Introduction

Here's an uncomfortable truth about contractor warranties: every dollar you pay to a third-party warranty provider is underwriting profit that leaves your business. The choice of reinsurance partner determines whether that changes.

Choosing the wrong reinsurance company means poor claims support, hidden fees, compliance exposure, and profits walking out the door. The right partner does the opposite — it turns your warranty program into a recurring revenue stream, with underwriting profits staying inside your business where they belong.

This guide walks through the key factors contractors should evaluate when choosing a warranty reinsurance company, so you can make a decision that actually serves your bottom line.

TL;DR

- Warranty reinsurance lets you own your warranty company and capture the underwriting profits third-party providers currently keep

- Look for an Admin Obligor model backed by A-rated insurers, with compliance, claims handling, and tax filing managed for you

- Evaluate partners on financial backing, claims support, contractor experience, fee transparency, and profit potential

- Since 1994, WarrantyRE has helped 400+ contractors nationwide build profitable reinsurance programs — no hidden fees, ever

What Is Warranty Reinsurance for Contractors?

Warranty reinsurance allows contractors to establish their own insurance entity instead of paying a third-party warranty company to cover post-install or service warranties. Your reinsurance company absorbs the risk, holds the premium reserve, and keeps whatever isn't paid out in claims as underwriting profit—rather than sending that profit to an outside provider.

Here's how it works for home service contractors: premiums from customer warranty fees fund a reserve account held in trust. An admin fee covers administration, insurer fees, and claims handling. The remaining reserve—any portion not used to pay claims—becomes profit for your reinsurance company, not someone else's.

26 U.S.C. § 831 Under 26 U.S.C. § 831, qualifying small property and casualty insurance companies can elect favorable tax treatment on underwriting income—an additional financial advantage built into contractor-owned structures.

How It Differs from Third-Party Warranties

With a third-party warranty, you sell the coverage but the warranty company retains all earned reserve as their profit—you only earn the retail markup, not the underwriting profit. In practice, that means collecting a small markup while the warranty company keeps the bulk of what your customers paid.

Control shifts dramatically as well. A contractor-owned reinsurance company gives you authority over policy design, claims decisions, and how reserves are invested—a third-party arrangement leaves all of that in someone else's hands.

Key Benefits for Home Service Contractors

These structural advantages translate into concrete outcomes for contractors who make the switch:

- Premiums from customers fund your own reserve; unused premiums become direct business profit, not a windfall for a third-party provider

- Property and casualty insurers below the annual net premium threshold may qualify for IRC 831(b) tax treatment—the 2026 limit is $2.9 million—allowing taxation on investment income only, not underwriting income

- Owning the warranty program creates a direct financial incentive to do quality work and gives you control over how service callbacks are handled, reducing friction with customers

Why the Right Reinsurance Partner Makes All the Difference

Warranty reinsurance is not a self-service product. A capable partner handles every layer of the program on your behalf:

- Entity formation and compliance filings

- Claims adjudication and bookkeeping

- Staff training and ongoing program management

Attempting to manage these independently — without the right expertise — creates real legal, financial, and operational exposure.

That exposure compounds when the wrong partner is involved. Undercapitalized programs, unrated insurance backing, or hidden fee structures can quietly drain the profits reinsurance is supposed to generate. Choosing your reinsurance administrator deserves the same scrutiny as choosing to enter the program in the first place.

Key Factors to Consider When Choosing a Warranty Reinsurance Company

Not all reinsurance providers are structured the same way. Each factor below should be weighed against your business size, product type (HVAC, roofing, plumbing, electrical), and long-term goals.

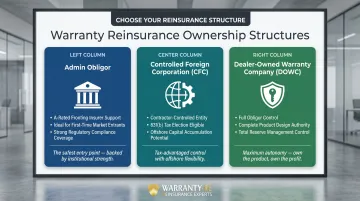

Program Structure and Ownership Model

The main structures available include:

- Admin Obligor: Your reinsurance company is supported by an A-rated fronting insurer that administers policies and cedes risk to your entity

- Controlled Foreign Corporation (CFC): You establish and control a reinsurance company, often able to elect 831(b) if qualifying

- Dealer-Owned Warranty Company (DOWC): You operate as the obligor for service contracts with full product design and reserve control

The structure chosen affects how much control you have over premiums, claims, and profit distributions. An Admin Obligor model tends to offer the best balance of ownership, compliance coverage, and financial security—especially for contractors entering reinsurance for the first time.

Financial Backing and Insurer Rating

The underlying insurance carrier's financial strength rating matters critically. If a fronting insurer is not A-rated, the validity and trustworthiness of all warranties issued under that program can be called into question, damaging your reputation and leaving customers unprotected.

AM Best Financial Strength Ratings provide an independent opinion of an insurer's ability to meet ongoing policy obligations. The rating tiers include:

- Superior: A++, A+

- Excellent: A, A-

- Good: B++, B+

Ask prospective reinsurance partners directly which insurance carrier backs their program and what that carrier's AM Best rating is before signing anything.

Claims Administration and Support

Claims adjudication—evaluating and approving or denying warranty claims—should be handled professionally and transparently. A reinsurance company that manages claims poorly creates customer dissatisfaction that reflects directly on your business.

Industry benchmarks show top performers achieve under 24-hour cycle times, 88-93% approval rates, and customer satisfaction scores above 4.5/5. Full-service administration should include:

- Staff training so your team knows how to explain the program to customers

- Ongoing performance reporting

- Active support when claims disputes arise

Compliance and Legal Management

Reinsurance companies are regulated financial entities. Forming and maintaining one requires ongoing legal filings, tax returns (including 831(b) elections where applicable), state registrations, and renewals—all of which must stay current to avoid penalties or program invalidation.

Vermont, the most commonly used captive domicile in the United States, outlines the formation and licensing process for various captive types including affiliated reinsurance companies.

Look for a reinsurance partner that manages all legal forms, compliance filings, and tax returns on your behalf. Most contractors don't have the internal infrastructure to handle this in-house.

Industry Experience with Contractors

Reinsurance structures built for auto dealerships don't automatically translate to home service contractor businesses. Claim types, seasonality, labor costs, and warranty term lengths differ significantly across HVAC, roofing, plumbing, and electrical. Your reinsurance partner should have experience navigating these differences.

For context: IBISWorld reports the HVAC industry generated $158.4 billion in 2025, while roofing contractors reached $92.5 billion and electricians $347.5 billion. These are distinct markets with distinct warranty challenges.

Ask for case examples or a demonstrated track record with businesses in your specific trade before committing to a program.

Fee Transparency and Profit Potential

Some reinsurance providers advertise profit participation but offset returns through hidden fees, management charges, or fund-level expenses not disclosed upfront. Request a full, written fee breakdown before entering any agreement.

A reputable reinsurance partner should clearly illustrate how much of each premium dollar goes to:

- Administration

- Insurer fees

- Reserve

They should also show you what realistic underwriting profit looks like based on your volume and expected claim ratio.

How WarrantyRE Helps Contractors Build Their Own Warranty Program

WarrantyRE is a reinsurance partner with over 30 years of experience, founded in 1994 by Tim Byrd in Southeast Virginia. Originally built for the automotive industry, the company now serves home service contractors nationwide — HVAC, roofing, plumbing, and electrical — bringing cross-industry claim structure knowledge that most warranty reinsurers simply don't have.

WarrantyRE's Admin Obligor model backs your contractor-owned reinsurance company with A-rated insurers. You retain full ownership of underwriting profits while customers see the financial credibility they expect from a legitimate warranty program.

Key differentiators that make WarrantyRE stand out:

- Handles claims adjudication, compliance, bookkeeping, tax filings, and performance reporting — no internal management required

- Trains your staff to confidently sell and explain the warranty program from day one

- Sets up your company quickly with no hidden fees — WarrantyRE only succeeds when you do

Conclusion

Choosing a warranty reinsurance company shapes how your contractor business handles risk, retains customers, and generates profit over time. The right partner makes that structure work in your favor. The wrong one creates compliance exposure and leaves money on the table.

When evaluating your options, keep the following priorities front of mind:

- Financial stability: Confirm A-rated insurer backing and transparent reserve practices

- Compliance track record: Verify the administrator handles filings, renewals, and state-level requirements

- Program flexibility: Ensure the structure scales with your growth and claim history

- Ongoing support: Look for active performance reporting, not just initial setup assistance

- Alignment of incentives: Choose a partner whose revenue model rewards your profitability, not just volume

The best time to evaluate a reinsurance partner is before committing to a program structure. Once you're enrolled, revisit performance at least annually — not just at setup — to confirm the program still aligns with your business growth and actual claim experience.

If you're ready to explore what a contractor-focused reinsurance program looks like in practice, WarrantyRE has been structuring these programs for contractors and dealers across the US since 1994.

Frequently Asked Questions

What is warranty reinsurance?

Warranty reinsurance is a structure where a contractor (or dealer) owns their own insurance entity to assume the risk of warranty claims, retaining the premiums and keeping unused reserves as underwriting profit instead of paying a third-party warranty provider.

What are the 4 types of reinsurance?

The four main types are facultative, treaty, proportional, and non-proportional. Contractor warranty programs typically use treaty structures with proportional cessions to capture underwriting results from portfolios of service contracts.

What factors do you consider most when choosing an insurance provider?

Financial stability (A-rated backing), program structure transparency, claims handling quality, compliance support, and industry-specific experience are the top factors contractors should weigh when evaluating a warranty reinsurance partner.

What are the four types of warranties?

Express warranties (written promises), implied warranties (merchantability and fitness), extended warranties (separately priced service agreements), and manufacturer warranties. Extended service warranties are most relevant to reinsurance programs contractors typically offer.

What are the 5 C's of insurance?

The 5 C's are coverage, cost, claims, company, and comfort/customer service. For contractors evaluating a reinsurance partner, "company" and "claims" carry the most weight — a provider's financial backing and claims adjudication process directly determine whether your program runs profitably or becomes a liability.