That last question matters more than most contractors realize.

This article breaks down the four primary types of contractor warranty programs, what distinguishes each one, and what to consider when deciding which structure actually fits your business.

TL;DR

- Contractor warranty programs vary widely in structure — and that structure determines who absorbs the risk and who keeps the profit.

- The four types: manufacturer/product warranties, third-party warranty plans, self-administered workmanship warranties, and contractor-owned reinsurance programs.

- Third-party plans shift claims risk off the contractor, but the warranty company keeps the underwriting profits too.

- Contractor-owned reinsurance flips that model: the contractor captures premium income and controls the claims experience directly.

- The right choice depends on your install volume, risk tolerance, and whether profit retention is a business priority.

What Is a Contractor Warranty Program?

A contractor warranty program is a formal commitment to address defects, failures, or performance issues in work or installed products within a defined period and under specific conditions.

That definition sounds straightforward. The complexity lives in the business structure behind the commitment — how it's funded, who administers it, and who is legally obligated to pay when something goes wrong.

Warranty programs can cover three distinct things:

- Materials and equipment — defects in the products themselves

- Labor and workmanship — defects in how those products were installed

- Both — combined coverage under a single program

Most contractors think of a warranty as the written guarantee they hand to a customer. That framing is incomplete. A warranty program is also a financial and operational system — one that affects customer acquisition, repeat business, liability exposure, and revenue potential. How you structure it is a business decision with real consequences, not just a legal formality to check off.

Why Contractor Warranty Programs Matter for Your Business

The Competitive Reality

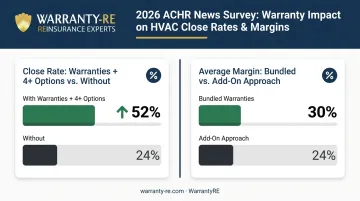

Customers increasingly expect coverage they can understand and rely on. A 2026 survey by ACHR News found that proposals including warranties and four or more options reached 52% close rates — yet only 10% of contractors used that approach. The contractors who can articulate exactly what they stand behind (and for how long) are closing more jobs.

The same survey found bundled warranties produced 30% average margins versus 24% when sold as add-ons. That's a structural pricing difference, not a sales skill difference.

What Happens Without a Defined Program

Contractors without a formal warranty structure absorb callback costs informally, with no mechanism to predict expenses or handle disputes consistently. The result is unpredictable overhead and margin erosion that compounds over time.

Without deliberate planning, common problems include:

- No reserves to offset repair costs

- No process for handling customer disputes consistently

- Callbacks charged directly to operating margins with no buffer

Some HVAC contractors historically set aside roughly 2% of new-construction job cost as a warranty reserve. That kind of discipline requires a defined program — not informal absorption.

The Financial Dimension

The type of warranty program you choose determines whether warranty-related revenue stays in your business or flows to someone else.

At one transaction, the difference may seem minor. Across hundreds of installs per year, the cumulative underwriting profit transferred to a third-party provider adds up fast — and knowing which program structure keeps that money in-house is the first step toward changing it.

Types of Contractor Warranty Programs

Warranty programs vary significantly in who bears financial risk, who administers claims, and how the program operates legally. Understanding these distinctions helps you make a deliberate choice rather than defaulting to whatever feels most familiar.

Manufacturer and Product Warranty

What it is: The equipment or materials supplier issues this warranty — not the contractor. It covers defects in the product itself (a failed HVAC compressor, a defective roofing shingle). The contractor passes it through to the customer on the manufacturer's behalf.

The contractor is a facilitator here, not the obligor.

What it covers (and doesn't): Major manufacturers are explicit about exclusions. GAF excludes damage from improper fastening or installation outside their instructions. Moen, Kohler, and Delta all exclude labor and improper-installation damage. Carrier's extended labor coverage depends on dealer program participation and registration within 90 days.

The pattern is consistent: product warranties cover the product. Your installation quality is your problem.

Best suited for: Contractors installing manufacturer-certified products where the brand carries meaningful consumer trust — common in HVAC, roofing, and plumbing.

Key trade-offs:

- No direct financial liability for the contractor on product defects

- Manufacturer controls how claims are handled

- Installation errors are excluded from coverage

- Offers no financial upside to the contractor beyond the initial job

Third-Party Warranty Plans

A contractor partners with an external warranty company to offer a structured protection plan — typically sold to the customer at the point of installation. The external company collects premiums, administers claims, and bears the payment obligation.

The contractor may receive a commission or markup. But the underwriting profit — the surplus of premiums collected over claims paid — belongs to the third-party company.

Best suited for: Contractors who want to offer customers a structured protection plan without taking on claims risk, particularly smaller or newer operations that lack the volume or infrastructure to manage warranty programs internally.

Key trade-offs:

- Low administrative burden for the contractor

- Customers get a marketable protection plan

- Contractor does not carry direct financial exposure for covered claims

- Contractor does not retain underwriting profits

- Customer claims experience is controlled by the third party — if it goes poorly, your reputation takes the damage

- At scale, the cumulative profit transferred to the warranty administrator can represent a significant lost revenue stream

WarrantyRE frames the third-party model with a pointed question contractors should ask themselves: If your warranty company weren't making a profit off you, would they continue doing business with you? The answer clarifies who the arrangement primarily benefits.

Self-Administered Workmanship Warranty

A direct commitment by the contractor to repair or redo defects in their own labor and installation within a defined period — typically one to two years — without involving a manufacturer or third party. The contractor funds and manages every claim internally.

Per NRCA guidance, there is no industry standard for workmanship warranty duration; many roofing contractors offer one or two years. HVAC contractors skew longer — the 2026 ACHR News survey found 10 years was the most common extended labor warranty duration among the 58% of HVAC contractors who offer them.

Best suited for: Contractors with strong quality control, experienced crews, and low historical callback rates. Often used as a supplemental commitment alongside manufacturer or third-party warranties.

Key trade-offs:

- Demonstrates confidence in workmanship and builds customer trust

- Zero administrative overhead or third-party cost

- Simple to communicate and honor

- All financial risk sits directly with the contractor

- A spike in callbacks in any given year hits cash flow with no mechanism to offset costs

- No recurring revenue component and no ability to accumulate reserves

The self-administered model works well as a standalone commitment for smaller operations — but it leaves one question unanswered: where does the money to cover claims actually come from? That's the gap the fourth model is designed to solve.

Contractor-Owned Reinsurance Program

The contractor establishes their own warranty or reinsurance company — functioning as the administrator and obligor. Customer premiums flow into the contractor's own entity, claims are paid from those reserves, and the surplus stays with the contractor.

This is the structure WarrantyRE specializes in helping home service contractors build and manage. Rather than paying a third-party company to hold and benefit from warranty funds, the contractor owns the structure and captures the underwriting profit.

How the admin obligor structure works:

- Warranty fees collected from customers flow into a trust account in the contractor's name

- A-rated insurers serve as the financial backstop — if the contractor's reinsurance company can't meet obligations, the insurer covers claims, limiting contractor liability to formation costs plus accumulated earnings

- Reserve funds are invested conservatively in government bonds, and investment income belongs to the contractor's reinsurance company

- Once reserves exceed 125% of unearned premiums, funds can be invested more aggressively at the owner's direction

- The program operates under IRS Code Section 831(b), which can allow smaller property and casualty companies to be taxed only on investment income — a tax planning advantage for contractors at serious volume

WarrantyRE handles full administration from first claim call to final payout: legal filings, compliance, bookkeeping, performance reporting, tax returns, and renewals. Contractors stay focused on their core business.

Best suited for: HVAC, roofing, plumbing, and electrical contractors with consistent install volume who are currently selling warranty or service agreements through a third-party provider. A common misconception is that this structure requires large volume or significant startup cost — WarrantyRE's FAQ is direct: neither is true.

Key advantages:

- Captures 100% of underwriting profit rather than sending it to a third party

- Contractor controls the claims experience and customer relationship

- Premiums generate investment income while held in reserve

- Creates a recurring revenue stream independent of new installations

- Structural tax planning benefits under IRS 831(b)

The tradeoffs are real but manageable with the right partner in place.

Key trade-offs:

- Requires proper legal setup, compliance infrastructure, and ongoing administration — not a plug-and-play arrangement

- Best results depend on working with an experienced reinsurance partner who handles the regulatory and administrative complexity

- Requires consistent premium volume to build meaningful reserves over time

How to Choose the Right Contractor Warranty Program

Choosing a warranty program comes down to your specific business model — install volume, administrative capacity, and whether you're positioned to capture the financial upside or just absorb the cost. No single structure fits every contractor, so evaluate these four factors before committing.

Four factors to evaluate:

Install volume and consistency — Self-administered workmanship warranties work at low volume. As installs scale, contractor-owned reinsurance becomes compelling — that's where premium accumulation starts generating meaningful profit.

Control over customer experience — If a third-party administrator handles claims poorly, the reputational damage lands on your business, not theirs. Evaluate how much control you actually want over the claims process.

Where the money goes — Trace exactly what happens to the premiums you collect or pass through. If a third-party company retains the underwriting surplus, quantify that gap annually — at scale, it adds up fast.

Administrative support available to you — Some structures require minimal internal involvement. Contractor-owned reinsurance requires a capable administrative partner. The question isn't whether the structure is complex — it's whether you have the right partner managing that complexity for you.

These four factors won't point to the same answer for every contractor. But working through them honestly narrows the field quickly.

Common Mistakes Contractors Make When Evaluating Warranty Programs

Three patterns come up repeatedly when contractors choose the wrong program structure — and each one is avoidable.

Staying with what's familiar rather than what fits. Many contractors keep a third-party warranty arrangement simply because it's what they've always done. Familiarity isn't a strategy. The arrangement may be serving the warranty company's goals far better than yours.

Underestimating the long-term cost of third-party commissions. A commission that looks acceptable at the transaction level looks very different across three years of consistent install volume. If your current provider retains underwriting surplus on every plan sold, that cumulative outflow is real revenue that could have stayed in your business. WarrantyRE offers a business analysis process specifically to help contractors quantify this gap.

Jumping to the most advanced structure without the right support. Contractor-owned reinsurance programs carry real financial advantages, but they require proper legal structure, claims administration, and compliance management. Vet your administrative partner carefully. Training, claims adjudication, compliance, bookkeeping, and legal filings should all be included in the arrangement — not treated as optional add-ons.

Frequently Asked Questions

What are the different types of construction warranties?

The four main categories are manufacturer/product warranties, third-party service agreements, self-administered workmanship warranties, and contractor-owned reinsurance programs. Each differs in who bears the financial risk, who administers claims, and who retains the financial benefit when premiums exceed claims.

What is the difference between a workmanship warranty and a manufacturer warranty?

A workmanship warranty covers defects in the contractor's labor and installation quality. A manufacturer warranty covers defects in the product or equipment itself. Both can — and often should — exist simultaneously, since most manufacturer warranties explicitly exclude improper installation damage.

How long should a contractor warranty last?

Duration varies by program type, trade, and state law. Workmanship warranties commonly run one to two years per NRCA guidance; HVAC extended labor warranties frequently reach 10 years. Equipment warranties can extend five years or more depending on the manufacturer, product tier, and registration requirements.

What is a contractor-owned warranty reinsurance program?

It's a structure where the contractor establishes their own warranty company, collects customer premiums into that entity, pays claims from reserves, and retains the underwriting profits — rather than transferring those profits to a third-party warranty administrator. A-rated insurers serve as the financial backstop.

Are contractor warranties legally required?

Requirements vary by state and trade. Minnesota imposes statutory warranties for new dwellings covering one year for workmanship, two years for mechanical systems, and 10 years for major structural defects. Arizona, Tennessee, Virginia, and other states impose their own standards and obligations.

What happens if a contractor doesn't honor their warranty?

Consequences include financial liability for repairs, potential civil litigation, licensing board complaints, and reputational damage. Tennessee and Virginia both treat failure to honor warranty terms as contractor misconduct subject to disciplinary action. Contractors using a properly funded reinsurance structure have dedicated reserves in place specifically to cover these obligations when claims arise.