Introduction

Most HVAC contractors view labor warranties as an unavoidable cost—a promise that costs money when things go wrong. Every callback, every warranty repair, every time you roll a truck to fix a refrigerant leak or a bad contactor you installed, that's your technician's time, fuel, parts, and margin walking out the door. According to the 2024 ACCA Financial Benchmarking Study, the median HVAC contractor operates at just 5.8% net profit margin, leaving almost no room for error. Unpriced warranty callbacks can be the difference between profit and loss.

The warranty itself isn't the problem. When labor warranties are treated as cost centers rather than revenue opportunities, every system you install becomes a liability sitting on your books until the coverage expires.

Contractors who restructure their warranty programs generate markup revenue, build predictable income, and reduce financial exposure. Those ready to go further can capture underwriting profits directly through reinsurance ownership — turning what drains margin into something that builds it.

TLDR

- Labor warranties are a hidden liability because they're unpriced, unfunded, or outsourced to third parties who keep the profits

- Pricing warranties consistently and selling them on every job adds direct per-job revenue without added headcount or inventory

- The most profitable contractors don't just sell warranties—they own the warranty company, capturing 100% of underwriting profits

- An administrator obligor reinsurance structure converts warranty liability into a funded asset—with investment returns and tax advantages built in

- Making that shift requires three things: repricing warranties, tightening the sales process, and restructuring how warranty income is held

Why Most HVAC Contractors Treat Warranties as a Loss Leader

The Default Mindset Problem

Most HVAC contractors include a one-year labor guarantee with every installation at no additional charge. This is positioned as a customer service gesture rather than a revenue line, creating uncapped, unfunded liability. When manufacturers like Carrier, Trane, and Lennox provide 5-10 year parts warranties, they cover components only—the moment your technician puts hands on the system, all labor costs fall on you.

Manufacturer warranties explicitly exclude labor, refrigerant, brazing materials, rigging, freight, and administrative costs. According to ACHR News, manufacturers pay a "ridiculously low amount" for warranty labor and charge processing fees of $50-$75 per claim. One bad callback season can wipe out margins on multiple jobs when these costs come directly from your pocket.

The Structural Problem: Self-Insurance Without Reserves

When contractors "self-insure" without a funded reserve or priced warranty product, they carry unknown liabilities that creditors and potential buyers see as red flags. A DOE/AHRI field study found that more than 65% of residential HVAC systems are improperly installed and performing suboptimally. Even quality-focused contractors absorb risk from weather extremes, customer misuse, and unforeseen failures.

Those installation issues translate directly into callbacks — and callbacks cost you. With average HVAC job values ranging from $2,800 to $5,500, unpriced warranties on 100 annual installs represent potentially $280,000-$550,000 in exposure with zero revenue offset. That liability compounds every year you add jobs without pricing the risk.

The Better Framework: Priced Warranty Products

Every HVAC install is an opportunity to sell a priced, documented labor warranty. When customers pay for coverage upfront, the liability shifts from an open-ended internal cost to a funded product with defined terms. That's the difference between absorbing callbacks and building a warranty program that pays for itself.

The Real Profit Opportunity Hidden in Labor Warranties

Revenue Mechanics: Turning Liability Into Income

When you charge customers a warranty premium (built into the install quote), a portion covers expected claim costs and the remainder is direct margin. The global extended warranty market reached $159.38 billion in 2025, growing at 8.6% annually—proof that consumers actively seek protection products.

Warranty pricing context:

- Average HVAC job value: $2,800-$5,500

- Typical warranty pricing: 8-10% of system cost

- Per-job revenue uplift: $400-$800

Warranty Week's analysis of 236 service contracts found appliance warranties average 8.7-10.5% of product price for 3-year terms. Applied to HVAC, a warranty priced at 8-10% of a $6,000 system represents $480-$600 in additional revenue per job.

Warranty Markup vs. Underwriting Profit

Critical distinction: When you sell through a third-party warranty provider, you earn the markup (commission) but the provider keeps the underwriting profit—the spread between premiums collected and claims paid.

How it breaks down:

- Warranty markup: 10-20% commission you receive when selling third-party warranties

- Underwriting profit: 20-40% of premiums that remain after all claims and administrative costs—currently going to the warranty company

In dealer-owned reinsurance structures, underwriting profit typically ranges from 20% to 40% of total premiums collected, with target loss ratios of 40-60%. Over hundreds of installs, this represents significant money leaving your pocket.

The Claims Reserve Float

When warranty premiums are collected and claims are statistically predictable, the funded reserve generates a float—money held before claims are paid. Contractors who own their warranty structure earn investment returns on this float.

Labor cost context: BLS data from May 2023 shows median HVAC technician wages at $27.55/hour. A typical warranty call covers diagnostic time, travel, and repair labor—usually 1.5-3 hours, placing internal labor cost at $55-$120 per call before overhead.

A $500-$750 warranty premium covers multiple potential service calls—a favorable ratio for contractors with low callback rates.

The DOE/AHRI finding that 65%+ of systems have installation-related faults also matters here: contractors who install correctly experience substantially lower claim rates than the industry average, making the math even more attractive.

Two-Year Backdating Revenue Opportunity

Most warranty programs allow contractors to enroll installs up to 24 months after original start-up date. This means joining a warranty program today lets you immediately market extended coverage to your existing customer base and generate revenue from past jobs—creating instant cashflow from completed work.

Tax Planning Dimension

Owning a reinsurance structure creates legitimate tax planning opportunities, including the ability to build reserves treated differently than ordinary income. Money that would go to the IRS can instead remain in a tax-advantaged structure working for your business. Consult a qualified tax advisor to understand how this applies to your specific situation.

How Owning Your Own Warranty Company Changes Everything

The Administrator Obligor Reinsurance Model Explained

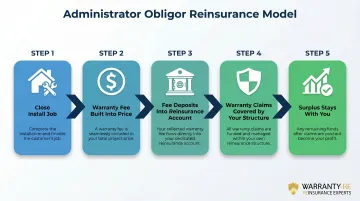

Instead of sending premiums to a third-party warranty company, you establish your own reinsurance entity (backed by an A-rated insurer) that collects and holds the premiums. When claims occur, your company pays them—when claims are lower than expected, you keep the surplus.

How it works in practice:

- You close a $12,000 system replacement with a 2-year labor warranty

- A warranty fee is built into the job price (the homeowner pays for it)

- That fee goes into your reinsurance account—not to an outside company

- When warranty calls come in, they're covered by your structure

- Money not used for claims stays yours

The Contrast With Third-Party Programs

Standard third-party arrangement:

- Contractor earns 10-20% markup

- Warranty company earns 20-40% underwriting profit

- Warranty company controls claims process

- Warranty company builds customer relationship around their brand

Administrator obligor ownership:

- Contractor captures 100% of profits

- Contractor controls customer experience

- Contractor builds brand loyalty through consistent warranty service

- Contractor retains all investment income on reserves

Home warranty providers like Frontdoor Inc. reported 18% profit margins in Q3 2024, with contract renewals representing 66-69% of quarterly revenue. That recurring revenue and profit currently flows to third parties—ownership captures it internally.

What Setup Actually Involves

Setting up your reinsurance structure requires:

- Forming the reinsurance entity (corporate structure and registration)

- Establishing compliance and legal filings

- Setting up claims adjudication processes

- Ongoing administration and regulatory compliance

WarrantyRE provides full-service support across all these areas, drawing on over 30 years of experience helping contractors establish and manage their own reinsurance programs. Services include company formation, training, claims management from first call to final resolution, bookkeeping, monthly financial statements, and regulatory compliance. You focus on installations—WarrantyRE handles everything else.

Most contractors are surprised how straightforward qualification actually is.

Is This Only for Large Contractors?

A contractor with consistent install volume can make this model work, and funding builds over time. While automotive dealer reinsurance typically requires approximately 25 service contracts per month as a minimum threshold, HVAC contractors with 200-300+ annual installs can justify the structure. The key is sufficient premium volume to cover administrative costs and build meaningful reserves.

Important: Evaluate volume requirements through a consultation with a reinsurance advisor who can analyze your specific business financials and install history.

The Compounding Effect: Building a Financial Asset

As your reserve grows and claims history is established, your reinsurance company becomes a standalone financial asset—separate from the HVAC operation—that builds equity, supports business valuation, and can be passed down or sold. For many owners, the reinsurance entity eventually carries meaningful value on its own—separate from what the contracting business itself is worth.

Investment income earned on reserves belongs to your reinsurance company, generating compounding returns across multi-year warranty terms. Conservative government bond allocations produce steady baseline returns.

Once balance sheet cash exceeds 125% of unearned premiums, excess funds can be invested more aggressively—at ownership direction.

Pricing Labor Warranties to Build Margin Without Losing Deals

Embed Pricing, Don't Add On

Position warranty coverage as "included" in the install quote rather than presenting it as an optional line item after the fact. Bundled pricing removes the friction of a separate upsell conversation — and the numbers support it.

Appliance retailers hit 20% attachment rates on products over $500 and 23% on products over $1,500 after building structured warranty offers into the point-of-sale process. HVAC contractors with average job values of $2,800-$5,500 are well-positioned to reach comparable — or better — attachment rates.

Tiered Pricing Framework

Recommended structure:

- 1-year standard: Baked into the base price — no upsell needed, sets the expectation

- 5-year extended: Priced above projected callback costs to generate a clear margin buffer

- 10-year premium: Highest margin tier, with the added benefit of locking in a long-term customer relationship

Actual pricing should reference your own labor cost data and warranty program guidelines. A contractor carrying $35/hour fully burdened technician costs and averaging 2-3 callbacks per 100 installs can price all three tiers profitably — the key is knowing your numbers before you set the price.

Once the pricing structure is solid, the next hurdle is usually the same: convincing yourself (and your sales team) that customers will actually pay for it.

Addressing the "Customers Won't Pay for It" Objection

Customers who just wrote a $5,000-$15,000 check for a new system are primed for this conversation — not resistant to it. The extended warranty market is growing at 8.6% CAGR, which reflects real consumer demand for protection, not just upsell success stories.

Key insight: Warranty buyers show 17.5% higher satisfaction scores, repeat at 2x the rate of non-buyers, and are 2x as likely to refer. Done right, the warranty pays for itself twice: once in margin, again in the referrals and repeat calls that follow.

Converting Warranties Into Recurring Revenue and Customer Loyalty

The Retention Mechanic

A 10-year labor warranty that names you as the service provider locks in future maintenance calls, repair visits, and ultimately the replacement job—creating a 10-year pipeline of touchpoints that no competitor can displace. Every warranty service call is an opportunity to demonstrate quality, upsell maintenance plans, and position yourself for the next system replacement.

Average HVAC contractor referral rates are 18%, with top performers reaching 35%. Warranty holders who experience seamless service become active referral sources—a warranty claim handled quickly and professionally is often more powerful for reputation than the original install.

The Referral and Word-of-Mouth Effect

That referral advantage compounds when customers feel protected. Warranty buyers rate post-purchase experience an average of 9.4 out of 10, versus 8.0 for non-buyers—a 17.5% satisfaction gap. They return 30 days sooner for their next purchase and carry 2-3x higher customer lifetime value. In HVAC terms, warranty customers become your most reliable promoters.

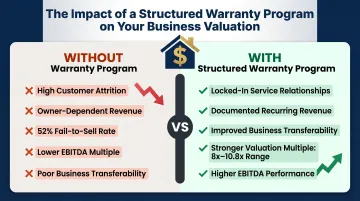

Business Valuation Impact

That loyalty also reshapes how buyers value your business. HVAC companies command average EBITDA multiples of 8x as of Q1 2025, with residential all-purpose firms in the $5-10M EBITDA range reaching 10.8x. Revenue durability is "the strongest determinant of valuation outcomes."

Approximately 52% of HVAC companies that go to market do not sell—most often because of high customer attrition or owner dependence. A structured warranty program directly counters both:

- Reduces attrition risk by locking in service relationships for the full warranty term

- Reduces owner dependence by creating documented, transferable recurring revenue

A contractor with a funded warranty book commands a stronger multiple when selling or transitioning the business. That makes the warranty program not just a revenue line—it's an equity-building strategy.

Frequently Asked Questions

What is a good profit margin for HVAC?

Industry average net profit margin is 5-10%, with the 2024 ACCA study placing median at 5.8% and top quartile at 13.2%. Contractors who price and structure labor warranties as a profit center can meaningfully improve margins beyond the industry average by capturing underwriting profits and investment returns.

Can I make $200K doing HVAC?

Yes, high earning potential exists for HVAC business owners. Owner compensation scales with revenue: $80K-$140K at $500K-$1M revenue, $160K-$240K at $2.5M-$5M. Reaching $200K generally requires scaling beyond $2.5M in annual revenue with disciplined margin management — and recurring warranty revenue through reinsurance ownership is one of the highest-leverage ways to get there.

What does HVAC labor warranty cover?

A labor warranty covers the cost of the technician's time and work for covered repairs, separate from manufacturer parts warranties. This includes diagnostic time, travel, hands-on repair labor, and troubleshooting. Extended labor warranties can cover this cost for 5-10 years post-install, protecting homeowners from the expenses manufacturers explicitly exclude.

How to become a home warranty HVAC contractor?

Distinguish between joining a home warranty network (as a service provider paid per call) and running your own warranty program. Network membership means accepting their pricing and terms; running your own program through reinsurance gives you control over pricing, claims, profits, and customer relationships. The latter provides superior long-term financial benefits.

Is an HVAC warranty worth it?

From the contractor's perspective: yes, when structured correctly. A labor warranty program generates direct revenue per job, reduces open-ended liability, and builds long-term customer relationships—making it one of the highest-return additions to any HVAC business. The key is capturing underwriting profits rather than ceding them to third parties.