This guide covers the full process: what a warranty insurance claim is, what documentation you need, the authorization sequence you must follow, and why that sequence matters. It's written for both policyholders navigating the process as customers and for contractors and dealers who administer warranty programs and need to understand how claims function operationally.

TL;DR

- Verify coverage and contact your warranty administrator before any repairs begin — authorization is non-negotiable.

- The five most common denial triggers: non-covered items, unauthorized repairs, missed deadlines, incomplete documentation, and no maintenance records.

- Under a third-party program, a separate company controls your claims. Under a contractor-owned reinsurance structure, the contractor controls the outcome.

- Contractors who own their warranty program retain underwriting profits and claims control — with full administrative support behind them.

What Is a Warranty Insurance Claim?

A warranty insurance claim is a formal request submitted by a contract holder asking the warranty administrator or insurer to cover the cost of a qualifying repair, replacement, or service call under the terms of an active warranty agreement.

When approved, the claim results in one of three outcomes:

- Direct payment to the service provider

- Reimbursement to the policyholder

- Dispatch of an authorized technician

Where confusion tends to creep in is what actually qualifies — and that's where the line between warranty claims and property insurance claims matters.

How Warranty Claims Differ from Property Insurance Claims

Warranty insurance claims are triggered by normal wear, mechanical failure, or workmanship defects — not accidents or unforeseen damage events.

As the FTC notes in its guidance on auto service contracts, service contracts typically do not cover damage from an accident. That falls under property or liability insurance. A compressor that fails after seven years of normal use is a warranty claim. A compressor damaged when a tree falls on the unit is not.

The NAIC Service Contracts Model Act defines service contracts as agreements covering operational or structural failure due to defects in materials, workmanship, or normal wear and tear.

Why the Claims Filing Process Matters

A poorly managed claims process doesn't just frustrate customers — it creates regulatory and financial exposure for everyone involved.

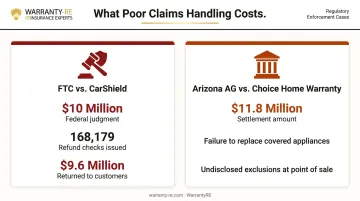

The FTC's 2024 enforcement action against CarShield resulted in a $10 million judgment after customers' claims for advertised covered systems were frequently denied due to exclusions. The FTC then sent 168,179 refund checks totaling over $9.6 million to affected customers.

Separately, an Arizona Attorney General settlement with Choice Home Warranty reached $11.8 million after complaints that the company failed to replace advertised covered appliances and that sales representatives did not disclose exclusions.

For contractors running warranty programs, these cases carry a direct lesson: how claims are handled — and who controls that process — determines both customer outcomes and legal exposure.

Why It Matters for Contractors and Dealers

For contractors and dealers administering warranty programs, how claims are handled directly shapes customer retention and program profitability. The structural difference between two common program types matters here:

- Third-party warranty programs: Claims are adjudicated by an outside administrator whose financial incentive may be to minimize payouts. The contractor has no control over the outcome, the service provider used, or how disputes are resolved.

- Contractor-owned reinsurance structures: The contractor owns the reinsurance company. Claims are administered on their behalf, service decisions stay within the contractor's ecosystem, and underwriting profits — the money left after claims are paid — remain with the contractor rather than flowing to a third party.

- Full-service administration: Contractors don't manage adjusters or claims paperwork directly — an administrator handles adjudication, compliance, and financial reporting on their behalf, while the contractor retains control over how customers are treated.

WarrantyRE works with HVAC, roofing, plumbing, and electrical contractors to establish contractor-owned reinsurance structures. Their administration team handles claims from intake through resolution — adjudication, compliance, and financial reporting — so contractors stay focused on their business rather than claims logistics.

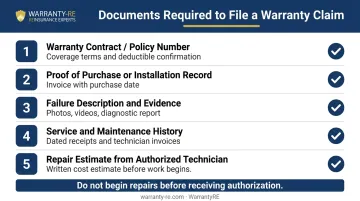

What Documents Are Needed to File a Warranty Insurance Claim

Submitting an incomplete claim is one of the most avoidable reasons for delays and denials. Have these documents ready before you contact the administrator:

- Warranty contract or policy number — confirms your coverage terms, exclusions, and deductible amounts. Review it before you call, not after.

- Proof of purchase or installation record — for HVAC or home service work, this is the installation invoice or sale record showing the purchase date.

- Description and evidence of the failure — a written account of what failed and when, plus any photos, videos, or diagnostic reports. For HVAC and mechanical systems, a technician's diagnostic report is usually required before authorization is granted.

- Service and maintenance history — administrators use these records to confirm the failure resulted from normal use, not neglect. The California Department of Insurance notes that a claim may be denied if the consumer cannot prove proper maintenance. Keep dated receipts and technician invoices for every service call.

- Repair estimate from an authorized technician — most administrators require a written cost estimate before approving any work. Starting repairs without pre-authorization is one of the fastest ways to void coverage.

How to File a Warranty Insurance Claim: Step-by-Step

The claims process follows a specific sequence. Deviating from it — especially by making repairs before authorization — is a primary cause of denial.

Step 1: Review Your Contract Before Contacting Anyone

Locate and read the warranty contract to confirm:

- The damaged item or system is actually covered

- No applicable exclusions apply (pre-existing conditions, improper installation, cosmetic damage)

- You note the claim submission deadline — most programs require notice within a defined window after a failure is identified

Step 2: Contact Your Warranty Administrator Promptly

Contact the administrator via phone, online portal, or email at the first sign of a problem. Waiting increases risk in two ways: the submission window may close, and additional damage that occurs after the initial failure may not be covered.

Document every contact: names, dates, confirmation numbers. This record protects you if the claim is disputed later.

Step 3: Submit Required Documentation

Gather and submit the documents the administrator requests. Common requirements include:

- Proof of purchase or installation date

- Original warranty contract or coverage agreement

- Photos or written description of the failure

- Prior service records relevant to the issue

- Any diagnostic reports from an initial inspection

Describe the issue clearly and confirm coverage with the administrator before assuming the claim will proceed. Digital submissions typically speed up processing. Incomplete submissions are a primary cause of delays — the review cannot move forward without all required materials.

Step 4: Receive Authorization Before Repairs Begin

The California Department of Insurance explicitly warns that repairs performed without prior authorization may result in a denied claim. The administrator must issue a claim authorization number — which is a promise to pay for the specific repair — before any work starts.

For costly or complex repairs, the administrator may send an independent inspector or require a diagnostic teardown (disassembly to confirm the failure cause) before authorization is issued.

Step 5: Complete Repairs and Finalize Payment

Once authorized:

- An approved technician completes the work

- You pay only the applicable service fee or deductible

- Your warranty program pays the technician directly or reimburses the remaining balance

Keep the final repair invoice and all communications. You may need them for follow-up claims or if a dispute arises.

Common Reasons Warranty Insurance Claims Get Denied

Filing for Non-Covered Items or Excluded Conditions

One of the most frequent denial triggers is claiming for a repair that falls under a contract exclusion — pre-existing conditions, cosmetic damage, pest damage, or improper installation. The Arizona AG's investigation into Choice Home Warranty found that sales representatives frequently failed to disclose these exclusions at the point of sale, leaving customers to discover them only when a claim was filed.

Reading the contract before filing — and flagging ambiguous exclusions early — is the most reliable way to avoid this outcome.

Starting Repairs Without Pre-Authorization

Performing repairs before the administrator approves the claim almost always voids coverage — regardless of whether the underlying damage would have qualified. This catches both policyholders and contractors off guard.

Without authorization, the administrator has no opportunity to verify the failure, select an approved technician, or confirm the repair scope. That step exists to protect the integrity of the review process, not to create delays.

Missing Deadlines or Submitting Incomplete Documentation

Most warranty programs require claim notice within a defined period after a failure is identified. Missing that window eliminates the claim. Equally, submitting without supporting documentation — no photos, no maintenance records, no estimate — stalls or terminates the review process.

No Maintenance History or Evidence of Neglect

Warranty programs cover failures from normal use — not deferred maintenance or negligence. If a failure is attributable to years of skipped service calls, the administrator has grounds to deny.

Keep these records on file and readily accessible:

- Annual or seasonal service invoices with dates and technician signatures

- Manufacturer-recommended maintenance logs

- Receipts for filter replacements, tune-ups, or inspections

- Any correspondence about prior repairs or known issues

Conclusion

Most denied claims trace back to the same mistakes: coverage gaps no one reviewed upfront, repairs started before authorization, and missing documentation. Know what your contract covers, act at the first sign of a problem, collect the right paperwork, and wait for written approval before any work begins.

For contractors and dealers running warranty programs, understanding the process from both sides matters. How claims are handled determines whether customers trust the program — and whether the program stays financially viable.

Contractors who control their claims process, rather than deferring it to a third-party administrator, are better positioned to deliver consistent outcomes while retaining the underwriting profits the program generates.

WarrantyRE works with contractors across HVAC, roofing, plumbing, and electrical trades to build reinsurance programs where contractors legally own the warranty company and control the full claims experience, with WarrantyRE managing claims adjudication, compliance, and financial reporting in the background.

Frequently Asked Questions

How do I submit a warranty reinsurance claim?

Contact your warranty administrator by phone or online portal, provide your contract details and a description of the failure, and submit required documentation before repairs begin. The exact process depends on whether the program is administered by a third party or through a contractor-owned reinsurance structure like WarrantyRE's.

What documents are needed to file a warranty reinsurance claim?

You'll need your warranty contract or policy number, proof of purchase or installation, a written description of the failure with supporting photos or diagnostic reports, maintenance and service history, and a cost estimate from an authorized technician.

How long does it take for a warranty insurance claim to be processed?

Some states set minimum response windows — California, for example, requires home protection contracts to initiate services within 48 hours of a service request. More complex claims involving inspections or disputes take longer. Submitting complete documentation upfront is the most reliable way to avoid unnecessary delays.

What are the most common reasons warranty insurance claims get denied?

The top reasons: filing for non-covered or excluded items, starting repairs without pre-authorization, missing the submission deadline, and submitting incomplete documentation or lacking maintenance records.

Can I file a warranty insurance claim after repairs have already been completed?

In most cases, completing repairs before receiving authorization voids coverage for those repairs. Some programs allow emergency exceptions, but this must be confirmed with the administrator before any work proceeds, not after the fact.

What is the difference between a contractor-owned warranty program and a third-party warranty?

Under a third-party warranty, claims are adjudicated by an outside company whose financial interest may favor minimizing payouts. Under a contractor-owned reinsurance structure, the contractor controls how claims are evaluated and fulfilled, typically resulting in faster resolution and underwriting profits that stay within the business rather than going to an outside provider.