Introduction

A new roof runs $10,000 to $20,000 or more in Michigan — and most homeowners have no idea what their warranty or insurance policy actually covers until water is coming through the ceiling.

The confusion is understandable. A single Michigan home can have three separate warranties active at once, each covering something different and excluding everything else.

Layered on top of that is a homeowners insurance policy with its own covered perils, deductibles, and valuation methods — factors that can mean the difference between a full replacement check and a fraction of what you expected.

That coverage complexity is compounded by Michigan's climate. Freeze-thaw cycles, lake-effect snow loads, and regular hail events stress roofing systems far harder than most of the country — and that wear creates warranty and coverage situations that simply don't arise in milder climates.

This guide breaks down the three types of roofing warranties, what homeowners insurance actually pays for, how to file a storm damage claim, and how Michigan roofing contractors can build warranty programs that protect their customers and their business.

TL;DR: What Michigan Homeowners and Contractors Need to Know

- Most roofs carry up to three warranties — manufacturer material, contractor workmanship, and extended system — each covering something different

- Homeowners insurance covers sudden storm damage but not wear and tear, installation defects, or neglect

- Michigan's freeze-thaw cycles, lake-effect snow, and hail events create warranty and coverage situations that don't exist in stable climates

- DIY repairs, poor ventilation, and skipped maintenance can void all three warranties at once

- Choose contractors whose workmanship warranties are backed by a reinsurance structure — not just a standard third-party plan

The Three Types of Roofing Warranties in Michigan

Manufacturer's Material Warranty

This warranty comes from the shingle manufacturer — GAF, CertainTeed, or Owens Corning — and covers defects in the product itself: premature granule loss, cracking, blistering, or manufacturing failures. It does not cover improper installation, storm damage, or labor costs unless the homeowner qualifies for an enhanced plan.

Coverage durations vary significantly:

- GAF offers a Lifetime term on qualifying shingles, but the non-prorated Smart Choice period is only 10 years under basic coverage. After that, payouts shrink as the roof ages.

- CertainTeed provides full material and labor replacement cost during its SureStart period (typically 10 years) on most laminated shingle lines.

- Owens Corning follows a similar structure, with a 10-year TRU PROtection non-prorated period on standard coverage.

All three structures are prorated after the initial coverage period. A basic material warranty on a 15-year-old roof may cover only a small fraction of replacement cost — that shrinkage is intentional, not an oversight.

To qualify for non-prorated extended coverage — sometimes up to 50 years — the entire roofing system must use matching manufacturer components: underlayment, starter strips, ridge cap, ventilation, and flashing. Installation must also be performed by a credentialed contractor in that manufacturer's program.

Contractor Workmanship Warranty

The workmanship warranty comes from the roofing contractor, not the manufacturer. It covers problems caused by how the roof was installed — improper flashing, nail placement errors, poor sealing, misaligned shingles. If those installation mistakes cause a leak, this is the warranty that should respond.

Key facts Michigan homeowners should know:

- Standard workmanship warranties run 1 to 2 years, per NRCA guidance

- Some Michigan contractors extend this to 5 or 10 years voluntarily

- Certified contractors in manufacturer programs can offer manufacturer-backed workmanship coverage up to 25 years

- The warranty is only as reliable as the contractor behind it — if the company closes in year four of a 10-year warranty, that protection disappears entirely

Extended System (Enhanced Manufacturer) Warranty

When a certified contractor installs a complete matched system using one manufacturer's components, some manufacturers offer comprehensive system warranties that go well beyond basic material coverage. These enhanced plans typically include:

- Both materials and labor (including tear-off and disposal)

- Non-prorated coverage periods extending to 50 years

- Transferability to new homeowners (a real selling point at resale)

- Manufacturer-backed workmanship protection

Understanding which plan covers what prevents the most common claim disputes. Here's how they compare:

| Warranty Type | What It Covers | What It Excludes |

|---|---|---|

| Manufacturer material warranty | Product defects (cracking, blistering, granule loss) | Installation errors, storm damage, labor |

| Contractor workmanship warranty | Installation quality | Material defects, storm damage |

| Extended system warranty | Both materials and labor under one plan | Anything outside a fully matched, credentialed install |

Each warranty addresses a different failure mode. A roof with only manufacturer coverage has no protection against installation errors — which are responsible for a significant share of premature roof failures in Michigan's freeze-thaw climate.

What Michigan Homeowners Insurance Actually Covers for Roof Damage

What's Typically Covered

Standard Michigan homeowners insurance covers sudden, accidental damage from named perils. For roofs, that means:

- Hail strikes

- High-wind damage

- Fallen trees or debris

- Ice dams (subject to policy terms and maintenance conditions)

- Fire

According to the Insurance Information Institute, wind and hail represent the largest category of homeowners insurance claims, with 2.8% of insured homes experiencing a wind or hail loss in any given year. In Michigan, with its regular lake-effect storms and hail seasons, roof claims are among the most common insurance events homeowners face.

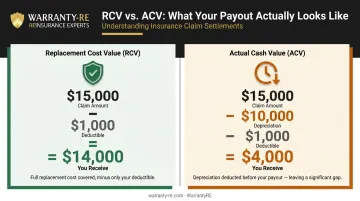

RCV vs. ACV: the most important distinction in any policy:

| Policy Type | How It Pays | Example ($15,000 Claim, $1,000 Deductible) |

|---|---|---|

| Replacement Cost Value (RCV) | Full replacement at today's cost | $14,000 paid |

| Actual Cash Value (ACV) | Replacement cost minus depreciation | $4,000 paid (if $10,000 depreciation applied) |

This example comes directly from NAIC's consumer guidance, and it illustrates why policy type matters so much. An older roof on an ACV policy can generate a fraction of what the homeowner expects. Contractors working with insurance-involved projects should verify policy type upfront — it directly shapes what's recoverable and how the conversation with the homeowner goes.

Michigan also updated its rules in 2024: DIFS announced that insurers may not depreciate labor in standard ACV calculations, with changes taking effect January 2025. Optional endorsements may still allow labor depreciation in exchange for lower premiums — another policy detail worth verifying.

What's NOT Covered

Homeowners insurance is not a maintenance program. Insurers routinely deny claims when they determine damage resulted from neglect rather than a sudden covered event. What's excluded:

- Normal wear and tear

- Manufacturer defects (that's what the material warranty addresses)

- Installation errors (that's the workmanship warranty)

- Damage from deferred maintenance — rotted decking, long-ignored flashing failures, blocked gutters

Some Michigan policies also carry wind or hail exclusions, higher deductibles for named storm events, or age-based limitations that reduce payouts on older roofs. Contractors should know which exclusions their customers' policies carry — it directly affects claim outcomes and post-storm conversations with homeowners.

One more dynamic to understand: after major storms, out-of-area contractors often arrive promising that "insurance will cover everything." Storm chasers can overstate coverage and complicate how claims are filed. Licensed Michigan contractors who understand the actual scope of damage — and how it maps to policy thresholds — are better positioned to serve customers honestly and protect their own reputation in the process.

How to File a Roof Insurance Claim in Michigan: Step by Step

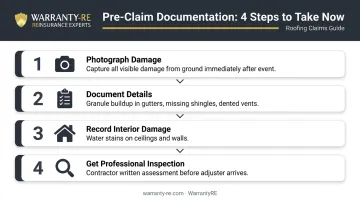

Before You File: Document Everything First

The order of operations matters. Most homeowners call their insurer before documenting anything — and that sequence often costs them.

Document damage before you call anyone:

- Photograph all visible damage from the ground immediately after the event

- Capture granule buildup in gutters, displaced or missing shingles, dented vents and gutters

- Record any interior water stains on ceilings or walls

- Note the date and, if possible, the storm event (NOAA weather records can support your claim)

Drone footage from a licensed contractor can capture damage invisible from ground level and often becomes critical evidence in a successful claim. Have a professional inspection completed before your insurer's adjuster arrives. A Michigan-licensed roofing contractor can assess the full scope of damage, provide a written estimate, and help you understand whether the damage exceeds your deductible — all before you're committed to an adjuster's assessment.

Note that DIFS advises homeowners to contact their insurer promptly after a loss and before hiring contractors for repair work. The two steps aren't mutually exclusive: notify your insurer, then get your contractor's written assessment ready before the adjuster's visit. Going in without documentation often results in underestimated claims.

Working With Your Adjuster and Contractor

When the adjuster visits, they assess the damage, estimate repair costs, and determine payout based on your coverage type (RCV or ACV). Three things every Michigan homeowner should understand before that meeting:

- You have the right to have your contractor present during the adjuster's inspection. A contractor's written damage assessment can support or dispute the adjuster's findings — and sometimes makes a significant difference in the outcome.

- Understand your deductible before signing anything. If your deductible is $2,500 and the adjuster estimates $2,400 in damage, no check is issued.

- Be cautious of any contractor offering to "waive" your deductible. This practice raises serious legal concerns. Michigan's insurance fraud statutes under MCL 500.4503 and MCL 500.4511 make fraudulent insurance acts a felony punishable by up to 4 years imprisonment and fines up to $50,000. Proposed legislation (HB 4713/HB 4714, introduced in 2025) would specifically prohibit contractors from paying or rebating deductibles — treat any such offer as a red flag.

DIFS also requires insurers to inform claimants within 30 days what information is needed for proof of loss, and to pay claims within 60 days of receiving that documentation.

How Michigan's Climate Affects Your Warranty and Coverage

Michigan's weather creates roofing stresses that simply don't apply in calmer climates. Three factors stand out.

Freeze-thaw cycling is one of the most destructive forces acting on Michigan roofs. GLISA research documents that water expands by approximately 9% when it freezes — meaning any water that has worked its way into small cracks, seams, or gaps in underlayment or flashing expands and contracts repeatedly throughout fall, winter, and spring. This thermal cycling degrades sealants and flashing faster than in stable climates and shortens the effective lifespan of roofing systems.

That degradation shows up in claims data. Michigan recorded 53 billion-dollar weather and climate disasters between 1980 and 2024, with the annual average climbing from 1.3 events per year to 4.4 events per year in the 2020–2024 period — a pattern that directly affects how often warranties and coverage are put to the test.

Ice dams form when heat escaping through the roof deck melts snow near the peak, and that meltwater refreezes at the cold eaves, forcing water back under shingles. According to NWS Grand Rapids, undetected ice dams can cause structural damage and interior water intrusion. The coverage trap: if inadequate attic insulation or ventilation caused the ice dam, neither the workmanship warranty nor homeowners insurance may respond. That's the homeowner's maintenance responsibility, and insurers know it.

Hail and wind frequency in Michigan's Lower Peninsula is higher than most of the country. For new installations, the practical response is straightforward:

- Ask about shingles with a Class 4 impact resistance rating (the highest available)

- Confirm wind uplift ratings match Michigan's exposure levels

- Check whether your insurer offers premium discounts for impact-resistant materials — many do

These upgrades cost more upfront but can reduce both out-of-pocket claims costs and annual premiums.

How Michigan Roofing Contractors Can Build a Stronger Warranty Program

Here's the structural problem most Michigan roofers don't talk about: a standard 1-to-5-year workmanship warranty is backed entirely by the contractor's own business. If a claim comes in during a slow quarter, honoring it hurts. If the company experiences a tough year and closes, the warranty disappears entirely — leaving homeowners with no recourse.

Meanwhile, third-party warranty companies collect premium fees, retain underwriting profits on all the warranties that never generate claims, and leave the contractor with the risk and the paperwork.

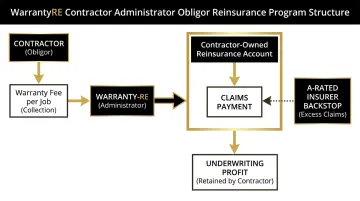

A different model exists. Some Michigan contractors are now establishing their own administrator obligor reinsurance structures — programs that allow them to collect warranty fees built into every job, hold those funds in a legally owned reinsurance account, cover claims when they arise, and retain unused funds as underwriting profit.

Here's how the structure works in practice:

- A warranty fee is included in every job price and flows into the contractor's own reinsurance account

- When a claim comes in — a leak, a flashing failure, a callback — it's paid from that pool

- Unused funds stay with the contractor, not a third-party provider

- The structure is backed by A-rated insurers, so if reserves are ever insufficient, there's a financial backstop

That's exactly the kind of program WarrantyRE has helped contractors across the country build. The company handles all administration — claims adjudication, compliance filings, tax returns, financial reporting — so the contractor's crew stays focused on roofing, not paperwork.

The result is a workmanship warranty that doesn't evaporate when cash flow gets tight — for the contractor. For the homeowner, it means protection backed by a real financial structure, not just a promise tied to the contractor's current bank balance.

In a competitive Michigan roofing market, that's a meaningful differentiator — especially when a homeowner is comparing bids from three companies and trying to evaluate which warranty offer actually means something.

Frequently Asked Questions

How do you get a free roof from insurance?

Insurance pays for roof replacement only when damage results from a covered peril (hail, wind, fire) and when repair costs exceed your deductible. A "free roof" isn't guaranteed — it depends on your policy type, deductible amount, roof age, and what the adjuster determines caused the damage. ACV policies and high deductibles often mean the homeowner still pays a significant portion.

Does homeowners insurance cover full roof replacement in Michigan?

Full replacement may be covered under RCV policies when a covered storm event causes widespread damage. ACV policies subtract depreciation, and those with age-based limits or wind/hail exclusions may cover only partial costs or deny the claim outright. Review your declarations page and ask your agent how your roof would be valued before a claim arises.

What voids a roofing warranty in Michigan?

The most common voiding conditions are DIY repairs that alter the roofing system, failure to perform required maintenance (gutters, ventilation, annual inspections), poor attic ventilation, and using materials from a different manufacturer on an extended system warranty. Any of these can void all three warranty types simultaneously.

What is the difference between a manufacturer warranty and a workmanship warranty?

The manufacturer warranty covers defects in the materials themselves — premature granule loss, cracking, blistering. The workmanship warranty covers how the contractor installed those materials — leaks from improper flashing, nail errors, poor sealing. Both are required for complete protection; neither replaces the other.

How long should a roofing workmanship warranty last?

Standard workmanship warranties run 1 to 2 years per NRCA guidance, but reputable Michigan contractors often offer 5 to 10 years. Certified contractors in manufacturer programs can extend that to 25-year manufacturer-backed workmanship coverage. Always confirm the warranty is in writing and know which company is actually backing it.

Can Michigan roofing contractors offer their own warranty instead of relying on a third-party plan?

Yes. Contractors can establish their own administrator obligor reinsurance structures that allow them to underwrite their own workmanship warranties, collect and retain underwriting profits, and cover claims from a financially sound reserve backed by A-rated insurers. WarrantyRE helps roofing contractors build and administer exactly this kind of program nationwide.