Introduction

Warranty revenue sounds straightforward until you actually sit down to account for it. Under ASC 606 — Revenue from Contracts with Customers — the treatment depends entirely on how a warranty is classified, and that classification requires real judgment, not assumptions.

For HVAC contractors, roofing companies, dealers, and other service businesses that bundle warranties into their pricing, this matters. Getting the classification wrong creates material misstatements: revenue overstated in one period, understated in the next, and a balance sheet that doesn't reflect actual economic reality.

The SEC has specifically flagged warranty and service arrangements as an area where performance obligation disclosures frequently need revision. This is one of the most judgment-intensive areas of revenue accounting, and the rules interact across multiple standards.

This article walks through the full accounting treatment:

- How to classify warranties under ASC 606

- How the five-step revenue model applies to warranty arrangements

- What the journal entries look like in practice

- Why program structure — including contractor-owned reinsurance arrangements — changes the analysis

TL;DR

- ASC 606 requires classifying every warranty as either assurance-type or service-type before recognizing any revenue

- Assurance-type warranties are not separate performance obligations — recognize revenue at sale, accrue costs under ASC 460-10

- Service-type warranties qualify as distinct performance obligations — defer revenue and recognize it ratably over the coverage period

- The five-step ASC 606 model determines how transaction price is split and when revenue is released

- Contractors running their own reinsurance companies face a layered accounting analysis spanning multiple legal entities

What Is Warranty Revenue Recognition Under ASC 606?

Warranty revenue recognition determines when warranty-related income is earned and reportable on the income statement — and getting it wrong creates compliance exposure. Under FASB's ASC Topic 606, the timing depends on what the warranty actually promises, not when cash is collected.

The core principle from ASC 606-10-05-3 is straightforward: recognize revenue to depict the transfer of promised goods or services to customers in an amount reflecting the consideration the entity expects to receive. For warranties, that means revenue timing is driven by when the obligation is satisfied, not by when cash changes hands.

How ASC 606 and ASC 460 Work Together

These two standards are complementary, not competing. Each governs a distinct element of a warranty arrangement:

| Warranty Type | Governing Standard | Treatment |

|---|---|---|

| Assurance that work meets agreed specifications | ASC 460-10 (cost accrual) | Not a separate performance obligation; accrue estimated costs at sale |

| Additional service beyond basic assurance | ASC 606 (revenue recognition) | Distinct performance obligation; defer and recognize over time |

| Guarantees other than product/service warranties | ASC 460 (excluded from ASC 606) | Evaluated under Topic 460 |

| Contracts transferring significant insurance risk | ASC 944 (insurance accounting) | Separate analysis required |

ASC 606 governs whether a warranty creates a performance obligation and how to recognize revenue. ASC 460-10 governs cost accrual for warranty obligations that aren't performance obligations. In practice, a single warranty program can trigger obligations under both standards simultaneously — which is why classifying each element correctly from the start matters.

Assurance-Type vs. Service-Type Warranties: The Classification That Drives Everything

This is where the analysis starts — and where most errors originate.

Assurance-Type Warranties

An assurance-type warranty is a promise that the product or service will function as intended and meet agreed-upon specifications for a defined period. Nothing more.

Under ASC 606-10-55-30 through 55-35, assurance-type warranties are not separate performance obligations. No portion of the transaction price is allocated to them. Revenue is recognized at the point of sale alongside the product, and estimated future warranty costs are accrued under ASC 460-10 as a contingent liability — not as deferred revenue.

Example: A one-year workmanship warranty included with an HVAC installation, covering defects in the contractor's labor. The contractor isn't promising anything beyond "the work will hold up as intended."

Service-Type Warranties

A service-type warranty provides the customer with something beyond basic assurance — extended coverage periods, repairs for damage outside of manufacturing defects, or separately negotiated protection plans. These must be treated as distinct performance obligations under ASC 606, with revenue deferred and recognized over the warranty period.

Example: A five-year labor warranty sold as part of a roofing contract, covering workmanship beyond the standard one-year period. The contractor is committing to stand ready to perform services over an extended term.

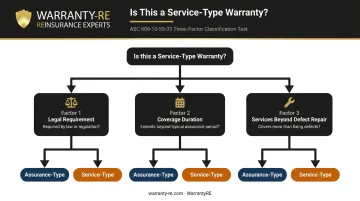

The Three-Factor Test (ASC 606-10-55-33)

FASB provides three specific factors for evaluating whether a warranty crosses into service-type territory:

- Warranties required by law are typically assurance-type

- Longer coverage periods suggest a service is being provided

- If the entity commits to performing services beyond fixing the original defect, the warranty is likely service-type

One additional indicator worth noting: if the customer can purchase the warranty separately at a stated price, that's a strong signal it's a distinct service-type performance obligation. However, FASB TRG Memo No. 29 and guidance from all four major accounting firms confirm that a warranty doesn't need to be separately priced to qualify as service-type. The substance of what's promised is what matters.

For contractors operating programs through WarrantyRE's structure, warranties are typically bundled into the job price rather than quoted separately. That doesn't automatically make them assurance-type — the nature and duration of the coverage still drive the classification.

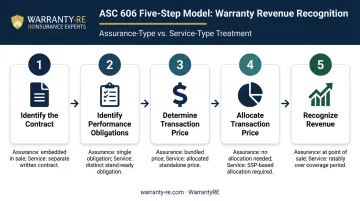

How ASC 606's Five-Step Model Applies to Warranty Revenue

Once you've classified the warranty type, ASC 606's five-step model dictates both how much revenue to recognize and when. Each step builds on the last — here's how each one applies to warranty arrangements specifically.

Step 1: Identify the Contract

Confirm that a contract exists with defined rights, obligations, and payment terms. For contractors, this is typically the installation agreement or a separately executed warranty service agreement.

Step 2: Identify the Performance Obligations

- Assurance-type warranty: Not a separate performance obligation. The product or installation is the only obligation to evaluate.

- Service-type warranty: A distinct, separate performance obligation alongside the core work — even if no separate line item exists on the invoice.

Step 3: Determine the Transaction Price

Identify the total consideration expected. If a service-type warranty is bundled at no extra charge, the full contract price still must be allocated between the installation and the warranty.

Step 4: Allocate the Transaction Price

With the transaction price identified, allocate it based on standalone selling prices (SSP) at contract inception, per ASC 606-10-32-31. For service-type warranties, this typically uses:

- The observable price when the warranty is sold separately, or

- An estimated price using adjusted market assessment or expected cost-plus-margin methods when no direct market exists

This allocation determines how much revenue is deferred versus recognized immediately. On multi-year programs, the deferred amount can be material and warrants careful documentation at contract inception.

Step 5: Recognize Revenue When Each Obligation Is Satisfied

- Assurance-type: Revenue is recognized at the point of delivery; warranty costs are accrued separately under ASC 460

- Service-type: Revenue is recognized over the coverage period as the stand-ready obligation is satisfied. PwC's TRG guidance confirms that straight-line (ratable) recognition is the appropriate method when the service obligation is satisfied evenly over the term.

Recording Warranty Revenue: Journal Entries and Financial Statement Treatment

Assurance-Type Warranty Entries

At point of sale:

- Debit: Warranty Expense

- Credit: Warranty Liability (estimated future claim costs)

When a claim is settled:

- Debit: Warranty Liability

- Credit: Cash / Inventory / Accounts Payable

No revenue deferral entry is needed. Full product revenue is recognized at sale.

Service-Type Warranty Entries

At point of sale:

- Debit: Cash (or Accounts Receivable) — full contract amount

- Credit: Revenue — product/installation portion

- Credit: Deferred Revenue (Warranty) — warranty portion allocated by SSP

As the warranty obligation is fulfilled (monthly or annually):

- Debit: Deferred Revenue (Warranty)

- Credit: Warranty Revenue

Balance Sheet Presentation

Deferred warranty revenue sits as a liability:

- Portion expected to be earned within 12 months → Current liability

- Remainder → Non-current (long-term) liability

ASC 460 warranty accrual liabilities are presented separately from deferred revenue. They reflect estimated future claim costs, not unearned income.

Income Statement Impact

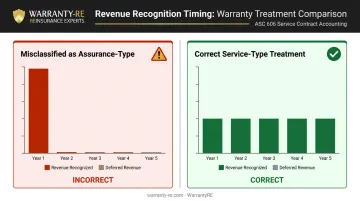

How you classify a warranty directly shapes what your income statement shows — and when. Misclassifying a service-type warranty as assurance-type causes revenue to be overstated in the period of sale and understated in every future period of the coverage term.

That gap matters beyond internal accuracy. Auditors and lenders reviewing multi-year financials will flag inconsistent revenue patterns, and a restatement to correct the misclassification can undermine credibility with investors or financing partners at the worst possible moment.

Common Misconceptions and Compliance Pitfalls

Misconception 1: All Warranty Revenue Is Recognized at the Point of Sale

Many contractors and dealers collect warranty fees upfront and assume all of it is immediately earned. For service-type warranties, cash collection timing is irrelevant — ASC 606-10-45-1 requires the advance payment to be recorded as a contract liability until the performance obligation is satisfied.

Misconception 2: Warranty Length Alone Determines the Type

Length is one of three factors in the ASC 606 assessment — the others being the nature of the promised coverage and whether services beyond defect repair are included. A short warranty covering services beyond basic defect repair can still be service-type. A longer warranty that only guarantees specification compliance may remain assurance-type. All three factors require judgment.

Misconception 3: Bundled Warranties Can't Be Separate Performance Obligations

ASC 606-10-55-32 makes this clear: the absence of a separate invoice line doesn't end the analysis. If the nature of what's promised goes beyond assurance of product functionality, you must evaluate it as a potential performance obligation — regardless of how it's packaged or priced.

Getting these classifications wrong creates real compliance exposure. When in doubt, the safer path is to document your reasoning and apply the ASC 606 framework consistently across all warranty arrangements.

When Warranty Program Structure Affects the Accounting Analysis

A contractor-owned warranty reinsurance company — a separate legal entity structured to underwrite and administer its own warranty obligations — adds a distinct layer to the accounting analysis.

In these arrangements, the contractor owns 100% of a separately incorporated reinsurance entity. An A-rated fronting insurer acts as the administrator-obligor backing the warranty contracts, and warranty fees built into job pricing flow into the contractor's reinsurance account rather than to a third-party provider.

WarrantyRE has helped home service contractors and auto dealers establish administrator-obligor reinsurance programs for over 30 years using this structure.

That separation matters for accounting: the entity selling the warranty to the customer and the entity bearing the underwriting risk are different legal entities, each with its own revenue recognition and reporting requirements.

Specifically:

- The contractor entity may have ASC 606 deferred revenue for service-type warranty obligations and ASC 460 cost accruals for assurance coverage

- The reinsurance entity receives ceded premiums, maintains its own financial statements, and may fall under ASC 944 (insurance accounting) if it transfers significant insurance risk — a facts-and-circumstances determination

- Premium flows between the contractor, the fronting insurer, and the reinsurance entity must each be evaluated at the entity level

WarrantyRE provides full financial administration for the reinsurance entity itself, including monthly financial statements and annual reporting coordinated with specialized insurance tax counsel. Contractors establishing these structures should also engage independent accounting counsel experienced in ASC 606, ASC 460, and potentially ASC 944 — the analysis at the contractor's operating entity level and the reinsurance entity level each requires its own evaluation.

Frequently Asked Questions

What is the journal entry to record a warranty?

For assurance-type warranties, debit Warranty Expense and credit Warranty Liability at the time of sale to accrue estimated future costs. For service-type warranties, credit Deferred Revenue (Warranty) at the point of sale for the allocated warranty portion, then recognize that balance into Warranty Revenue over the coverage period.

How is warranty revenue recognized?

Assurance-type warranty revenue is recognized at the point of sale alongside the product, because no separate performance obligation exists. Service-type warranty revenue is deferred at sale and recognized ratably over the warranty period as the stand-ready service obligation is fulfilled under ASC 606.

Are warranties capitalized or expensed?

Assurance-type warranty costs are expensed at the time of sale under the matching principle, recorded as warranty expense with a corresponding warranty liability. These obligations are not capitalized as assets.

What is the difference between assurance-type and service-type warranties under ASC 606?

Assurance-type warranties guarantee the product meets agreed specifications. Because they don't create a separate performance obligation, no revenue is deferred. Service-type warranties extend beyond that basic assurance, qualify as distinct performance obligations, and require revenue to be deferred and recognized evenly over the coverage period.

Does ASC 606 or ASC 460 apply to my warranty obligations?

Both can apply simultaneously. ASC 606 determines whether a warranty is a separate performance obligation and governs revenue recognition, while ASC 460-10 governs cost accrual for assurance-type obligations that fall outside ASC 606. Most warranty programs involve both standards applied to different elements of the same arrangement.

How does owning a warranty reinsurance company affect revenue recognition?

When a contractor operates a separate reinsurance entity, revenue recognition must be evaluated independently at each legal entity. Beyond ASC 606, ASC 460 and potentially ASC 944 insurance accounting standards may apply at the reinsurance level, which is why qualified accounting counsel and a structured administration program are important from the start.