The result: pricing an extended warranty program without understanding the full cost structure is increasingly expensive. Price too low and claims eat into margin. Price too high and customers walk. Get the coverage terms wrong and disputes follow.

This guide breaks down what HVAC extended warranties actually cost, what drives those costs, and how contractors can price programs that are both competitive and profitable.

TL;DR

- Labor warranties for HVAC equipment typically range from $115–$220 for 2-year coverage to $500–$940 for 10-year coverage on a central AC unit alone

- Four factors drive pricing most: years of coverage, local labor rates, coverage provider type, and contractor markup

- Underpricing cuts margin; ignoring claims exposure creates financial risk you may not see until it's too late

- Profitable warranty programs require understanding the full cost structure, not just the upfront premium

How Much Does an Extended Warranty Cost?

Extended warranties don't have a fixed price. Costs shift based on equipment type, coverage term, local labor market, and the structure behind the program. When contractors don't account for these variables, the outcomes are predictable: underpricing leads to unrecovered claim costs, overpricing drives customers to competitors, and vague coverage terms generate disputes at the worst possible moment.

Typical Price Ranges by Coverage Term

The most detailed publicly available pricing benchmark comes from Trinity Warranty's published rate data for HVAC labor warranties. These figures reflect provider-published ranges, not independently verified industry averages, but they offer a practical starting point for contractors building their own pricing:

| Equipment | 2-Year | 3-Year | 5-Year | 10-Year |

|---|---|---|---|---|

| Central AC (labor only) | $115–$220 | $170–$300 | $285–$500 | $500–$940 |

| Furnace (labor only) | $135–$240 | — | — | — |

| Complete heat pump system | — | — | — | $850–$1,600 |

Source: Trinity Warranty published pricing

Most major manufacturers — Carrier, Trane, Lennox, Goodman, and Daikin — cover parts for up to 10 years when equipment is registered within 60–90 days of installation. That means contractor-sold extended warranties are filling the labor gap, not replacing parts coverage. Customers are paying for technician time, not components.

Coverage Tier Comparison

Not all extended warranties deliver the same thing. Three general tiers exist in the market:

- Basic (labor only): Covers technician labor after the manufacturer's one-year labor period ends. Lower cost, but higher risk of disputes when customers expect coverage that isn't included.

- Mid-range (labor plus): Adds trip charges and diagnostic fees. Broader protection reduces friction when claims are filed.

- Premium (comprehensive): Covers labor, trip charges, diagnostic time, and sometimes refrigerant. ACHR News reimbursement examples showed tiers at $75, $100, and $125 per claim, with higher tiers including one-hour trip and diagnostic coverage.

Choosing a tier isn't just a pricing decision — it's a customer retention decision. A plan that declines a repair the customer expected to be covered creates more damage than the cost of upgrading the coverage in the first place.

Key Factors That Affect Extended Warranty Pricing

No single variable determines the right price. Four factors interact, and getting any one of them wrong throws off the entire program.

Years of Coverage

Longer terms cost more — roughly proportionally for labor-based plans. Trinity's published AC-only data illustrates this:

- 2-year plan: $115–$220

- 5-year plan: $285–$500

- 10-year plan: $500–$940

That's approximately a 4x increase from the shortest to longest term available. Longer plans also carry more uncertainty about future labor costs, which is why reserve-based programs need conservative funding assumptions built in from the start.

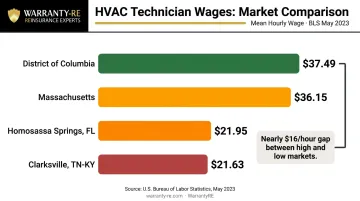

Local Labor Rates

Local labor rates expose a flaw in most generic pricing guidance. BLS May 2023 occupational wage data shows a dramatic spread across U.S. markets:

| Market | Mean Hourly Wage |

|---|---|

| District of Columbia | $37.49 |

| Massachusetts | $36.15 |

| Clarksville, TN-KY | $21.63 |

| Homosassa Springs, FL | $21.95 |

That's nearly a $16/hour gap between high-wage and low-wage markets. A warranty reimbursement rate set at the national median will systematically underpay claims in DC or Boston and leave margin sitting unused in Tennessee. Pricing must reflect the market where the work is actually performed.

Coverage Provider Type

Four main provider structures exist, each with different implications for cost and risk:

- Manufacturer programs (Carrier, Lennox, Rheem): Labor coverage is optional and often limited — Lennox's Warranty Your Way covers up to 3 years of labor; Carrier's Consumer Choice requires dealer participation. Reimbursement schedules may not match contractor labor rates.

- Insurance-backed plans: Contractor selects reimbursement rate, term, and covered components. ACHR News recommends verifying providers are backed by AM Best A-rated carriers.

- Third-party administrators (TPAs): Offer plan flexibility across brands and equipment types. JB Warranties, for example, offers labor-only, labor plus, and parts-and-labor options. TPAs capture the underwriting profit — that's the cost of simplicity.

- Contractor-owned reinsurance: The contractor establishes their own reinsurance entity. They collect premiums, retain underwriting profits, and carry the risk — with proper structure and backing. More on this below.

Contractor Markup Strategy

Regardless of the coverage source, contractors decide how to price to customers. Three common approaches:

- Bundle into the install price — Higher conversion, lower transparency. Customer doesn't see the warranty as a line item.

- Tiered add-on at time of sale — Fully visible to the customer. Giving buyers a 3/5/10-year choice increases perceived value and average ticket.

- Post-sale outreach — Lower conversion but captures customers who passed initially. Often sold at a slight premium.

Each approach carries different margin implications. Bundling compresses margin visibility; tiered add-ons create upsell opportunity. Contractors running higher average ticket jobs ($8,000+) typically see the strongest results from tiered add-ons — the dollar amount is visible but doesn't feel disproportionate relative to the install price.

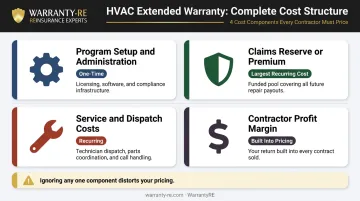

The Full Cost Breakdown

The upfront premium is not the total cost. Every warranty program has four distinct cost components — and ignoring any one of them will distort your pricing from the start:

| Cost Component | Type | Notes |

|---|---|---|

| Program setup and administration | One-time | Enrollment, documentation, company formation if applicable |

| Claims reserve or premium | Recurring | The largest cost; either TPA premiums or funded reserves |

| Service and dispatch costs | Recurring | Labor, trip charges, diagnostic time per warranty call |

| Contractor profit margin | Built into pricing | Should be priced deliberately, not calculated as "whatever's left" |

The claims reserve is the component most commonly underestimated. Consider a straightforward example:

- Warranty sold for: $300

- Two service calls at $250 each: $500 in claims

- Net result: -$200 per warranty sold

That loss is entirely preventable — but only if you model claims frequency and labor cost before setting your price, not after.

How Contractors Price Extended Warranties for Customers

Effective pricing starts with knowing the base cost from the coverage provider, then layering in a target margin. Pricing without knowing claims frequency and severity for the equipment being covered is the most common reason programs underperform.

The three most common contractor pricing approaches each come with tradeoffs:

- Bundle into install price: Warranty is invisible to the customer, conversion is high, but the margin contribution is harder to track

- Tiered add-on at sale: Transparent, gives customers a choice, and often increases average ticket — customers who select a 10-year plan spend more and tend to stay loyal longer

- Post-sale outreach: Lower close rate but useful for recapturing customers who declined at install

Contractor-Owned Reinsurance as a Structural Alternative

There's a fourth option that changes the economics entirely: establishing a contractor-owned reinsurance company.

With this model, contractors collect warranty premiums from customers, and those funds flow into a reinsurance structure the contractor legally owns, held in a U.S. Trust Company custodial account. Claims are paid from that pool. Unused funds stay with the contractor — not a third-party administrator.

WarrantyRE has worked with contractors and dealers since 1994 to set up these administrator obligor structures. The contractor's reinsurance company is backed by A-rated insurers, so if the reinsurance company can't meet obligations, the underwriting carrier covers the gap.

WarrantyRE handles the full administrative load so contractors stay focused on installs:

- Claims adjudication

- Compliance filings and legal forms

- Tax returns and financial bookkeeping

- Performance reporting and program analysis

One common misconception: this structure isn't just for large contractors. WarrantyRE works with contractors across a range of install volumes.

Common Mistakes When Estimating Extended Warranty Costs

Three mistakes show up repeatedly when contractors price warranty programs without a full picture:

- Upfront premium tunnel vision — ignoring claims exposure and service delivery costs. A plan that's cheap to sell can be expensive to fulfill, particularly in high-wage labor markets.

- Copying competitor pricing without accounting for local labor costs or equipment type. A rate that works in rural Tennessee may produce losses in suburban Boston.

- Chasing the lowest-cost provider without vetting reimbursement rates, claim reliability, or financial stability. If a provider exits the market, the contractor's reputation absorbs the damage — not the provider's.

Frequently Asked Questions

How do you calculate warranty costs?

Start with the base premium or reserve amount from your coverage provider, then adjust for local labor rates and years of coverage. Add service delivery costs and contractor margin. The formula: provider cost + service delivery costs + contractor margin = customer price.

What is a warranty labor rate?

It's the hourly or per-visit amount a coverage provider reimburses a technician for covered repair work. If that rate is lower than your actual labor cost, you lose money on every warranty service call — making reimbursement rate alignment a critical factor when selecting a provider.

What is the average cost of an HVAC extended warranty?

Based on published provider data, a 2-year labor warranty on a central AC unit typically runs $115–$220, while a 10-year plan on a complete heat pump system can reach $850–$1,600. Actual figures shift based on equipment type, coverage length, and your local labor market.

How does coverage length affect extended warranty cost?

Longer terms increase total cost roughly proportionally, since more years of potential claims must be funded. A 10-year plan costs approximately 4x a 2-year plan for the same equipment. On a per-year basis, longer plans typically deliver better value for the customer.

Is it better to buy a third-party warranty or own your own warranty program?

Buying from a TPA is simpler to start but passes all underwriting profits to the provider. Owning a reinsurance program keeps those profits inside your business. The tradeoff is setup complexity and compliance requirements — which is where a reinsurance program administrator handles structure, filings, and compliance on your behalf.

What factors most affect extended warranty pricing for HVAC contractors?

The four primary factors: years of coverage, local labor rates, coverage provider structure, and contractor markup. Geographic labor rates typically drive the most variation in both upfront pricing and actual claims costs.