thresholds

Workmanship coverage: GAF's Golden Pledge offers 25-30 years of workmanship coverage (available only to Master Elite contractors). CertainTeed's 5-Star SureStart PLUS provides 25 years workmanship coverage through SELECT ShingleMaster status. These programs shift significant warranty liability to the manufacturer, but the barrier to entry—and maintenance requirements—limits accessibility.

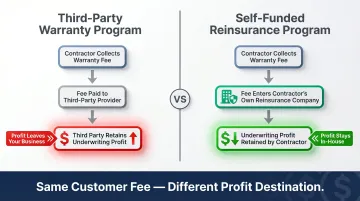

Third-Party Warranty Programs

Third-party warranty companies allow contractors to purchase and resell extended warranty coverage to customers—offloading claims risk to the provider. This reduces your financial exposure on claims, but the premium income is captured by the third-party company, not you.

The business trade-off: Third-party programs do eliminate your direct claims risk. The catch: they eliminate your profit opportunity at the same time. Warranty fees you collect flow to an outside company that retains underwriting profits — the premiums not used to pay claims. Those providers stay in business precisely because that margin is significant.

Self-Funded Reinsurance-Backed Programs

The reinsurance model is the most advanced option: you establish your own administrator-obligor entity (backed by A-rated insurers) that collects warranty premiums from customers, holds reserves, and pays claims—with you capturing underwriting profits.

Core financial logic: Warranty fees that previously flowed to a third-party provider are now retained in your own tax-advantaged reinsurance company. In low-claim periods, those premiums become direct profit. The structure also allows investment of premium reserves for additional ROI.

Your liability is limited to formation costs plus accumulated earnings. If your reinsurance company cannot meet financial obligations, the A-rated insurer provides the ultimate backstop — so your customers are protected regardless.

For contractors who qualify, this is the only model where the warranty program itself generates consistent income — rather than just managing risk.

Key Factors to Consider When Choosing a Warranty Program

The right program depends on business size, risk tolerance, growth goals, and operational capacity. Each factor below connects the program structure to measurable business outcomes.

Profitability and Revenue Potential

A warranty program should generate revenue, not just absorb costs. Third-party models extract premium income from your business; reinsurance models keep it.

The U.S. roofing industry generates $92.5 billion annually across approximately 109,000 businesses. The average residential roof replacement runs $9,540—meaning even a modest warranty fee per job compounds into significant revenue at volume.

With reinsurance structures, contractors retain 100% of underwriting profits instead of paying third-party providers. For example, on a $15,000 roof replacement with a built-in warranty fee, that fee flows into your reinsurance account rather than to an outside company—turning warranty obligations into recurring revenue.

Claims Risk Exposure and Control

Every warranty program transfers, retains, or shares claims risk differently. Understanding your exposure is critical before choosing a structure.

Severe convective storm insured losses have grown at 9.4% annually since 1990, and wind and hail alone drove 34.3% of all property damage claims in 2019. That trend makes proper risk modeling—not just a handshake guarantee—essential to protecting your margins.

A basic workmanship warranty with no reserve fund creates unpredictable financial liability after a bad storm season. Reinsurance-backed programs build reserves and are supported by A-rated insurers, limiting downside risk while keeping profit upside.

Customer Experience and Competitive Differentiation

The strength of the warranty you offer directly affects close rates, referrals, and premium pricing power.

Roofing Contractor magazine's consumer survey found 71% of contractors who won jobs offered enhanced warranties, versus only 30% of those who lost. Homeowners passed on quotes that were 17% lower than the contractor they hired—proof that warranty presentation influences revenue, not just margin.

Customers increasingly use warranty terms—coverage length, what's included, ease of claims—as a buying signal. Contractors offering robust, clearly explained programs win jobs that pure price competitors cannot.

Administrative Burden and Compliance Requirements

Warranty programs vary significantly in operational complexity:

- Basic workmanship guarantee: Minimal administration

- Manufacturer-backed programs: Certification maintenance and installation documentation

- Reinsurance programs: Company formation, compliance filings, claims adjudication, financial reporting

Choosing a program without accounting for administrative capacity can lead to compliance gaps or poor claims handling. Full-service program administrators can handle these functions on your behalf, eliminating burden while ensuring professional claims management.

Coverage Terms, Exclusions, and Transferability

The fine print determines real-world value to customers and your liability profile as a business.

Before committing to any program, review these variables:

- Coverage duration (1 year vs. 10 years vs. 25 years)

- What triggers a valid claim

- Exclusions (weather events, improper maintenance, unauthorized repairs)

- Whether the warranty transfers upon home sale

Most manufacturers allow a one-time transfer to a second owner, typically requiring formal notification within 30-60 days of home sale. Research shows that transferability of an extended warranty increases the resale price of used products—which raises consumers' willingness to pay for new ones.

When reviewing any warranty agreement, ask specifically what is excluded and under what conditions a claim can be denied. Ambiguous terms tend to favor whichever party wrote them.

Scalability as the Business Grows

The warranty program structure you choose today should not become a bottleneck at higher volume.

Basic workmanship warranties and manual third-party programs may work at 100 jobs per year. At 500+, they create unmanageable exposure or administrative friction. Evaluate whether a program scales with your install volume and geographic footprint—and whether the economics improve or erode as you grow.

Reinsurance-backed programs handle volume naturally. Every installation generates a warranty fee that flows into your reserve structure, so claim exposure and funding grow in proportion.

How WarrantyRE Can Help Roofing Contractors Build a Better Warranty Program

WarrantyRE helps roofing contractors move beyond basic workmanship guarantees and third-party programs. By establishing and managing their own administrator-obligor reinsurance companies, contractors keep the warranty profits their customers are already generating.

Founded in 1994 by Tim Byrd, WarrantyRE brings 30+ years of reinsurance experience, helping over 400 auto dealers become more profitable before expanding into the home service contractor space. The company provides a full-service model that handles legal formation, compliance, claims adjudication, staff training, bookkeeping, and performance reporting—so contractors don't have to manage the complexity alone. Here's what sets WarrantyRE apart for roofing contractors:

- Capture 100% of warranty profits previously paid to third-party providers

- Admin Obligor structure backed by A-rated insurers for added financial security

- Invest premium reserves for additional ROI beyond underwriting profits

- Transparent pricing with no hidden fees

- Fast company setup with structured onboarding and hands-on staff training

- Shared-success model — WarrantyRE only profits when contractor clients do

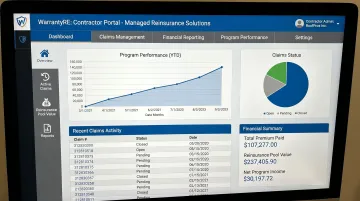

Contractors stay focused on their work while WarrantyRE manages claims from first call to final payout, handles all legal filings, and delivers monthly financial statements with periodic performance reviews. The result: a warranty program that generates profit instead of draining it.

Conclusion

Choosing a warranty program is one of the most financially strategic decisions a roofing contractor can make. The structure you choose determines who keeps the profit generated by your customer relationships—and that gap compounds over years.

The right program isn't the most popular one or the easiest sell—it's the one that fits your risk tolerance, operational capacity, and profitability goals. Each structure involves real trade-offs:

- Third-party programs eliminate claims risk but surrender underwriting profits

- Manufacturer-backed programs boost credibility but require ongoing certification

- Reinsurance-backed programs capture profits but need professional administration

Warranty program selection is not a one-time decision. As your roofing business grows in volume, market position, and financial sophistication, the right program structure will evolve. Contractors who reassess their program structure as their business scales tend to find that the reinsurance model becomes increasingly viable—and increasingly profitable. If you're at that point, speaking with a reinsurance program administrator like WarrantyRE can clarify whether capturing those underwriting profits makes sense for your operation.

Frequently Asked Questions

What is a typical warranty on a roof?

A homeowner receives two main components: a manufacturer's material warranty (typically 25–50 years, depending on shingle product and contractor certification) and a contractor workmanship warranty (ranging from 1 year to lifetime depending on the contractor's program). The quality of coverage depends heavily on which program structure the contractor has chosen.

What is the difference between a workmanship warranty and a manufacturer warranty?

The manufacturer warranty covers product defects in shingles and components, while the workmanship warranty—issued by the contractor—covers installation errors. Since most early roof failures are installation-related, that makes the workmanship warranty the more important of the two — for both the contractor and the homeowner.

What is a reinsurance-backed warranty program for roofing contractors?

A reinsurance-backed program lets a contractor establish their own warranty company, supported by A-rated insurers. Instead of paying premiums to a third-party provider, the contractor retains the underwriting profits — converting what was an expense into a profit center.

Can a roofing contractor create their own warranty company?

Yes, roofing contractors can establish their own administrator-obligor reinsurance company with the help of a program administrator like WarrantyRE, which handles legal formation, compliance, and ongoing administration so the contractor can focus on installation.

How do warranty programs help roofing contractors win more business?

A strong warranty program signals quality and confidence to homeowners, reduces price objection, and enables contractors to justify premium pricing. It also supports referrals and repeat business because customers feel protected long after the installation is complete.

How much does it cost to offer a warranty program for a roofing business?

Cost structure varies by program type:

- Basic workmanship warranties carry minimal direct cost but leave the contractor exposed to claims liability

- Third-party programs charge per-job fees paid to the provider

- Reinsurance programs involve setup and administration fees, but are designed to be net-profitable through retained premium income