Introduction

Most HVAC contractors price their extended warranty programs without ever accounting for the full cost of running them. The result: some turn warranties into a reliable profit center, while others absorb losses they never saw coming — and never properly calculated.

Program pricing varies widely depending on provider type, coverage structure, and sales volume. What looks like a straightforward markup often hides administrative fees, claims exposure, and compliance costs that quietly erode the margin.

This article is for contractors who want a clear picture of what these programs actually cost. We cover typical price ranges, the factors that drive costs up or down, how to read a full cost breakdown, and a contractor-owned reinsurance alternative that shifts the economics in your favor.

TL;DR

- Contractors typically pay a per-contract wholesale rate to a third-party administrator

- The biggest cost drivers are coverage duration, local labor rates, program type, and annual install volume

- Higher install volume usually unlocks lower per-contract wholesale pricing

- Uncovered liability from self-insured or poorly backed programs is the hidden cost most contractors miss

- Owning a reinsurance structure lets contractors capture underwriting profit instead of paying it to a third party

How Much Does It Cost for HVAC Contractors to Offer Extended Warranty Programs?

HVAC extended warranty program costs are not fixed. A contractor running 50 installs a year faces a very different cost structure than one running 500, and the program type chosen changes the entire pricing model.

What goes wrong when costs are misunderstood: Contractors either undercharge customers (eating the cost themselves), overprice the warranty (losing deals to competitors), or ignore warranty liability entirely—exposing the business to uncapped risk.

Wholesale Cost Tiers by Coverage Length

Specific wholesale pricing (what contractors pay) is proprietary across the industry. Major third-party administrators (JB Warranties, Trinity Warranty, OnPoint Warranty) require dealer registration before disclosing rate sheets, and no industry association publishes benchmark figures.

What we do know: Contractor wholesale costs are commonly estimated at 40-60% of the homeowner-facing price, though this ratio cannot be verified from authoritative public sources. Homeowner-facing pricing at point of installation typically ranges from approximately $300 to $1,500, varying by coverage scope, duration, and equipment type.

Coverage tier structure:

- 2-year warranties serve as introductory upsells — accessible price point, lower margin

- 5-year warranties hit the middle tier, balancing customer appeal with moderate contractor margin

- 10-year warranties carry the highest margin potential and are the most defensible upsell

Why Contractor Labor Warranties Fill a Real Gap

Major manufacturers — Carrier, Trane, Lennox — already offer up to 10 years of parts coverage when customers register equipment within 60-90 days of installation. Labor coverage is another matter entirely. It's either excluded or capped at 3 years (Carrier's optional Consumer Choice program is one example). That gap is exactly what contractor extended labor warranties are built to fill.

Program Setup and Enrollment Costs

Most third-party administrators operate on a per-contract purchase model with minimal barriers to entry:

Enrollment requirements across major TPAs:

- JB Warranties: Online portal registration; no published upfront fees or minimum volume requirements

- OnPoint Warranty: Online form and dealer agreement; no published fees or minimums

- Trinity Warranty: Online enrollment; no published fees or minimums

All three providers appear to charge only on a per-contract basis, making entry accessible for contractors of any size.

Hidden soft costs: Even with no hard enrollment fee, contractors must account for staff time and training. ACCA recommends two practices worth noting:

- Train service technicians to present warranty options on every call

- Roll warranty costs into equipment financing to reduce friction at the point of sale

Key Factors That Affect the Cost of HVAC Extended Warranty Programs

The price a contractor pays per warranty contract is shaped by technical, geographic, and operational variables. Understanding each one helps contractors negotiate better terms and structure profitable pricing.

Coverage Duration

Longer coverage windows mean more exposure for the administrator, which raises the contractor's wholesale cost. A 10-year warranty costs significantly more than a 2-year warranty — it covers more potential failure points as equipment ages.

As systems age, failure probability increases, cumulative labor costs rise, and components may become harder to source — all of which increase the administrator's risk exposure.

Local Labor Rates

Administrators price coverage based on expected claims costs, and labor rates vary dramatically by geography. According to May 2023 BLS data, HVAC technician hourly wages range from $24.21/hr in Idaho to $43.99/hr in San Jose — an 82% spread.

That gap has real consequences: a warranty labor claim costing roughly $242 in Idaho could run $440 in San Jose for the identical repair. Geographic cost differentials are a primary driver of regional variation in extended warranty pricing.

Contractors in higher labor-rate markets will pay more per contract but can also charge customers more, preserving margin if priced correctly.

Install Volume

Contractors doing more installs per year can negotiate lower per-contract wholesale rates with third-party administrators. Administrators don't publish their exact volume thresholds, but the tiered pricing principle is consistent across the industry.

Texas TDLR's service contract renewal fee structure illustrates how volume tiers work in practice: $250 for 0–250 contracts/year, $500 for 251–499, and $1,000 for 500+. It's a regulatory fee, not a wholesale rate — but it confirms that volume thresholds are a recognized dimension of this industry.

Type of Coverage Provider

The source of extended warranty coverage affects not just cost but risk exposure, claims responsiveness, and program flexibility. Four main structures exist:

- Manufacturer programs: Limited to branded equipment; Carrier's Consumer Choice is the primary example

- Insurance-backed service contracts: Supported by A-rated carriers; claims obligations survive even if the TPA ceases operations

- Third-party administrators (TPAs): Handle administration and claims processing while contractors serve as the sales channel

- Contractor self-insurance: The contractor funds and backs the program directly

Self-insurance carries a business continuity risk worth understanding: when an LLC or corporation dissolves, outstanding warranty obligations typically end with the entity, leaving customers no recourse for future claims. Sole proprietors and partners may remain personally liable for the full warranty period. Insurance-backed TPA programs eliminate this exposure entirely.

Cost Breakdown: One-Time vs. Ongoing Expenses

The full cost of running an extended warranty program extends beyond the per-contract wholesale fee. Contractors should map both one-time and recurring expenses to understand true program economics.

Program enrollment and setup (One-time):

- Dealer account fees (generally waived by major TPAs)

- Training time for staff

- Integration with quoting and invoicing systems

Per-contract wholesale cost (Recurring—per install):

- Paid each time a warranty is registered; typically the largest line item in program costs

- Grows proportionally with install volume — higher revenue also means higher wholesale outlay

- The primary variable contractors must build into pricing

Administration and claims support (Recurring):

- Some programs include full admin support

- Others charge extra for claims adjudication, contract management, or customer service

- "Full-service" TPA programs typically bundle all administration; "basic" programs may charge separately

Compliance and legal requirements (Periodic):

State regulations vary significantly — and compliance costs are separate from everything above. Under the NAIC Service Contracts Model Act, adopted in various forms across all 50 states, providers must maintain one of three financial security options:

- Reimbursement insurance policy (100% of liabilities covered)

- Funded reserve account plus security deposit

- $100 million net worth

State-specific compliance costs:

| State | Application Fee | Financial Security Requirement |

|---|---|---|

| Texas | $250 initial; $250-$1,000 renewal | 40% funded reserve + $250,000 deposit, or $100M net worth |

| Florida | $500 license fee | Net assets: $25,000-$300,000 |

| Washington | $250 registration | Reimbursement insurance, funded reserve, or net worth |

| Nevada | $1,000 registration; $1,000 annual renewal | $25,000 bond or 10% of gross consideration |

Most contractors cannot meet these thresholds independently. That's why the majority partner with a TPA — or explore reinsurance structures that shift compliance obligations and underwriting risk off the contractor's books entirely.

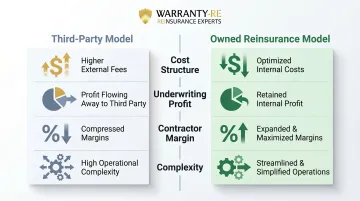

Third-Party Warranty Programs vs. Owning Your Own Warranty Company

Most contractors default to paying a TPA for warranty administration, but there is an alternative model where contractors establish their own administrator/obligor reinsurance company. This changes the cost and profit equation entirely.

| Third-Party Model | Owned Reinsurance Model | |

|---|---|---|

| Cost structure | Wholesale rate per contract + admin fees | Setup costs only; no recurring wholesale fees |

| Underwriting profit | Stays with the TPA or insurer | Retained by the contractor |

| Contractor margin | Markup between wholesale cost and customer price | Full spread between premiums collected and claims paid |

| Complexity | Low — plug in and sell | Higher setup threshold; ongoing compliance required |

WarrantyRE helps HVAC contractors build this structure. The model requires initial setup and compliance management, but it replaces recurring third-party fees with long-term profit capture. Warranty fees are built into job pricing, claims are fully administered, and any unused premium funds stay with the contractor — not the TPA.

The core tradeoff comes down to timing. The third-party model is simpler to enter — you pay per contract and move on. The owned-company model takes more to set up, but once running, it eliminates the recurring wholesale cost and routes that profit back to you.

What Most HVAC Contractors Overlook When Evaluating Warranty Program Costs

Most contractors evaluate warranty programs by looking at one number: the per-contract wholesale cost. That's only part of the picture. Three oversights consistently erode profitability:

- Skipping margin math on pricing. Contractors who don't calculate their required markup end up offering warranties at break-even or worse. The wholesale cost is only half the equation — profitable programs need an intentional pricing strategy built in from the start.

- Underestimating uncovered callback costs. Contractors without a program (or with a poorly backed one) still handle warranty service calls — they just pay out of pocket. ACHR News reports that HVAC contractors commonly budget 2% of total sales price for warranty callbacks, with best-practice rates falling between 0.5–1% of total labor hours. It's an invisible but real expense.

- Ignoring long-term service revenue. Warranty programs that lock in the contractor as the service provider for 5–10 years generate recurring revenue through maintenance visits and eventual system replacements. The per-contract fee looks different when measured against that lifetime customer value.

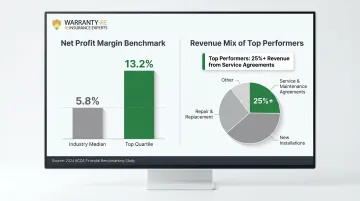

The gap between average and top-performing contractors reflects exactly these blind spots. The 2024 ACCA Financial Benchmarking Study found the median HVAC contractor net profit margin sits at 5.8%, while top-quartile firms reach 13.2%. Those top performers also derive over 25% of total revenue from service and maintenance agreements — and extended warranty programs are a documented path to get there.

Frequently Asked Questions

How much does an HVAC extended warranty cost?

Homeowner-facing pricing typically ranges from $300 to $1,500 depending on coverage duration and equipment type. Contractor wholesale costs are estimated at 40-60% of the retail price, though exact figures vary by provider, local labor rates, and coverage duration.

Are HVAC extended warranties worth the cost?

From a contractor's perspective, yes — when structured correctly. Extended warranties lock in future service revenue, reduce uncovered callback liability, and increase customer satisfaction and retention.

What is the $5,000 rule for HVAC?

The $5,000 rule is a widely cited HVAC industry decision heuristic: multiply system age (years) by repair cost. If the result exceeds $5,000, replacement is often recommended over repair. Contractors can use this to position extended warranties as protection before a system reaches that threshold.

What fees do HVAC contractors pay to offer extended warranty programs?

Fees typically include the per-contract wholesale cost (the primary ongoing expense), occasional enrollment or setup fees (often waived by major TPAs), and state compliance costs ($250-$1,000+ depending on state requirements and financial security options).

Can HVAC contractors make money on extended warranty programs?

Contractors profit two ways: markup on the warranty itself, and long-term service revenue from being the locked-in provider. A reinsurance model goes further, generating underwriting returns when claims fall below premiums collected.

What is the difference between a third-party warranty program and a contractor-owned reinsurance program?

In a third-party program, the contractor pays fees per contract and the administrator keeps the underwriting profit. In a reinsurance model, the contractor owns the warranty company and retains those profits directly when claims are less than premiums collected.