Introduction

Every year contractors pay third-party warranty providers, they're handing over underwriting profits that could stay inside their own business. For home service contractors in HVAC, roofing, plumbing, and electrical trades, the choice between managing warranty risk yourself (self-insurance) and building a structured reinsurance program is one of the most impactful financial decisions you'll make.

Extended service contract programs typically show loss ratios of 30% or lower, meaning 70% of every warranty premium dollar goes toward commissions, administration, and underwriting profit. When you pay a third-party warranty company, you're funding their profit center — money that could be building equity in your own business.

That profit gap is why this decision matters so much for home service contractors specifically. Warranty claims are predictable enough to model actuarially — but one bad season of defective equipment, weather-stressed installations, or workforce quality problems can wipe out cash reserves if the wrong risk structure is in place.

This guide covers definitions of both approaches, a side-by-side comparison, and a clear framework for deciding which option fits your business stage and risk tolerance.

TL;DR

- Warranty reinsurance lets you own the company underwriting your warranties, keeping premiums, investment income, and profits instead of paying third-party providers

- Self-insurance uses cash reserves to pay claims directly — no formal entity, no insurer backing, no built-in profit structure

- Reinsurance offers catastrophic loss protection, tax planning advantages, and investment ROI potential; self-insurance offers simplicity but full exposure in high-claim years

- The right choice depends on warranty volume, financial position, and long-term growth goals

- Contractors focused on scaling will generally find warranty reinsurance delivers stronger long-term financial returns

Warranty Reinsurance vs. Self-Insurance: Quick Comparison

| Dimension | Warranty Reinsurance | Self-Insurance |

|---|---|---|

| Setup & Cost | Formal entity creation with legal/compliance costs; administered by partner like WarrantyRE | Minimal setup—dedicated reserve account or earmarked funds |

| Catastrophic Loss Protection | A-rated insurer backstop limits contractor exposure; ultimate liability rests with insurer | Zero protection—contractor absorbs 100% of claim spikes |

| Profit Potential | Captures 100% of underwriting profits; investment income on reserves | No profit mechanism—funds sit idle or deplete with claims |

| Tax Planning | IRC 831(b) election allows taxation only on investment income (premiums under $2.85M); deductible contributions | No tax advantages—reserves are after-tax dollars |

| Administrative Complexity | Full-service administration available; compliance managed professionally | Contractor handles all tracking, adjudication, and reserve management |

| Best Fit Profile | High-volume contractors selling warranties at scale; growth-focused businesses building sellable assets | Small contractors with limited warranty exposure; early-stage businesses testing warranty offerings |

The "Free" Myth

Many contractors assume self-insurance is "free" because there's no premium payment. The real cost shows up differently. If you're holding $40,000 in warranty reserves (required in many states) earning zero return, that's capital sitting idle. You could deploy it toward marketing, equipment, or hiring—or generate additional returns through a reinsurance structure instead.

Regulatory and Customer Trust Differences

Those capital differences connect to a broader credibility gap. Warranty reinsurance operates under formal regulatory compliance backed by A-rated insurers; self-insurance carries no such backing.

That distinction matters to customers. Formally backed warranties signal financial strength and enforce contractual accountability. An informal "we'll take care of it" promise rarely closes a high-ticket job the same way—and it won't hold up the same way if a customer pushes back.

What Is Warranty Reinsurance for Contractors?

Warranty reinsurance is a structure where the contractor forms their own administrator-obligor reinsurance company, collects warranty premiums from customers, and the reinsurance entity assumes the risk of paying claims—with an A-rated insurer as a backstop for catastrophic exposure.

The Administrator-Obligor Model

The contractor's reinsurance company serves dual roles:

- Administrator: Manages claims, compliance, financial reporting, and program operations

- Obligor: Holds financial responsibility for paying warranty claims

This dual role means the contractor controls the claims experience rather than outsourcing it to a third-party warranty company that profits from claim denials. When you own the obligor entity, you decide how aggressively or generously to handle claims—protecting your customer relationships while managing costs strategically.

How the Profit Mechanism Works

Premiums collected from customers that exceed claims paid accumulate as underwriting profit inside your reinsurance entity. Over time, this builds a reserve asset that belongs to you, not an external warranty provider.

Consider a practical example: an HVAC contractor includes a 2-year labor warranty on a $12,000 system replacement. The warranty fee—built into the proposal—flows into the contractor's reinsurance account. If the system performs well and no claims arise, that premium becomes profit.

Even when claims do occur, the contractor only pays actual costs. The remaining premium still accrues as profit inside the reinsurance entity.

WarrantyRE helps contractors establish and manage these programs, handling legal filings, compliance, claims adjudication, and financial reporting so contractors can focus on running their business. Founded in 1994, the company has served 400+ clients across the United States—starting in automotive reinsurance and expanding into the home service space over the past 30 years.

Tax Planning Advantages

Because the reinsurance company is a separate legal entity, premiums paid into it may be tax-advantaged. Under IRC Section 831(b), qualifying reinsurance companies with less than $2.85 million in annual net premiums may elect to be taxed only on investment income, effectively excluding premium income from taxable income. The operating business that pays premiums receives an ordinary tax deduction.

Critical caveat: The IRS has intensified scrutiny of 831(b) captive arrangements. IRS regulations classify arrangements with loss ratios below 30% over 10 years as "listed transactions", requiring extensive disclosure. Tax planning via captive reinsurance requires qualified professional guidance and genuine risk transfer, not tax-motivated premium levels.

Beyond tax treatment, accumulated reserves can generate additional ROI through investment. Initially, regulatory requirements limit funds to conservative instruments like government bonds. Once reserves exceed 125% of unearned premiums, excess funds may be invested more aggressively at the owner's direction.

Ideal Use Cases

Warranty reinsurance makes the most sense for:

- Contractors selling high volumes of service agreements or warranties

- Businesses looking to turn installs into recurring revenue streams

- Companies seeking long-term financial resilience rather than just short-term cost control

- Contractors building a sellable asset (recurring warranty revenue increases valuation multiples)

What Is Self-Insurance for Warranty Obligations?

Self-insurance means the contractor commits to covering defects and failures out of operating cash flow or a dedicated reserve account—there is no separate legal entity and no external insurer involved.

How It Works Operationally

The contractor sets aside a portion of revenue from each job into a reserve fund. When a warranty claim arises, funds are drawn from this reserve. The approach is straightforward: estimate your annual claims exposure, set aside funds each month, and pay claims as they occur.

The vulnerability: If claims spike in a given season—a product defect affects many installs, extreme weather stresses systems, or a workforce quality issue creates callbacks—the reserve can be depleted rapidly, creating a cash flow crisis.

State Financial Security Requirements Create Burden

More than 30 states regulate service contracts under frameworks modeled on NAIC Model Act #685. These typically require one of three financial security options:

- Reimbursement insurance from a licensed insurer

- Funded reserve of at least 40% of gross consideration received (less claims paid), plus a security deposit of 5% (minimum $25,000)

- Net worth of at least $100 million (or parent company guarantee)

For most home service contractors, the $100 million option is unreachable. The 40% funded reserve requirement means that for every $100,000 in warranty premiums collected, at least $40,000 must be held in reserve rather than deployed in the business.

With HVAC industry average net profit margins running between 2% and 5%—even high performers reaching only 10-25%—the opportunity cost of locking capital in self-insurance reserves is real and immediate. That capital could otherwise support marketing (benchmarked at 8-12% of revenue), equipment investment, or hiring.

Hidden Costs That Make Self-Insurance Less "Free" Than It Appears

- Requires dedicated staff time for reserve tracking, claims adjudication, and compliance documentation — none of it revenue-generating

- Idle reserve funds in a checking account earn nothing; that capital is simply frozen

- Unpaid claims from a depleted reserve trigger legal liability, licensing complaints, and lasting reputational damage

When Self-Insurance May Make Sense

Self-insurance fits a narrow set of scenarios:

- Very small contractors with limited warranty exposure (fewer than 100 agreements annually)

- Businesses in early growth stages where volume doesn't yet justify formal reinsurance structure

- Transitional approach before setting up a full reinsurance program

Once your warranty volume grows past that threshold, the math shifts — reserve requirements consume capital, administrative overhead compounds, and a single bad claims season can wipe out months of margin. That's the point where a structured reinsurance program starts to pay for itself.

Warranty Reinsurance vs. Self-Insurance: Which Is Right for Your Contracting Business?

The decision hinges on three key variables:

1. Annual Volume of Warranty Contracts Sold

Threshold question: How many warranty contracts or service agreements do you sell annually?

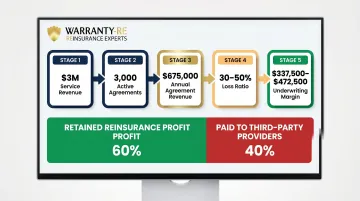

ServiceTitan benchmarks 1,000 or more service agreements per $1 million in service sales. At an average agreement price of $225 per year, a mid-size HVAC contractor doing $3 million in service sales would carry approximately 3,000 active agreements generating $675,000 in annual agreement revenue.

If the underlying loss ratio on these agreements is in the 30-50% range (consistent with actuarial data), the potential underwriting margin represents $337,500 to $472,500 annually. That's money contractors currently hand over to third-party warranty providers, or fail to capture entirely through informal self-insurance.

Rule of thumb: Once you're consistently selling warranties at scale (500+ agreements annually), the math shifts clearly toward reinsurance. Every premium dollar that previously went to a third-party provider now flows into an entity you own.

2. Financial Reserves and Ability to Absorb High-Claim Years

Self-insurance candidacy requires:

- Sufficient cash reserves to cover 2-3x your average annual claims

- Strong cash flow stability

- Low seasonal volatility in claims patterns

- Willingness to accept full downside risk

For contractors who can't comfortably absorb a bad claims year, reinsurance provides:

- Structural ceiling on downside exposure through A-rated insurer backing

- Protection against catastrophic claim years

- Predictable reserve requirements without personal asset risk

If one batch of defective equipment or a systemic installation issue could produce claims exceeding your reserves and threatening business operations, self-insurance is too risky.

3. Long-Term Goal: Sellable Asset vs. Near-Term Expense Management

If you're building a business to sell, warranty reinsurance creates a tangible asset. HVAC companies with higher maintenance contract revenue command higher valuation multiples in the 3x to 6x SDE range. A well-structured, profitable warranty program directly increases exit value.

If you're managing near-term expenses only, self-insurance works temporarily. You're still leaving money on the table, but it can serve as a starting point before you're ready to scale.

Situational Recommendations

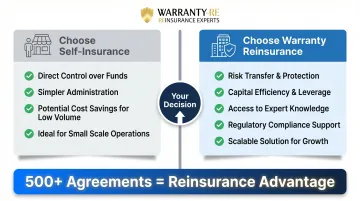

Choose self-insurance if:

- You're just starting to offer service agreements and annual volume is below 200 contracts

- Your business is in early growth stages where administrative overhead would outweigh reinsurance benefits

- You have strong cash reserves and very low claims volatility

- You view warranties as a temporary competitive necessity, not a profit center

Choose warranty reinsurance if:

- You consistently sell 500+ warranties or service agreements annually

- You want to capture 100% of underwriting profits instead of paying third-party providers

- You're building a business for long-term value and potential sale

- You want catastrophic loss protection and tax planning advantages

- You value customer-facing credibility (A-rated insurer backing)

Customer-Facing Value: Marketing Credibility

The structure you choose also shapes how customers perceive your warranty. Contractors backed by a licensed reinsurance entity can market their warranties with real credibility behind them. 64% of warranty purchasers cite peace of mind as their leading motivator, with 85% satisfied with value received and 81% planning to renew.

An insurer-backed warranty signals financial strength and commitment versus an informal "we'll take care of it" promise. When closing a $15,000 roof replacement or $12,000 HVAC system, that credibility difference matters.

Service agreement customers close replacement sales at approximately 70%, compared to 25-35% for marketing-generated leads. Warranty programs drive downstream revenue well beyond the agreement value itself, which makes the structure you choose even more financially consequential.

Conclusion

For contractors managing small warranty volumes or just starting out, self-insurance may be a practical starting point—but view it as temporary, not permanent. It leaves profits on the table and exposes your business to uncapped claim risk.

For growing contractors, owning a reinsurance entity means owning the underwriting profit, controlling the claims process, building a reserve asset, and turning every warranty sale into a contribution to your financial future. Those structural advantages compound over time in ways a simple reserve account cannot replicate.

Third-party warranty companies keep the underwriting profit your business generates. Informal self-insurance lets you avoid that cost—but you're still leaving money behind, because there's no mechanism to capture what's being earned.

Warranty reinsurance closes that gap. Your premiums build reserves inside your own company, claims stay under your control, and A-rated insurance backing protects against the unexpected. With the right program structure and administration behind it, warranties shift from an obligation you manage to an asset you own.

Frequently Asked Questions

What's the difference between reinsurance and insurance?

Insurance transfers risk from a policyholder to an insurer, while reinsurance is a mechanism where an insurer (or a contractor's reinsurance entity) transfers a portion of its risk to another insurer. In the contractor context, your reinsurance company is backed by an A-rated insurer as a safety net for large losses.

What is warranty reinsurance?

Warranty reinsurance is a structure in which a contractor establishes their own reinsurance company to underwrite the warranties they sell to customers, collecting premiums, paying claims, and retaining underwriting profits rather than paying a third-party warranty provider.

Why would a company be self-insured?

Companies choose self-insurance to avoid paying premiums to external insurers, to retain funds if claims are lower than expected, and to maintain direct control over claims handling. This approach requires sufficient cash reserves and works best for predictable, manageable loss exposures.

What is an example of self-insurance?

An HVAC contractor sets aside $150 per installation into a dedicated account to fund future warranty service calls or part replacements—rather than paying a third-party warranty company or home warranty provider. The contractor handles all claims directly from this reserve pool.

What are the 5 reasons insurers need to reinsure?

Insurers use reinsurance to:

- Protect against catastrophic or unexpected large losses

- Stabilize underwriting results year over year

- Increase capacity to underwrite more policies

- Improve solvency ratios

- Transfer risk on exposures that exceed their appetite

What are the 4 types of reinsurance?

The four types are facultative (individual risk), treaty (groups of policies), proportional (shared premiums and losses), and non-proportional (insurer pays only above a set retention limit). For contractor warranty programs, treaty reinsurance is most common.