Introduction

Most electrical contractors handle warranty obligations one of two ways: they absorb callbacks as an untracked labor cost, or they pay a third-party provider to manage the exposure. Neither approach captures the financial upside that's sitting right there in every job they close.

A contractor-owned reinsurance program changes that calculation. Without clear numbers, though, it's easy to compare program fees against "nothing" and conclude the math doesn't work.

This article breaks down what electrical warranty reinsurance actually costs, what drives those costs higher or lower, and how to evaluate whether the model makes financial sense for your business. It also reframes the cost question: the right comparison isn't program fees against zero — it's program fees against what you're already paying without tracking it.

TL;DR

- Electrical warranty reinsurance programs are funded by warranty premiums collected from customers — not out-of-pocket contractor capital

- Primary costs include initial company formation, annual administration, and maintaining a claims reserve fund

- Unused reserves stay in your reinsurance company as underwriting profit — they're not forfeited

- The IRS 831(b) election lets qualifying small insurance companies pay tax only on investment income, not underwriting profits — a cost offset most contractors miss

- The real cost comparison is program fees vs. the underwriting profit you're currently surrendering to a third-party provider

How Much Does Electrical Warranty Reinsurance Cost?

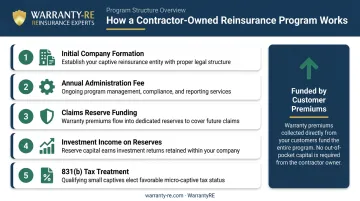

A contractor-owned reinsurance program doesn't work like a standard business expense you pay out of cash flow. The program is funded by warranty premiums you collect from customers at the point of sale, built into your job pricing. That changes the entire cost conversation.

When contractors misread this model, they tend to make one of three mistakes:

- Comparing program fees to the "zero" they spend now, ignoring untracked callback labor

- Underestimating the value of retaining underwriting profit that currently flows to their third-party provider

- Focusing only on setup fees without accounting for what the program generates over time

Typical Program Cost Ranges

Industry benchmarks for captive and reinsurance-backed structures point to the following general ranges — though exact costs vary by provider, state domicile, and program scope:

| Program Tier | Formation (One-Time) | Annual Administration |

|---|---|---|

| Entry-level | ~$50,000–$75,000 | ~$36,000–$60,000 |

| Mid-range | ~$75,000–$100,000 | ~$60,000–$85,000 |

| High-volume | $100,000+ | $85,000–$100,000+ |

Note: These reflect industry-sourced benchmarks for captive/reinsurance structures. State regulatory fees add modestly — Delaware, for example, charges a $300 application fee plus $3,200 processing fee for captive formation, with a $400 annual renewal.

Across all tiers, the economics are designed so that warranty premiums collected from customers fund both the reserve and the administration cost. The goal is profit capture, not an out-of-pocket expense.

WarrantyRE structures this under a single bundled arrangement — legal filings, claims adjudication, tax returns, and compliance renewals are all included, with no separate line items added later.

Key Factors That Affect the Cost of Electrical Warranty Reinsurance

Pricing depends on four primary variables: annual premium volume, coverage scope, your claims history, and the administration provider you choose.

Annual Premium Volume

Total warranty premiums collected annually drive both program cost and profit potential. Higher volume means a larger reserve, more underwriting profit, and a lower effective cost-per-dollar-retained.

Contractors just starting out will see a smaller profit margin in year one. That changes as the install base compounds — every new job adds another warranty fee to the reserve, and unclaimed reserves stay in your company.

You don't need to be a large-volume operation to start. The program scales from smaller contractors upward, with economics that improve as volume grows.

Coverage Scope and Duration

Longer warranties (3-year, 5-year, or beyond) and broader coverage — labor plus service calls plus diagnostic — require larger claims reserves and more careful premium pricing. Broader coverage is often more attractive to customers and can justify higher warranty fees. The key is that coverage must be priced and reserved correctly to stay profitable.

Claims History and Callback Rate

A contractor's historical callback rate directly affects reserve requirements. Well-documented low callback rates can support lower reserve thresholds. Unknown or elevated rates require larger reserves as a buffer.

This is why tracking callback costs before entering a reinsurance program matters — not as a barrier to entry, but as a way to negotiate more favorable reserve terms and understand your true warranty exposure.

Administration Provider Selection

Full-service reinsurance administration bundles everything a contractor would otherwise manage separately. WarrantyRE, for example, covers:

- Company formation and compliance filings

- Claims adjudication and financial reporting

- Tax management and renewals

That eliminates the need for internal claims staff, separate compliance counsel, or a piecemeal accounting arrangement.

State regulatory requirements vary and can affect setup complexity. A full-service administrator handles those filings on your behalf, since insurance regulations vary significantly by state.

Cost Breakdown: What You're Actually Paying For

Understanding what the fees cover helps separate one-time investment from ongoing operating cost.

Here's where your money actually goes:

- Initial company formation (one-time): Legal entity formation, state and federal regulatory filings, and the compliance structure that establishes your company as an administrator obligor backed by A-rated insurers. You're building a legal entity you own outright.

- Annual administration fee (recurring): Ongoing program management — claims adjudication, financial statements, bookkeeping, Form 1120PC tax return preparation, compliance renewals, and performance reporting. For most contractors, this replaces the cost of dedicated internal staff.

- Claims reserve funding (recurring): Warranty premiums collected from customers are held in your reinsurance company's reserve account. Your company pays covered claims from this pool. Reserves not paid out as claims stay in your company as underwriting profit — money you keep.

- Investment income on reserves: Reserve capital earns investment income while it sits in your account. Short-term Treasury yields ran between 3.47% and 4.37% at the end of 2024. That return belongs to your reinsurance company.

- Tax treatment: Under IRS 831(b), qualifying small property and casualty insurers with under $2,900,000 in annual net premiums (2026 limit) are taxed only on investment income — not underwriting profits. That tax advantage alone can significantly offset program costs that most contractors overlook when running initial numbers.

What Electrical Contractors Miss When Evaluating Warranty Reinsurance Cost

Three blind spots consistently distort how contractors evaluate program economics:

The Profit You're Already Surrendering

The most common miscalculation is treating the current situation as "free." If you're using a third-party warranty provider, that provider is retaining underwriting profits on your premiums. If you're informally absorbing callbacks, those labor hours have a real cost — they just aren't tracked on a line item.

Consider a simple example: an electrical contractor completing 200 service upgrades per year at an average job value of $4,500, with a $200 warranty fee built into each job.

- Annual warranty premium collected: $40,000

- Claims reserve (40% of premium): $16,000

- Underwriting profit retained: $24,000

Under a third-party arrangement, most of that $24,000 flows to the provider. Under a contractor-owned reinsurance structure, it stays in your company.

At consistent volume, that $24,000 compounds annually into a material reserve — capital most contractors are currently building for someone else.

The Unfunded Warranty Liability Problem

As your install base grows, informal warranty obligations grow with it. Every new installation adds to an unquantified balance sheet exposure.

Accounting guidance treats probable warranty obligations as recorded liabilities — meaning a buyer, lender, or valuation firm will price them in, even if you haven't. According to IBBA's valuation framework, off-balance-sheet and contingent liabilities are adjusted to fair market value in business valuations. Unfunded warranty obligations directly affect what your business is worth.

A funded reinsurance structure transforms that liability into an asset — you have a reserve account, a compliant legal entity, and a documented claims history.

The 831(b) Tax Advantage

The IRS 831(b) election allows qualifying small insurance companies to be taxed only on investment income, not underwriting profits. For a contractor retaining $24,000 annually in underwriting profit, the tax difference is significant. This benefit is frequently overlooked in initial cost comparisons because contractors evaluate the gross administration fee without netting out the tax advantage that comes with the structure.

WarrantyRE manages the 831(b) election and associated tax filings on the contractor's behalf, including Form 1120PC preparation through insurance tax specialists — so contractors don't manage specialized tax filings in-house.

Frequently Asked Questions

How much does insurance cost for an electrical contractor?

According to Insureon, electricians pay roughly $684/year for general liability, $2,602/year for workers' comp, and $1,682/year for commercial auto on average. These are separate from warranty reinsurance — they transfer risk, not generate profit.

What does it cost to set up an electrical warranty reinsurance program?

Formation costs typically run $50,000–$100,000+ depending on program scale, with annual administration fees ranging from $36,000 to $100,000+. These costs are structured to be funded by warranty premiums collected from customers — not out-of-pocket contractor capital.

What are the ongoing annual costs of running a warranty reinsurance program?

Ongoing costs include the annual administration fee — covering claims adjudication, bookkeeping, tax returns, compliance renewals, and reporting — plus state regulatory renewal fees. With a full-service provider, these are structured to be covered by the warranty revenue the program generates, not drawn from operating cash flow.

Can electrical contractors own their own warranty company?

Yes. Through an administrator obligor reinsurance structure backed by A-rated insurers — the structure WarrantyRE administers for contractors — electrical contractors can establish their own warranty company, retain premiums, control the claims process, and keep underwriting profits that would otherwise go to a third party.

How does a contractor-owned reinsurance program compare in cost to a third-party warranty provider?

In a third-party model, you pay with profit — the provider retains underwriting gains. In a contractor-owned model, you pay an administration fee but retain all remaining underwriting profit. In most scenarios, the long-term cost of the reinsurance program is lower because the profit you keep exceeds the administration fee you pay.

Are there tax benefits that offset the cost of an electrical warranty reinsurance program?

Yes. The IRS 831(b) election allows qualifying small property and casualty insurance companies — including contractor-owned reinsurance entities — to be taxed only on investment income rather than underwriting profits. For the 2026 tax year, the premium ceiling is $2,900,000. For many contractors, the tax savings alone push the program into positive territory before underwriting profits are factored in.