Introduction

Picture this: an HVAC contractor receives a callback on a $12,000 system installation completed six months ago. The compressor is failing, and the homeowner is expecting free repairs under the one-year labor warranty. The contractor pulls a two-man crew off a scheduled job, losing $450 in direct labor and fuel costs.

Add the $300 in forfeited opportunity revenue from the missed installation, and a single callback just consumed nearly $750—straight from profit margins running just 5-7% for most residential HVAC contractors.

Now imagine that scenario repeating itself. Industry benchmarks place acceptable HVAC callback rates at 2-2.5%, but many contractors start far higher—one profiled in ACHR News discovered his initial callback rate exceeded 25%.

At a 5% callback rate, annual warranty losses can top $100,000. Without a dedicated reserve fund, each claim hits operating cash flow directly—creating the exact cash flow crises that drive 82% of small business failures.

This guide provides a practical, step-by-step approach to building a warranty reserve fund specifically for home service contractors (HVAC, roofing, plumbing, and electrical). You'll learn how to calculate the right reserve amount based on your actual claim history, where to hold those funds, when to adjust your accruals, and how to properly record reserves in your books so warranty costs stop blindsiding your cash flow.

TLDR:

- A warranty reserve covers future claims from a dedicated account—not an emergency fund, but a forward-looking liability

- Calculate your reserve: multiply your historical claim rate (%) by total revenue currently under active warranty

- Set aside 1-5% of each job's revenue into a separate account and record it as a liability on your balance sheet

- Review quarterly, adjust accrual rates annually based on actual claims data

- Contractor-owned reinsurance converts warranty programs from cost centers into profit centers

What Is a Warranty Reserve Fund and Why Home Service Contractors Need One

A warranty reserve fund is a dedicated pool of money set aside at the time of each job to cover the cost of future warranty claims, callbacks, and defect repairs. It's not an emergency fund or a general savings account—it's a forward-looking financial liability that matches the cost of warranty work to the revenue that created the obligation in the first place.

Why This Matters for Home Service Contractors

Unlike manufacturers who spread warranty risk across thousands of identical units, home service contractors offer warranties on individual projects: a roof, an HVAC installation, a plumbing system replacement, an electrical service upgrade. Unlike manufacturers who spread warranty risk across thousands of identical units, home service contractors offer warranties on individual projects: a roof, an HVAC installation, a plumbing system replacement, an electrical service upgrade. Each project carries its own unique risk — and the dollar figures make that risk concrete:

- Average residential HVAC installation: ~$7,500

- Roof replacement: $6,000–$12,000

- Single warranty claim on a $15,000 job: can consume 5–10% of contract value

A callback that costs $650 in technician time represents nearly 9% of a $7,500 HVAC job. At the industry-standard 5-7% net profit margin, that single callback wipes out the entire profit from the original installation. At a 2–2.5% callback rate, those losses compound across every job you complete.

Reserve vs. Accrual: Understanding Both Terms

Many contractors confuse warranty reserve with warranty accrual, but both work together:

- Warranty accrual is the ongoing action—the percentage of job revenue you transfer into the reserve account at each job completion

- Warranty reserve is the accumulated balance held in the dedicated account to pay future claims

Think of the accrual as the monthly deposit and the reserve as the total balance. Under accounting standards (specifically ASC 450-20 for assurance-type warranties), you must record warranty obligations as a liability when they're both probable and reasonably estimable. That threshold is met the moment you complete a warranted job.

How to Calculate Your Warranty Reserve Amount

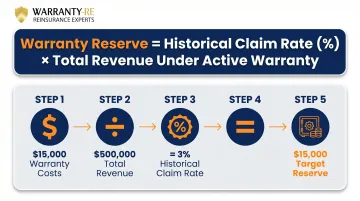

The Foundational Formula

Warranty Reserve Needed = (Historical Claim Rate %) × (Total Revenue Under Active Warranty Coverage)

Example: An HVAC contractor has completed $500,000 in installations over the past 18 months, all still under active warranty. Historical warranty costs over that period totaled $15,000. The claim rate is 3% ($15,000 ÷ $500,000). The target reserve is $15,000.

Determining Your Historical Claim Rate

Calculate your claim rate by dividing total warranty-related costs paid over the past 12-24 months by total revenue from jobs still under warranty in that same period. Every cost category counts:

- Technician labor and parts

- Fuel and vehicle time

- Administrative overhead

- Opportunity costs from pulling crews off paying work

If you're just starting out and lack historical data, use industry benchmarks:

- HVAC contractors: 2-2.5% of service calls is considered acceptable; SMACNA recommends starting at 2% of equipment cost

- Roofing, plumbing, electrical: Limited published benchmarks exist, but starting at 2-3% of job revenue is a reasonable baseline until you build your own data

Accounting for Warranty Term Length

Your reserve must cover the full remaining warranty period on all active jobs. A job with a two-year warranty completed six months ago still has 18 months of exposure.

Action step: Map out your active warranty obligations by job:

- Job ID, completion date, warranty term length, remaining coverage months

- Original job revenue and amount accrued to reserve

- Claims paid to date against that job

Job-level tracking also makes it straightforward to recalibrate when you extend warranty terms or roll out new service offerings — changes that directly affect your total exposure.

Adjusting for Job Complexity and Risk

That job-level view matters especially because not all jobs carry equal warranty risk. New product lines, subcontracted work, and equipment with known reliability issues should carry higher accrual rates than routine work.

Example: An HVAC contractor introducing geothermal system installations might set a 4-5% accrual rate until 12 months of claims data exists, versus 2% for standard furnace replacements with established reliability.

Calculating Reserve Capacity

Reserve Capacity (in months) = Current Reserve Balance ÷ Average Monthly Claims Cost

If your reserve holds $18,000 and you average $1,000 per month in warranty claims, your reserve capacity is 18 months. For home service contractors, a healthy target is 12-24 months of claims coverage, calibrated to the length of warranties offered.

How to Set Up and Fund Your Warranty Reserve Account

Open a Dedicated Account

Establish a separate business savings or money market account exclusively for warranty reserves. Do not co-mingle these funds with operating accounts. Co-mingling leads to three critical failures:

- Accidental spending on non-warranty costs

- Inaccurate financial statements that hide true profitability

- Inability to honor claims when multiple callbacks hit simultaneously

The Accrual Method: How to Fund Your Reserve

At the close of each job (or each billing cycle), transfer a fixed percentage of job revenue into the reserve account.

Typical accrual percentage ranges:

- SMACNA recommends 1-2% of equipment cost or $25 per ton for HVAC contractors, starting at 2%

- Aptora recommends 1-2% of job income across trades

- Most contractors settle in the 2-4% range depending on trade type, warranty term length, and historical claims experience

Consult your accountant to set the right rate for your specific business.

Bookkeeping Treatment: Recording Reserves Properly

At job completion, record the accrual:

- Debit: Warranty Expense (operating expense on income statement)

- Credit: Warranty Reserve Liability (current liability on balance sheet)

When a claim is paid:

- Debit: Warranty Reserve Liability

- Credit: Cash

This treatment ensures warranty obligations appear as liabilities on your balance sheet from the moment you complete the job, not when the claim arrives. It's the proper accounting method under ASC 450-20 for assurance-type warranties and keeps financials audit-ready.

Managing Cash Flow During the Ramp-Up Period

For new contractors without an existing reserve balance, the ramp-up period is real — start accruing on day one and build the fund steadily from your first job forward. Prioritize reserve building before:

- Expanding warranty offerings beyond one year

- Offering extended service contracts

- Aggressively marketing warranty coverage as a competitive differentiator

Consider reducing warranty terms temporarily (for example, offering six-month coverage instead of one year) until reserves can cover the full term.

Investment Strategy for Larger Reserves

Once your reserve reaches 12+ months of claims coverage, move idle funds into low-risk, interest-bearing vehicles:

- High-yield savings accounts: Currently offering ~4% APY

- Money market accounts: Similar rates with potential check-writing privileges

- Short-term CDs: Rates up to 4.20% APY

That passive return is valuable — but it's just the starting point. Contractor-owned reinsurance programs take this further: rather than simply earning interest on reserves, contractors capture the underwriting profits that third-party warranty providers have been keeping for themselves.

Managing and Adjusting Your Reserve Over Time

Conduct Quarterly Reserve Reviews

Every quarter, compare your current reserve balance against your calculated reserve target. Calculate:

- Total active warranty exposure (revenue under warranty)

- Actual claims paid in the quarter

- Reserve balance vs. target reserve

- Reserve capacity in months

Two triggers require immediate review:

- Spike in claims activity: If claims jump 25%+ above your historical average, investigate root causes and adjust accruals upward

- Significant increase in job volume or warranty terms: If you double revenue or extend standard warranties from one to two years, your reserve target doubles

Adjusting Accrual Rates Based on Claims Experience

SMACNA recommends an annual adjustment process:

- If your reserve balance is negative or depleted at year-end, add 1 percentage point to your accrual rate

- If your reserve is growing consistently, you may reduce to 1% the following year

This creates a self-correcting mechanism tied to actual experience.

External Factors That Affect Reserve Needs

Three cost pressures directly drive your reserve requirements up over time:

| Factor | What Happened | Reserve Impact |

|---|---|---|

| Labor cost inflation | BLS data shows median HVAC technician wages rose from $48,730 (2019) to $59,810 (2024) — a 22.7% increase | Warranty repair costs rise proportionally with your labor rates |

| Material cost inflation | CBRE forecasted 14.1% year-over-year construction cost increases in 2022, driven by supply chain disruptions | Higher parts costs mean a fixed reserve buys less coverage than it used to |

| Extended warranty terms | Stretching standard labor warranties from one to two years to stay competitive | Doubles your exposure on every new job signed under the new terms |

Apply each of these changes to your reserve calculation at year-end — not just when a claim arrives.

Record-Keeping for Claims

Log every warranty claim with:

- Job ID and original completion date

- Nature of defect (equipment failure, installation error, material defect)

- Cost breakdown: labor hours, parts, fuel, administrative overhead

- Root cause category: technician error, product defect, subcontractor issue, customer misuse

This data allows accurate accrual rate refinement over time and protects you in disputes. It also helps identify systemic issues. If 80% of callbacks trace back to one product line or one install crew, the log tells you exactly where to intervene — before the next claim hits.

Common Mistakes Contractors Make With Warranty Reserves

Underfunding or Not Separating the Reserve

The most damaging error: treating warranty costs as operational expenses paid from general cash flow rather than from a dedicated reserve. This creates two problems:

- Cash flow crises: When multiple claims hit simultaneously (say, three callbacks in one week), operating cash drains fast. Without a reserve, you're scrambling to cover payroll and parts orders while honoring warranty obligations.

- Hidden profitability issues: If warranty costs flow through general expenses, you can't see the true net margin on warranted work. A job that appeared to net 8% may have actually returned 3% after warranty costs—but you won't know until it's too late.

Setting a One-Size-Fits-All Accrual Rate

Applying a flat percentage (e.g., 2% of revenue) across all job types leads to systemic problems:

- Under-reserving on high-risk jobs: A new geothermal installation with a five-year warranty carries far more risk than a standard furnace replacement with a one-year warranty. The same 2% accrual rate leaves the geothermal job significantly under-reserved.

- Over-reserving on low-risk jobs: Simple service repairs with 90-day warranties don't need the same accrual rate as complex installations. Over-reserving ties up cash unnecessarily.

Solution: Use job-specific and trade-specific accrual rates based on warranty term length, job complexity, and historical claims data for that work type.

Failing to Account for Long-Term Warranty Tail Risk

Job-specific accrual rates also need to account for when claims arrive — not just how many. Contractors offering multi-year labor warranties often underestimate that the bulk of claims tend to cluster in months 12-24, not immediately after installation.

Legal exposure compounds this. Even a one-year written warranty doesn't cap your liability:

- Standard callbacks are defined as within 30 days (service) or one year (installation)

- Statutes of limitation run 3-10 years from discovery of the defect

- Statutes of repose run 6-12 years from substantial completion

- Implied warranties of workmanship extend beyond any written warranty term

Action step: Track claims by age of original job. If your data shows claims clustering in months 12-18, adjust your reserve calculation to account for this delayed exposure rather than assuming claims occur evenly across the warranty period.

Beyond the Reserve Fund: The Reinsurance Alternative

What Is Contractor-Owned Reinsurance?

Instead of simply holding a reserve fund in a bank account, home service contractors can establish their own warranty company through an administrator obligor reinsurance structure. Rather than paying third-party warranty providers who keep the underwriting profits, you collect warranty premiums from customers, fund claims from your own reserve, and retain 100% of the underwriting profit when claims run below premiums collected.

WarrantyRE helps home service contractors — HVAC, roofing, plumbing, and electrical — set up and manage this exact structure. Founded in 1994, the company has helped over 400 clients establish reinsurance programs, drawing on 30+ years of experience originally built in the automotive dealer market.

The Key Difference: Cost Center vs. Profit Center

Traditional reserve fund:

- Money set aside from operating revenue

- Held in a bank account earning minimal interest

- Spent on claims as they arise

- Unused funds remain general business assets with no tax advantage

- No underwriting profit captured

Reinsurance structure:

- Warranty fees collected from customers (not from operating revenue)

- Held in a trust account invested in conservative government bonds

- Claims paid from the customer-funded pool

- Unused reserves remain in your reinsurance company, generating underwriting profit and investment income

- Tax-advantaged under IRS Code 831(b), reducing what flows to the IRS each year

- Backed by A-rated insurers for catastrophic claim protection

- Full administration handled by WarrantyRE (claims adjudication, compliance, bookkeeping)

Who Benefits Most?

Contractors with predictable, lower-than-average claim rates benefit most. If your historical data shows claims running consistently at 1.5–2% while you're offering warranty coverage priced at 3–4% of job revenue, you're essentially subsidizing third-party warranty companies. A reinsurance structure captures that spread as profit for your business instead.

Contractors running significant volume can also use the tax-advantaged structure to redirect money that would otherwise go to the IRS directly into their own reinsurance entity — keeping it working for the business rather than disappearing into overhead.

Frequently Asked Questions

How much should a reserve fund be?

The right amount depends on your active warranty exposure, historical claim rate, and warranty term length. A general starting target is 12-24 months' worth of average monthly claims, funded by accruing 1-5% of job revenue depending on trade type. HVAC contractors following SMACNA guidance start at 2% of equipment cost; other trades should start at 2-3% and adjust annually based on actual claim history.

How to calculate a warranty reserve?

Multiply your historical claim rate by total revenue currently under active warranty coverage. If you've paid $12,000 in warranty costs on $400,000 of covered jobs, your claim rate is 3% and your reserve target is $12,000. Adjust upward for longer warranty terms or higher-risk job types.

How does a warranty reserve work?

A warranty reserve is funded by setting aside a small percentage of each job's revenue into a dedicated account at the time of sale. When a valid warranty claim arises, the repair cost is paid from that account rather than from operating cash flow, protecting profitability and preventing cash flow crises when multiple claims hit simultaneously.

What is the difference between warranty accrual and warranty reserve?

The accrual is the ongoing action—the percentage of revenue transferred into the reserve at each job completion (e.g., 2% of every HVAC installation). The reserve is the accumulated balance held in the dedicated account to pay future claims. The accrual builds the reserve; the reserve absorbs claims.

What is a typical contractor warranty?

Most home service contractors offer a 1-year labor warranty as standard, with some trades (HVAC, roofing) offering 2-5 year warranties or extended service agreements. Manufacturer equipment warranties are separate—typically 5 years, or 10 years if registered within 60 days—and typically pass through to the customer. Metal roofing workmanship warranties run 5-10 years from installers.

What are the three types of warranties?

Express warranties are written promises defining specific coverage terms and duration, negotiated at the time of sale. Implied warranties are legally assumed workmanship standards that apply automatically — courts generally favor the consumer. Extended warranties (service contracts) provide coverage beyond standard terms and, when structured through a reinsurance program, allow contractors to capture the underwriting profits themselves rather than paying a third-party provider.

Building a warranty reserve fund converts unpredictable warranty obligations into a quantified, manageable liability. For contractors ready to go further, a reinsurance structure takes that same liability and turns it into a profit center — one funded by your own customer base.