Introduction

Replacing an HVAC system isn't cheap. According to Modernize, based on 56,000 real homeowner projects, the average full HVAC replacement runs $11,590–$14,100 in 2026. At that price point, homeowners notice whether a contractor backs their work — and they're paying attention. A survey reported by ACHR News found that 61% of homeowners were more likely to hire a contractor offering a 10-year labor warranty.

For contractors, the real challenge is understanding what warranties cost, what they cover, and whether the program structure they're using is actually building profit — or bleeding it.

That answer depends heavily on program type. Costs range from near-zero for a basic manufacturer extension to several thousand dollars annually for a comprehensive contractor-managed program — and who captures the underwriting profit in between varies just as widely.

This guide covers pricing ranges by program type, what coverage typically includes, the factors that drive cost up or down, and what contractors need to know before they commit to a warranty structure.

TL;DR

- HVAC warranty program costs range from near-zero (manufacturer parts coverage) to $700+ per contract for comprehensive contractor-administered programs

- Coverage scope, equipment age, labor-rate geography, term length, and program structure are the biggest cost variables

- Third-party programs are simpler to start but transfer most of the premium — and profit — to the provider

- Contractor-owned reinsurance programs require more upfront setup, but let contractors keep the underwriting profit rather than sending it to a third party

How Much Does an HVAC Warranty Program Cost?

There's no single fixed price for an HVAC warranty program. What a contractor pays depends almost entirely on what they're buying, who's backing it, and who keeps the money when claims don't happen.

The risk of getting this wrong runs in both directions. Contractors who underprice warranty offerings absorb losses on service calls they should have been paid for. Those who overpay third-party providers often collect far less in reimbursements than the premium volume they generate would justify.

Many contractors never realize the profit potential embedded in well-structured programs — because they've never been offered an alternative. Understanding what each program type actually costs is the starting point.

Typical Cost Ranges by Program Type

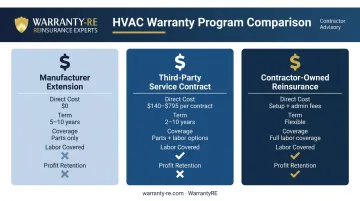

Manufacturer Warranty Extension (Entry-Level)

Most major manufacturers — Carrier, Trane, Goodman, Rheem, Lennox, York — follow a standard pattern: 5-year base parts coverage, extended to 10 years on registered equipment. Labor is excluded in every case. Registration windows typically run 60–90 days from installation.

For contractors, these cost nothing directly. But they also generate no revenue, cover no labor, and leave the contractor fully exposed to callback costs from day one.

Third-Party Extended Service Contracts (Mid-Range)

This is where most contractors land by default. Third-party administrators like JB Warranties and Trinity Warranty publish contractor-facing plans with published pricing.

Some published benchmarks:

- Homeowner-facing labor warranty pricing ranges from $180–$330 for 2-year coverage to $850–$1,600 for 10-year coverage, according to Trinity Warranty

- JB Warranties publishes contractor-facing rate sheets showing 10-year AC/heat pump labor coverage running approximately $140–$615, with parts-plus-labor combinations around $695–$795

- Reimbursable labor rates in third-party programs typically range from $85–$300/hour depending on market and plan tier

The contractor sells the contract, pays a portion of the premium to the administrator, and collects a margin — but the administrator keeps the rest. If claims run light, that difference stays with the provider.

Contractor-Owned Reinsurance Programs (Self-Owned)

In this model, contractors establish their own reinsurance company, legally owned by them, where warranty fees collected on installations flow into a segregated account rather than to a third-party provider. Claims are paid from that account. Unused funds stay with the contractor.

WarrantyRE, which has worked with home service contractors since 1994, structures exactly this type of program for HVAC contractors covering labor warranties on furnaces, AC systems, heat pumps, and mini-splits. Ongoing administration is fully managed, including:

- Claims adjudication and processing

- Compliance filings and tax returns

- Bookkeeping and performance reporting

- Staff training and onboarding support

What these programs typically include vs. exclude:

| Usually Included | Usually Excluded |

|---|---|

| Covered parts repair/replacement | Labor (manufacturer warranty) |

| Labor (service contracts, reinsurance) | Refrigerant (unless specified) |

| Claims administration support | Pre-existing conditions |

| Customer-facing contract terms | Cosmetic damage |

| Improper installation or maintenance |

What Does HVAC Warranty Coverage Include?

Coverage scope — not price — determines how many claims get paid, how customers experience the program, and how much financial risk the contractor actually carries. Two programs at the same price point can differ dramatically in what they protect.

Commonly Covered HVAC Components

Most extended warranty programs and service contracts cover the functional mechanical components of the system. Standard covered items typically include:

- Compressors — typically covered for up to 10 years due to high replacement cost

- Condensing units and outdoor components

- Evaporator and condenser coils — coil repair runs $600–$2,400 according to HomeAdvisor's 2025 component data

- Air handlers and blower motors

- Electrical components internal to the system

- Refrigerant — included in some contractor programs (JB Warranties, for example, lists this), excluded from most manufacturer warranties

The most important distinction in any coverage comparison is parts-only vs. parts-plus-labor. Manufacturer warranties cover parts — a failed compressor gets you a new compressor, not the labor to install it, not the refrigerant, not the diagnostic call.

That gap is entirely the contractor's exposure until an extended labor warranty or service contract fills it.

Compressor replacement runs $800–$3,000 in parts alone. Add labor at $85–$300/hour depending on the market, and a single claim can run well past $1,500. That's why parts-only coverage, while better than nothing, leaves contractors carrying the largest cost.

Common Exclusions to Know

Exclusions are where customer disputes originate. Standard exclusions across most programs:

- Pre-existing conditions at time of sale

- Improper installation or failure to perform required maintenance

- Cosmetic damage (cabinet dents, finish wear)

- Mismatched systems or non-conforming components

- Portable and window units

- Components still under active manufacturer warranty

Contractors using third-party programs inherit whatever exclusion language the provider wrote — which may not align with how they actually operate or what their customers expect. Those disputes land at the contractor's door regardless of who wrote the contract. Owning the program structure gives contractors more flexibility to define these terms in ways that match their business model and reduce friction at the point of claim.

Key Factors That Affect HVAC Warranty Program Costs

HVAC warranty pricing is shaped by a mix of operational and financial variables. Knowing which levers move cost helps contractors build programs that price correctly and stay profitable.

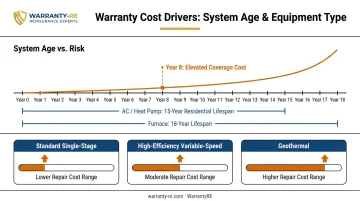

Type and Age of Equipment Covered

Older systems carry more failure risk. An HVAC system's expected service life averages around 15 years for residential air conditioners and heat pumps, and 18 years for gas furnaces, based on ASHRAE service-life data. A warranty written in year 8 of a 15-year system's life covers different risk than one written at installation.

System type matters too. Geothermal systems and high-efficiency variable-speed equipment carry more complex components and higher repair costs than standard single-stage systems. Per-claim exposure for those categories is higher, which should be reflected in warranty pricing.

Coverage Depth and Claims Cap

Per-claim limits directly affect what the contractor is on the hook for. A $2,000 cap functions very differently than a $5,000 cap when a compressor fails on a 4-ton commercial-grade residential system.

Higher limits mean:

- Greater financial exposure per claim event

- Need for stronger reserve backing or reinsurance support

- Higher premiums to customers — but also stronger perceived value

Customer Base Size and Claims Volume

Larger warranty portfolios spread risk more predictably. A contractor with 400 active contracts experiences much more stable claims averages than one with 40, where a single large claim can distort the entire program's economics.

SMACNA recommends contractors carrying direct warranty exposure maintain a reserve of 1–2% of equipment costs for self-insured programs. That benchmark also informs a key structural decision: whether to absorb that risk directly or shift to a reinsurance arrangement where the contractor owns the upside.

Program Structure and Who Retains the Risk

Program structure has the greatest impact on long-term profitability. In a third-party arrangement, the provider collects the premium, manages (or limits) claims, and keeps whatever isn't paid out. The contractor gets a flat reimbursement rate and no visibility into the economics.

In a contractor-owned reinsurance structure, that math inverts. The contractor collects the warranty fee, carries the claims obligation, and retains whatever remains. WarrantyRE helps HVAC contractors build this type of structure, handling entity setup, administration, and claims management so contractors aren't running a warranty back office alongside their service operations.

Third-Party HVAC Warranty Programs vs. Contractor-Owned Reinsurance

Most contractors default to third-party warranty arrangements. They seem simpler — and they are, upfront. But the cost comparison over time looks very different.

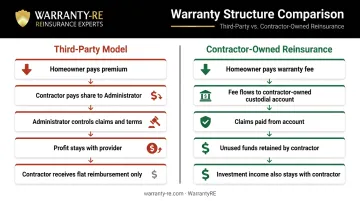

The third-party model:

- Contractor sells a service contract and pays a premium share to the administrator

- Administrator controls claims decisions, customer experience, and contract terms

- Profits flow to the provider; contractor receives a reimbursement when claims occur

- A denied claim or slow resolution reflects on the contractor even though the contractor had no say

The contractor-owned reinsurance model:

- Contractor establishes their own reinsurance entity (with WarrantyRE's support)

- Warranty fees flow into a segregated, contractor-owned custodial account at a U.S. Trust Company

- Claims are paid from that account; unused funds remain with the contractor

- WarrantyRE handles all claims adjudication, compliance, tax filings, monthly reporting, bookkeeping, and staff training — so the contractor isn't running a warranty operation on the side

- Reserve funds are invested in low-risk instruments (typically government bonds), and investment income also belongs to the contractor's reinsurance company

Third-party warranty companies stay profitable because they collect more in premiums than they pay in claims. A contractor-owned reinsurance structure captures that difference instead of paying it to a third party — and WarrantyRE's A-rated insurer backing means if the contractor's reinsurance company couldn't meet an obligation, the underwriting carrier covers it. That's the structural security contractors need to offer warranties confidently, without personally guaranteeing every claim.

What Most HVAC Contractors Get Wrong About Warranty Costs

Three patterns show up repeatedly when contractors evaluate their warranty programs poorly:

Pricing warranty at break-even. Many contractors cover expected claims without building in any margin. A well-structured program should carry its own profit, generate recurring customer touchpoints, and build retention. Price it correctly, and warranty becomes a revenue line — not an overhead item.

Assuming all program structures work the same way. A manufacturer extension, a third-party service contract, and a contractor-owned reinsurance program have different economics, different risk profiles, and different long-term outcomes. Choosing based on simplicity alone often means leaving consistent warranty revenue on the table.

Underestimating what happens when claims go wrong. When a third-party provider denies a claim or delays resolution, the customer calls the contractor. That complaint lands on your reputation regardless of who made the decision. Contractors who own their program control how those situations get resolved — and how customers feel afterward.

Frequently Asked Questions

How much does an HVAC contractor warranty program cost?

Costs range from near-zero for manufacturer parts coverage to $695–$795 per contract for parts-plus-labor programs through third-party administrators. Contractor-owned reinsurance programs involve setup costs and ongoing administration fees, but those are offset by the underwriting profit the contractor retains from unclaimed premium.

What does an HVAC warranty typically cover?

Standard coverage includes compressors, condensing units, coils, air handlers, blower motors, and internal electrical components. Labor, refrigerant, and ductwork vary by program — manufacturer warranties exclude labor entirely, while extended service contracts and reinsurance programs can include it.

What is the difference between a manufacturer's warranty and an extended HVAC warranty?

Manufacturer warranties cover part defects for a set term (typically 5 years base, 10 years registered) but exclude labor and refrigerant. Extended warranties or service contracts cover normal wear and tear repairs, often including labor, after or alongside the manufacturer's coverage.

Is an HVAC warranty the same as a home warranty?

No. A home warranty is a consumer product covering multiple systems and appliances throughout a house. A contractor-issued HVAC warranty applies only to the equipment and labor the contractor installs — the structure, scope, and claims process are entirely separate.

Can HVAC contractors make money from warranty programs?

Yes, when the program is structured correctly. In a contractor-owned reinsurance structure, the contractor retains premium not consumed by claims instead of sending it to a third-party provider. WarrantyRE builds this structure for HVAC contractors, turning warranty exposure into a revenue line the contractor controls.

What's typically excluded from HVAC warranty coverage?

Common exclusions include pre-existing conditions, cosmetic damage, mismatched systems, failure due to improper maintenance or installation, and components still covered under the active manufacturer warranty. Exclusion language varies significantly between third-party programs and contractor-owned structures.