Introduction

Every time an HVAC contractor completes a system installation, a roofing contractor seals the final shingle, or a plumbing contractor finishes a complex retrofit, there's a hidden profit leak happening—and most contractors don't even see it. Many contractors offering labor warranties today are unknowingly funding someone else's profit margin. When warranty claims stay low, the underwriting profit doesn't flow back to the contractor who did the work; it stays with the third-party warranty administrator.

For HVAC, roofing, plumbing, and electrical contractors, the choice between reselling an Extended Service Contract (ESC) and owning a Warranty Reinsurance program is a fundamental business decision. The structural difference between these two models determines who controls profitability, who owns the customer relationship after the job ends, and who keeps the money when claims run low. Understanding that difference is what separates contractors who treat warranty programs as a cost of doing business from those who turn them into a consistent revenue stream.

TLDR

- Extended Service Contracts earn contractors a commission, but third-party administrators capture underwriting profits

- Warranty Reinsurance lets contractors own the entity backing their warranties—retaining 100% of premiums and investment income

- ESCs are easier to start but limit earnings; reinsurance builds long-term asset value you actually own

- Predictable install volume is the clearest signal a contractor is ready for reinsurance

- Volume, growth trajectory, and long-term financial goals determine which model fits your business

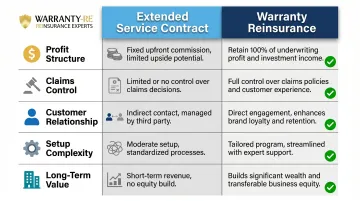

Extended Service Contract vs. Warranty Reinsurance: Quick Comparison

Here's how the two structures compare across the dimensions that matter most to contractors evaluating their warranty options.

| Dimension | Extended Service Contract | Warranty Reinsurance |

|---|---|---|

| Profit Structure | Contractor earns a small commission per contract sold; the third-party administrator keeps underwriting profit | Contractor captures 100% of underwriting profit plus investment income on reserves held in trust |

| Claims Control | Claims decisions rest entirely with the third-party provider — no contractor authority over approvals or outcomes | Contractor's reinsurance entity controls or directly influences claims review; a TPA handles paperwork, but the contractor owns the process |

| Customer Relationship | Warranty experience belongs to the third party; service failures damage contractor reputation despite being outside their control | Contractor owns the warranty lifecycle from sale through claim payment, strengthening trust and brand loyalty |

| Setup Complexity | Minimal setup — enroll with a provider and begin reselling immediately; no entity formation required | Requires reinsurance entity formation, compliance setup, and trust agreements; turnkey solutions reduce friction, but upfront complexity is higher |

| Long-Term Value | No equity built; when the provider relationship ends, the warranty program disappears with no transferable asset | Builds a funded, asset-backed company with accumulated reserves and investment income that compounds over time — and can be transferred or sold |

The core trade-off is speed versus ownership. ESCs are simple to start but leave profit and control with someone else. Reinsurance takes more to set up, but contractors keep what they build.

What is an Extended Service Contract for Contractors?

An Extended Service Contract in the contractor context is a service agreement sold to homeowners at project completion, backed and administered by a third-party warranty company. The contractor earns a commission for selling it, but the provider holds the financial risk—and keeps the profit margin.

The homeowner pays a premium for coverage beyond the contractor's standard workmanship warranty. The third-party administrator sets those premiums, manages the reserve pool, and adjudicates claims. When claims stay low, the administrator keeps the residual profit.

That spread between collected premiums and paid claims minus administrative costs is what contractors forfeit under the ESC model.

From a regulatory standpoint, service contracts are distinct from warranties under the Magnuson-Moss Warranty Act. A warranty is part of the purchase price; a service contract is sold for separate consideration. Most importantly, 45 US jurisdictions do not treat service contracts as insurance, which simplifies market entry for contractors using third-party providers.

Use Cases of ESCs for Contractors

ESCs make sense for contractors with:

- Install volume too low or inconsistent to justify building internal warranty infrastructure

- No in-house capacity for claims management or compliance oversight

- Interest in piloting a warranty offering before committing to a proprietary program

- Preference for immediate market entry without program development costs

The Service Contract Industry Council reports that 250 million service contracts are sold annually in the US, with SCIC members offering roughly 80% of all contracts. This is a mature, well-regulated market with infrastructure contractors can access immediately.

The trade-off is structural. Contractors using ESCs operate as resellers, not program owners — every dollar of underwriting profit flows to the administrator rather than back into the business that generated the customer relationship.

What is Warranty Reinsurance for Contractors?

Warranty Reinsurance flips the ESC model entirely. Instead of reselling a third party's product, the contractor establishes their own administrator obligor reinsurance company: an entity that backs warranty obligations, collects premiums, manages reserves, and captures the underwriting profit.

The Administrator Obligor Model

In an administrator obligor structure, the contractor's reinsurance company is the primary party responsible for administering policies, collecting premiums, and settling claims. This differs from dealer-obligor models where an intermediary facilitates placement but doesn't control operations.

The contractor's reinsurance entity is backed by an A-rated insurance carrier. If the contractor's company cannot meet obligations, the carrier absorbs the liability, protecting the contractor from catastrophic exposure while ensuring claims are always paid.

The contractor retains 100% ownership of their reinsurance company and all economic benefits, while the carrier provides regulatory backing and ultimate liability protection.

Financial Mechanics

When a contractor sells a labor warranty, the premium flows into their reinsurance company's trust account. Reserves are set aside for potential claims, invested conservatively in government bonds, and managed according to strict trust agreement guidelines.

The NAIC Service Contracts Model Act requires providers using funded reserves to maintain at least 40% of gross consideration (less claims paid) in reserve, a regulatory proxy for expected claim exposure.

Investment income earned on those reserves belongs entirely to the contractor's reinsurance company. Once reserves exceed 125% of unearned premiums, excess funds can be invested more aggressively at the contractor's direction or withdrawn for business use.

Tax Planning Advantage

Under IRC Section 831(b), qualifying small captive insurers with net written premiums not exceeding $2.2 million may elect to be taxed only on investment income, exempting underwriting profits from federal income tax. This creates a substantial tax deferral mechanism where warranty revenue accumulates in a tax-advantaged structure rather than flowing through as ordinary business income.

However, the IRS has scrutinized micro-captives closely. Notice 2016-66 designated certain 831(b) arrangements as "transactions of interest," and captives with loss ratios below 70% over five years face enhanced reporting. Tax benefits are real, but compliance rigor is non-negotiable.

Use Cases of Warranty Reinsurance for Contractors

Warranty Reinsurance is best suited for contractors with:

- Steady recurring install volume justifying premium flow and administrative setup

- HVAC companies selling annual service agreements on hundreds of installations

- Roofing contractors offering 5-10 year workmanship warranties on every project

- Plumbing and electrical contractors with repeat residential service generating predictable warranty revenue

Since 1994, WarrantyRE has helped business owners establish and manage administrator obligor reinsurance companies, handling everything from entity formation and compliance to claims adjudication and financial reporting. This end-to-end support removes the infrastructure barrier, making reinsurance accessible to contractors who would otherwise lack the legal, actuarial, and tax expertise to navigate the structure independently.

Which Model Makes More Business Sense for Contractors?

For contractors primarily concerned with minimal overhead and low commitment, an ESC is functional. For contractors focused on building a profitable, sustainable business with recurring revenue, the financial case for reinsurance is considerably stronger.

The ESC Model Has a Ceiling

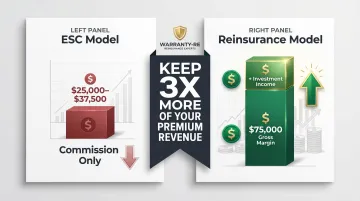

As install volume grows, so does the underwriting profit sent to third parties. Consider a hypothetical HVAC contractor selling $250,000 in warranty premiums annually. Under the ESC model, the contractor earns a 10-15% commission—$25,000 to $37,500. The administrator collects the full $250,000, sets aside reserves per the NAIC's 40% guideline ($100,000), pays administrative costs, and retains the underwriting margin if claims stay below reserves.

If claims come in at 30% of premiums ($75,000), the administrator's gross margin is $75,000 before administrative expenses. The contractor's take: their commission only. The administrator's take: the residual profit, investment income on reserves, and ongoing relationship equity.

Under a reinsurance model, that same contractor captures the full $75,000 gross margin, invests reserves for additional ROI, and builds an asset-backed company with transferable value.

Claims Control as a Business Risk Differentiator

The financial gap between models is one issue. Claims authority is another. Under an ESC, a third party's claims decisions can damage contractor-customer relationships. A denied claim that the contractor believes should be covered erodes trust—yet the contractor has no authority to override the decision.

Under reinsurance, the contractor's entity oversees claims outcomes. While professional administrators handle paperwork, the contractor controls precedent, customer experience, and resolution standards. Research from ACHR News shows that contractors with active maintenance agreement programs see 80-90% customer retention rates compared to 40-60% for general service customers. Claims control protects that retention by ensuring warranty experiences reinforce—not undermine—customer relationships.

Situational Guidance

Choose an ESC if:

- You have low or inconsistent install volume (fewer than 100-200 installations annually)

- You're testing warranty offerings before committing to infrastructure

- Administrative bandwidth is limited and you need a plug-and-play solution

- Your warranty program is a secondary revenue line, not a strategic priority

Choose Warranty Reinsurance if:

- You have consistent install volume justifying premium flow (200+ installations annually)

- You want to build long-term business equity and transferable asset value

- You're ready to operate a structured warranty program with professional support

- Retaining underwriting profit aligns with broader financial and tax planning goals

Contractors don't have to navigate this transition alone. WarrantyRE has helped contractors establish reinsurance programs since 1994, covering entity formation, compliance, claims administration, and financial reporting. Most contractors complete the move from ESC reseller to reinsurance company owner without taking on new operational staff.

Conclusion

ESCs are a legitimate entry point for contractors exploring warranty programs. But the reinsurance model is built for contractors who want to stop leaving money on the table and start building a warranty program that grows with every contract written. If you're writing enough volume to fund a reserve and you want ownership over what happens to that money, reinsurance is the more durable structure.

Contractors who move into reinsurance gain something an ESC can't offer: direct control over claims decisions, retained underwriting profit, and a program that builds equity instead of paying premiums to a third party. That shift — from paying for warranty coverage to owning the structure behind it — is what turns a warranty obligation into a profit center.

Frequently Asked Questions

What is the difference between a warranty and an extended service contract?

A warranty is a manufacturer's or contractor's direct promise to repair defects at no charge, included as part of the purchase price. An extended service contract is a separately purchased agreement backed by a third-party administrator, sold for separate consideration after the sale.

Are extended warranties worth it?

Reselling ESCs adds a revenue line, but the margins go to the provider. Contractors with strong install volume do better owning a reinsurance structure — capturing 100% of underwriting profits instead of commissions alone.

What are the main types of reinsurance?

The two primary types are proportional (quota share), where premiums and losses are shared in a pre-arranged ratio, and non-proportional (excess of loss), where the reinsurer pays only when claims exceed a specified threshold. Contractor warranty programs typically use proportional structures.

Why do insurers buy reinsurance?

Insurers use reinsurance to spread risk, protect against catastrophic loss concentrations, and stabilize financial results. For contractors, owning a reinsurance entity lets them capture the financial benefit of that risk-spreading rather than paying someone else to hold it.

How many years should my contractor offer a warranty?

Warranty length varies by trade. HVAC workmanship warranties commonly range from 1–5 years, roofing from 2–10 years, and plumbing/electrical from 1–2 years under California law — though requirements vary by state. Match your warranty term to your trade's typical claims window and your reserve capacity.