Introduction

Home service contractors — HVAC technicians, roofers, plumbers, electricians — hand over a slice of their revenue every time they sell a warranty. The U.S. extended warranties and service contracts market reached $6.76 billion in 2025 and is projected to grow to $12.95 billion by 2033 — and most of that underwriting profit flows to third-party providers, not the contractors doing the work.

Most contractors struggle to see this clearly: the premiums their customers pay go out the door, the third-party provider handles claims, and whatever is left over — the underwriting profit — stays with the provider. That margin doesn't have to belong to someone else.

This article is a practical guide for contractors who want to understand how to set up their own warranty company — specifically the administrator-obligor reinsurance model — and keep that underwriting margin inside their own business.

TL;DR

- Starting your own warranty company means becoming the administrator-obligor that collects premiums, manages claims, and keeps the underwriting profit after claims are paid

- The admin-obligor reinsurance model, backed by an A-rated insurer, delivers the highest profit capture

- Setup covers business formation, compliance, product design, and claims administration — all handled with the right reinsurance partner by your side

- Financial upside includes capturing 100% of underwriting profits, investing premium reserves for ROI, and reducing service callback costs

- Pricing, loss ratio management, and customer experience determine long-term profitability

What Is a Contractor-Owned Warranty Company?

A contractor-owned warranty company means you form a separate entity that acts as the administrator and obligor — responsible for collecting premiums, adjudicating claims, and retaining the profits left after claims are paid. Rather than referring customers to a third-party warranty provider, you own the entire structure.

Understanding the Warranty Ecosystem Roles

To understand where you fit, here are the four key roles in the warranty ecosystem:

- Seller — the contractor offering the warranty to customers

- Administrator — the entity managing claims, compliance, and operations

- Obligor — the entity legally responsible for paying claims

- Reinsurer — the A-rated insurance carrier providing the financial guarantee

In the contractor-owned model, you occupy the administrator-obligor role while being backed by an A-rated insurance carrier that provides the financial guarantee behind the contract. That combination gives your warranty program both legal standing and financial backing.

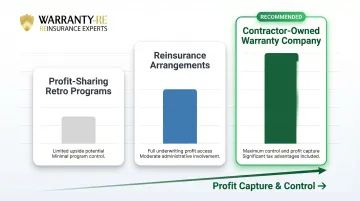

Three Participation Structures Compared

Contractors can consider three main participation structures:

- Profit-sharing/retro programs — limited upside, minimal control over pricing or claims

- Reinsurance arrangements — full underwriting profit, more involvement in program structure

- Dealer/contractor-owned warranty company — maximum control, full profit capture, on-shore structure with tax advantages

The rest of this guide walks through what it takes to set up and run that third option — the admin-obligor model.

Why Home Service Contractors Are Starting Their Own Warranty Companies

Capturing the Profit You're Already Generating

Every dollar a third-party warranty company retains after paying claims is a dollar you generated but never received. The total U.S. service contract industry generated $49 billion in revenue in 2019, with projections reaching $59 billion by 2028. Home warranties specifically represent over $4 billion annually.

When you send warranty premiums to a third-party provider, you're funding their underwriting profits. Major warranty providers like Frontdoor report 55% gross profit margins and 26.4% adjusted EBITDA margins — profits built on premium reserves that contractors generate.

Business Benefits Beyond Pure Profit

Beyond underwriting profit, contractor-owned warranty companies deliver several strategic advantages:

- Controls the claims experience — you set resolution speed, service quality, and customer treatment

- Captures reserve investment income from the gap between premiums collected upfront and claims paid over time, which can be invested in conservative bonds for additional ROI

- Creates tax planning advantages through IRS Code 831(b): reinsurance companies with under $2.9 million in annual net premiums can elect to be taxed only on investment income

- Converts one-time installs into ongoing warranty relationships, shifting your revenue model from transactional to recurring

Proven Model Now Expanding to Home Services

These benefits aren't theoretical — automotive dealers have validated this model since the late 1970s, with significant growth through the 1990s and 2000s. F&I (Finance and Insurance) is described as the most profitable department at the dealership, and reinsurance is characterized as an underappreciated opportunity for wealth creation.

Home service contractors — HVAC, roofing, plumbing, and electrical — are now adopting the same structure, driven by tightening margins and the recognition that warranty revenue has been flowing to third parties for too long.

What to Know Before You Start

Set Realistic Expectations on Involvement

Owning a warranty company is not passive income from day one. Early stages require attention to pricing, compliance, and claims management. A full-service reinsurance program administrator handles claims adjudication, compliance, training, and financial reporting — which keeps your administrative burden manageable from the start.

You'll need to focus on integrating warranty fees into your pricing, training your sales team to present warranties confidently, and monitoring financial performance. Legal filings, tax returns, claims administration, and regulatory compliance are all handled by your program administrator.

Understand the Regulatory Landscape

Service contracts (extended warranties) are regulated differently than insurance in most states, but the rules vary. More than 30 states have adopted elements of the NAIC Service Contracts Model Act, which explicitly states that service contracts are not insurance.

Key compliance requirements include:

- Backing by a licensed A-rated insurer or maintaining a reserve fund

- Registration with state insurance departments (in some states like Washington and New Hampshire)

- Proper disclosures to customers

- Recordkeeping and reporting obligations

A full-service program administrator manages these requirements on your behalf. The obligations are real and non-negotiable — but they don't have to fall on you.

Confirm You Have Critical Mass

Before launching your own warranty company, your job volume needs to support the economics. "Critical mass" is the point where premium inflows consistently cover claims and administrative costs — with underwriting profit left over.

Key indicators you're ready:

- You're completing at least 50-100 warranty-eligible jobs annually

- Average job ticket size is $3,000 or higher

- You're already offering labor warranties to win jobs and remain competitive

- You're absorbing callback costs out-of-pocket or paying third-party warranty providers

The right reinsurance partner will conduct a business analysis to determine whether your current volume supports the program. Don't assume you're too small — many contractors underestimate their eligibility.

How to Start Your Own Warranty Company as a Contractor – Step by Step

This section breaks the process into six execution stages designed specifically for home service contractors. Avoid the most common mistakes: treating the warranty company as an afterthought, underpricing contracts to win jobs, and skipping claims process design before launch.

Step 1 – Define the Warranty Opportunity Within Your Business

Audit your current warranty exposure:

Start by answering these baseline questions:

- How many jobs per year carry a warranty obligation?

- What's the average ticket size for warranty-eligible work?

- How much of your current warranty cost is absorbed by callbacks and rework versus paid to a third-party provider?

This baseline determines whether the economics support your own program. Pull your last 12 months of installations and track three numbers: hours spent on warranty callbacks, the labor and materials cost of those callbacks, and revenue lost by pulling crews off paying work.

Identify the best warranty candidates:

Not all services are equally suited for formal warranty products. The strongest candidates are:

- Higher-ticket installations — HVAC systems, roofing, electrical panels, whole-home repiping

- Clear customer appetite for extended coverage — customers understand the value and are willing to pay

- Meaningful premium pricing — warranty fees can be priced at 3-8% of job cost without resistance

For example, a $12,000 HVAC system replacement can support a $360-$960 warranty fee built into the proposal. A $200 service call typically cannot.

Step 2 – Choose the Right Warranty Company Structure

Administrator-obligor vs. profit-sharing programs:

Profit-sharing arrangements offer limited upside — typically 10-30% of underwriting profit after the third-party provider takes their share. You have no control over pricing, claims outcomes, or product design.

The admin-obligor structure gives you:

- 100% of underwriting profits — no sharing with a third party

- Full control over product design — you set coverage terms, pricing, and customer experience

- Claims outcome control — you determine what's covered and how fast claims are resolved

- A long-term financial asset — your reinsurance company builds value alongside your contracting business

The role of the A-rated insurer:

In the admin-obligor model, an A-rated insurance carrier backs your contracts as the ultimate financial guarantee. This insurer provides the underwriting support and regulatory credibility required to operate legally.

You sit as the administrator-obligor — collecting premiums, managing claims, and capturing 100% of the underwriting profit. The insurer stands behind your program; you own the entity outright.

Step 3 – Handle Legal Formation and Regulatory Compliance

Entity formation requirements:

Your warranty company is a separate legal entity — typically a corporation or LLC — formed specifically to act as the administrator-obligor. This keeps the warranty business legally distinct from your contracting business, protecting both from crossover liability.

Formation steps include:

- Choosing a jurisdiction (onshore U.S. or offshore options like Turks and Caicos)

- Filing articles of incorporation or organization

- Obtaining an EIN from the IRS

- Establishing corporate governance documents

State-by-state compliance requirements:

Most states regulate service contracts through the Department of Insurance or a similar agency. 42 states fall into "Quadrant I" with local oversight and insurance industry influence, including California, Texas, Florida, New York, and others.

Common compliance requirements include:

- Registration with the state insurance department

- Backing by an A-rated licensed insurer (most common approach)

- Maintaining minimum reserve funds (alternative to insurance backing in some states)

- Filing disclosures and contract forms for approval

Working with an experienced reinsurance program administrator cuts the compliance burden considerably. WarrantyRE has managed all legal forms, filings, tax returns, and renewals for contractors and dealers since 1994 — so you're not building that infrastructure from scratch.

Step 4 – Design Your Warranty Products and Pricing

Types of warranty products contractors offer:

Labor-only warranties cover your workmanship — repairs or corrections needed because of installation errors or defects in the contractor's work. These are the most common and carry the lowest risk since equipment failures are covered by manufacturers.

Parts-and-labor warranties cover both your labor and the installed equipment, extending beyond the manufacturer's warranty. These carry higher risk since you're covering equipment failure in addition to workmanship.

Extended service agreements (ESAs) cover the installed equipment beyond the manufacturer's warranty period, typically for 5-10 years. These are most common for HVAC systems and major mechanical equipment.

Each type has a different risk profile and premium structure. Labor-only warranties are easiest to start with and deliver the best profit margins.

How to price warranty products correctly:

Premiums must account for:

- Expected claims frequency — how often claims occur based on equipment type, age, and installation complexity

- Expected claims severity — average cost per claim (labor, materials, dispatch)

- Administrative costs — claims management, compliance, reporting (typically 20-25% of premium)

- Underwriting profit margin — the profit you intend to capture (target 10-20% of premium)

Pricing formula:

Premium = (Expected Claims Cost + Administrative Cost) / (1 - Target Profit Margin)

Example: If expected claims cost is $200, administrative cost is $50, and you target a 15% profit margin:

Premium = ($200 + $50) / (1 - 0.15) = $250 / 0.85 = $294

Industry benchmarks show loss ratios around 45-65% for well-managed service contract programs. This means 45-65% of premium goes to claims, leaving 35-55% for administration and profit.

Underpricing is the most common mistake contractors make when launching a warranty program. Dropping your fee to close a deal compresses the profit that makes the program worthwhile — and creates a claims deficit down the road. If you're building a 2-year labor warranty into a $10,000 HVAC installation, a $300-$500 fee is reasonable and expected. Don't default to $150 just to close the deal.

Step 5 – Build Your Claims Administration and Customer Experience Process

Define the claims flow from the customer's perspective:

A clear, fast claims process turns a warranty product into a customer loyalty tool rather than a source of complaints. Design your process around these touchpoints:

- Customer calls with a claim — they call a dedicated warranty claims line (managed by your administrator)

- Claim is evaluated and authorized — the administrator verifies coverage, determines if the claim is valid, and authorizes the repair

- Repair is scheduled — the contractor dispatches a technician or coordinates with their service team

- Payment is processed — the claim is paid from warranty reserves, and documentation is recorded

Operational infrastructure needed:

- Claims adjudication protocols — rules for what's covered, how claims are verified, and who approves repairs

- Contractor dispatch or vendor network — most contractors use their own technicians; larger programs add vendor networks for out-of-area coverage

- Documentation per claim — service report, photos, parts receipts, and proof of covered failure to guard against fraud and support loss ratio tracking

- Monthly financial reporting — claims paid, reserve balance, and loss ratio tell you whether your pricing is working and when to adjust

For most contractors starting out, a third-party program administrator handles these functions rather than your in-house team. That eliminates the need to hire claims staff, build software systems, or manage compliance reporting from day one.

Step 6 – Launch, Track, and Scale the Program

How to present warranties to customers during the sales process:

Don't present warranties as an upsell or add-on. Present them as a built-in part of your service offering that demonstrates confidence in your workmanship and protects the customer's investment.

Effective sales language:

"Every installation we complete includes a 2-year labor warranty covering our workmanship and installation. If anything goes wrong because of how we installed it, we'll fix it at no charge. This warranty is built into your proposal and gives you complete peace of mind."

This frames the warranty as standard, professional, and value-added — not optional or extra. ACCA industry benchmarks show service technicians should aim for a minimum 25% conversion rate from service calls to service agreements, with specialized technicians achieving 70% or higher.

Offering a warranty product increases customer confidence, reduces price objections, and differentiates you from competitors who don't stand behind their work.

Establish key performance indicators to monitor:

| KPI | What to Track | Target |

|---|---|---|

| Premium volume | Total warranty fees collected monthly and annually | Growing quarter-over-quarter |

| Claims loss ratio | Claims paid ÷ earned premiums | 45–65% |

| Reserve balance | Unearned premiums held to cover future claims | Grows with premium volume |

| Investment income | Returns on reserve funds in bonds or conservative vehicles | Additional ROI beyond underwriting profit |

| Net underwriting profit | Premiums minus claims minus administrative costs | 10–20% of premium |

If your loss ratio exceeds 70%, your pricing is too low or your claims are running too frequently — either way, it's time to adjust.

These metrics tell you whether the program is financially healthy and whether it's time to expand coverage offerings or adjust pricing.

Conclusion

Starting your own warranty company as a contractor turns a recurring cost into a revenue stream you own. The steps are sequential and manageable — especially when a program administrator like WarrantyRE handles legal formation, compliance, claims administration, and financial reporting on your behalf.

Contractors who set this up correctly build a separate financial asset — one that grows alongside the contracting business, deepens customer loyalty, and creates a real competitive edge in their market.

You're already offering warranties to win jobs. The next step is making sure those warranties generate profit for you, not a third-party provider you'll never meet.

Frequently Asked Questions

Do you need a license to sell a warranty?

Selling service contracts is distinct from selling insurance in most states, but it is still regulated. Typically, the obligor must be backed by a licensed insurer or meet state reserve requirements. A program administrator typically handles these compliance requirements, so contractors don't need to obtain individual licenses.

How long should a contractor's warranty be?

Contractor warranty lengths vary by trade. Labor warranties commonly range from 1 to 2 years, while extended service agreements on installed equipment (HVAC systems, roofing) can run 5 to 10 years. The right term depends on the risk profile of the work and the premium structure that supports it.

How do home warranty companies make money?

Warranty companies profit from the difference between premiums collected and claims paid (underwriting profit), plus investment income earned on reserves held before claims are paid out. Contractors who own their warranty company capture this margin directly instead of handing it to a third-party provider.

Are warranty companies profitable?

Yes, warranty and service contract businesses can be highly profitable when priced correctly and managed well. Frontdoor reported 55% gross profit margins and 26.4% adjusted EBITDA margins in 2025. Large third-party warranty providers have operated profitably for decades using the same premium reserves that contractors currently fund. The contractor-owned model captures that margin as business income rather than revenue paid out to a third party.

What is the difference between owning your own warranty company and using a third-party warranty provider?

With a third-party provider, the contractor sells the warranty, the customer pays the premium, and the provider keeps the underwriting profit. With a contractor-owned model (administrator-obligor structure), the contractor's entity collects the premium, manages claims, and retains that profit — converting what was a cost center into a recurring revenue stream.