Introduction

Most business owners running contractor-owned reinsurance programs invest real energy in program setup and claims performance — then arrive at renewal season without a clear plan.

That gap has real consequences. A reinsurance treaty isn't a set-it-and-forget-it arrangement.

For HVAC contractors, auto dealers, roofing companies, and other home service contractors running their own warranty reinsurance programs, renewal is the single event that determines whether the program continues on favorable terms, faces repricing, or opens a compliance gap that affects statutory accounting credit.

This guide walks through how the renewal process works — from pre-renewal data preparation through contract execution and post-renewal administration — in practical terms built for program owners who want to stay ahead of the timeline, not react to it.

TL;DR

- Reinsurance renewal is a structured, documented process — not an automatic rollover

- Preparation should begin 90 to 120 days before the treaty anniversary date

- The NAIC nine-month rule (SSAP No. 62R, Paragraph 24) requires treaty execution within nine months of the effective date or the contract is treated as retroactive reinsurance

- Loss experience, premium volume, and data quality drive renewal terms more than any other factors

- A full-service administrator like WarrantyRE manages the entire renewal cycle, lifting the compliance and documentation burden off the program owner

What Is the Reinsurance Renewal Process?

The reinsurance renewal process is the structured sequence of steps through which an existing reinsurance treaty is reviewed, renegotiated if necessary, and formally reinstated or replaced for an upcoming coverage period.

This is distinct from three related but different events:

| Event | What It Means |

|---|---|

| Renewal | Extends the existing treaty relationship and program framework for a new period |

| Recapture | The ceding company pulls risk back from the reinsurer — often ending the arrangement |

| New program formation | Building an entirely new reinsurance company structure from scratch |

Renewal has one goal: continuous, compliant reinsurance protection that reflects the current risk profile, premium volume, and loss experience of the ceding company's book of business.

Even when loss experience is clean and the relationship is stable, the reinsurer still requires updated data submissions, a formal review, and signed documentation before the coverage period begins.

Why the Renewal Process Matters for Contractor-Owned Programs

For contractors and dealers running administrator-obligor warranty programs, renewal isn't a back-office formality. It's the most consequential compliance and financial event of the year.

What's at Stake Financially

Renewal terms directly affect the profitability of the entire program:

- Strong loss performance and organized reporting earn favorable terms that preserve underwriting profit and premium investment returns

- Poor claims experience or incomplete submissions trigger rate increases or reduced limits, compressing margins

- Non-renewal leaves outstanding warranty obligations exposed, creating immediate financial liability for the program owner

The Compliance Dimension

Renewal is also a regulatory obligation. Two regulatory standards govern what happens if the process breaks down:

- NAIC SSAP No. 62R sets statutory accounting rules for property and casualty reinsurance. Its nine-month rule requires the treaty to be executed within a defined window — miss it, and the accounting treatment shifts in ways that directly affect the program owner's annual statement.

- NAIC Credit for Reinsurance Model Law #785 restricts reinsurance credit to situations where statutory conditions are properly met. A procedural gap at renewal can eliminate that credit entirely.

Missing either requirement costs more than a poor negotiation outcome. Getting the process right is the negotiation.

How the Reinsurance Renewal Process Works

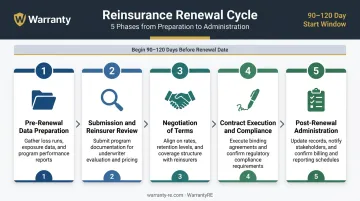

The end-to-end renewal cycle runs across five distinct phases, beginning months before the treaty anniversary and concluding with post-execution administrative setup.

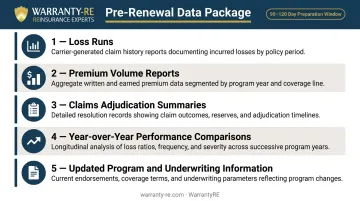

Step 1: Pre-Renewal Data Preparation

Pre-renewal work typically begins 90 to 120 days before the treaty anniversary date. During this phase, the ceding company — or its administrator — compiles the core program documentation the reinsurer will use to make its underwriting decision.

That package typically includes:

- Loss runs (current and historical)

- Premium volume reports

- Claims adjudication summaries

- Year-over-year performance comparisons

- Any updated program or underwriting information

The quality and timeliness of this data directly shapes what the reinsurer offers. A well-organized, complete submission signals program integrity. A late or incomplete one does the opposite. Reinsurers price that risk accordingly.

WarrantyRE prepares monthly financial statements and performance reports throughout the year, meaning clients aren't scrambling to compile data when the renewal window opens. The groundwork is already in place.

Step 2: Submission and Reinsurer Review

Once compiled, the data package goes to the reinsurer for formal underwriting review. This is not a passive extension. The reinsurer evaluates:

- Loss ratio — total claims paid relative to premiums ceded

- Retention adequacy — whether the ceding company's retained risk is appropriately sized

- Premium development — how the book has grown or contracted

- Portfolio composition — the mix of risk types and contract terms

Based on that review, the reinsurer will indicate whether it will renew on existing terms, propose adjusted pricing, or request additional information before deciding.

Step 3: Negotiation of Terms

Once the reinsurer's indication comes back, the parties negotiate the specifics:

- Premium rates

- Retention limits

- Reinsurance limits

- Coverage scope and any exclusions

Program owners with clean loss experience and organized administration negotiate from a position of strength. Those with incomplete submissions or deteriorating performance typically have fewer options. How the program was managed all year, not just the weeks before renewal, determines which side of that equation a client lands on.

Step 4: Contract Execution and Regulatory Compliance

After terms are agreed, the signed treaty document must be executed within a specific regulatory window.

The NAIC nine-month rule, codified in SSAP No. 62R, Paragraph 24, as referenced by NAIC INT 01-33, requires the contract to be finalized, reduced to written form, and signed within nine months of the treaty's effective date.

Miss that window, and the agreement is presumed retroactive. The ceding company must then record loss and loss expense reserves on a gross basis and report the reinsurance amount as a contra-liability — a material change in how the annual statement reads.

WarrantyRE manages all legal forms, filings, tax returns, and renewals on behalf of clients, ensuring treaty execution happens within the required window without the program owner having to track compliance deadlines independently.

Step 5: Post-Renewal Administration

Execution isn't the finish line. Once the new treaty is signed, several administrative tasks follow:

- Updating reporting templates to reflect new treaty terms

- Confirming premium remittance schedules

- Re-establishing claims reporting protocols

- Ensuring state filings reflect the renewed program structure

The quality of post-renewal administration determines whether the newly executed treaty runs smoothly — or creates friction — throughout the next coverage period.

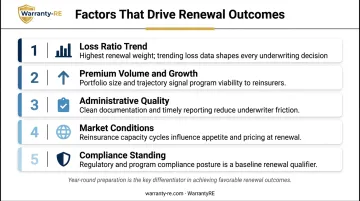

Key Factors That Affect Reinsurance Renewal Outcomes

Claims Experience and Loss Ratio

The loss ratio — total claims paid relative to premiums ceded — is the primary underwriting variable at renewal. No single metric carries more weight in the reinsurer's assessment.

Consistent low-loss performance lets program owners negotiate from strength and retain more premium-funded profit over time. A deteriorating trend does the opposite. Because no universal public benchmark exists for warranty and service contract reinsurance loss ratios, work closely with your administrator to track performance against your own program history and the terms of your current treaty.

Premium Volume and Program Growth

Reinsurers pay attention to trajectory. A growing book with stable loss experience signals a maturing, well-managed program — which increases reinsurer appetite. Declining premium volume or stagnant sales can prompt the reinsurer to reassess the program's long-term viability, sometimes resulting in less competitive terms even when loss experience is acceptable.

Quality and Timeliness of Administration

Organized loss runs, timely premium remittances, accurate bordereau reporting, and documented claims adjudication practices all signal program integrity. Reinsurers weight operational credibility heavily. A program that looks clean on paper but has administrative gaps raises questions the underwriter has to answer before committing to another year.

Market Conditions and Reinsurer Capacity

Broader market dynamics affect renewal pricing independent of individual program performance. According to Gallagher Re's January 2025 1st View report, renewal outcomes in 2025 were differentiated by loss experience and line of business — programs with strong performance fared better even in a mixed market environment. Specialty and casualty lines, which are the closest parallels to warranty and service contract reinsurance, showed more variability than property catastrophe lines.

Regulatory and Compliance Standing

Programs with documented compliance histories, clean state filings, and properly executed prior contracts renew with less friction. Administrative gaps — such as late-filed returns or unsigned treaty documents from prior periods — create questions at renewal that can delay execution or trigger regulatory scrutiny.

Across all five factors, the pattern is consistent: preparation and documentation reduce friction at renewal. Programs that track performance, maintain clean administration, and stay current on compliance give reinsurers fewer reasons to push back on terms.

The factors that matter most at renewal:

- Loss ratio trend — the single most influential number in the underwriter's assessment

- Premium volume and growth — signals program health and long-term viability

- Administrative quality — clean bordereaux, timely remittances, and organized loss runs reduce underwriter uncertainty

- Market conditions — broader capacity shifts can affect pricing regardless of individual performance

- Compliance standing — late filings or unsigned documents create avoidable delays

Common Misconceptions About Reinsurance Renewals

"Renewal is automatic if there are no claims."

A clean claims record is a strong advantage, but it doesn't trigger automatic renewal. The reinsurer still requires updated submission materials, formal review, and an executed contract within NAIC timelines regardless of loss history. Missing that distinction has cost programs their renewal window — even with spotless loss histories.

"Renewals only matter for large programs."

Every program operating under a reinsurance treaty — regardless of size — is subject to the same SSAP No. 62R documentation and execution requirements. The NAIC Credit for Reinsurance Model Law does not create exemptions for smaller contractor-owned or dealer-owned programs. Failure to comply can result in loss of statutory accounting credit or unprotected coverage gaps.

"Negotiating terms at renewal is only about price."

Premium rates are the most visible variable, but structural elements have a larger long-term impact. Key structural variables include:

- Retention levels and how they shift risk back to the program

- Coverage scope and any exclusions added at renewal

- Claims handling procedures that affect payout speed and dispute resolution

- Reporting requirements that drive administrative overhead

A small rate concession paired with tighter retention requirements can ultimately cost more than the rate reduction saves.

Frequently Asked Questions

What is the 9-month rule for reinsurance?

The NAIC nine-month rule, embedded in SSAP No. 62R Paragraph 24, requires a reinsurance treaty to be formally signed and executed within nine months of its effective date. If the contract isn't executed within that window, it's presumed retroactive — which changes how the ceding company must account for it on its annual statement and can eliminate credit for reinsurance.

What is the process of treaty reinsurance renewal?

Treaty reinsurance renewal involves pre-renewal data preparation, submission of updated loss and premium reports to the reinsurer, negotiation of terms, formal contract execution within NAIC timelines, and post-renewal administrative updates. The cycle typically begins 90 to 120 days before the treaty anniversary date.

How far in advance should reinsurance renewal negotiations begin?

Plan to start at least 90 to 120 days before the treaty expiration date. That window allows time to compile performance data, address reinsurer questions, negotiate terms, and execute the contract within the nine-month rule window without rushing the final steps.

What happens if a reinsurance contract is not renewed on time?

A lapsed or late-executed treaty results in unprotected warranty obligations, loss of statutory accounting credit for reinsurance recoverables, and regulatory compliance exposure. Those consequences hit immediately — gaps in coverage, lost accounting credit, and potential regulatory flags for any active obligations still in the field.

Can reinsurance premiums and terms change at renewal?

Yes — rates, retentions, coverage limits, and structural terms can all be renegotiated at renewal. The direction of those changes depends primarily on the program's loss experience, the quality of the submission package, and prevailing reinsurance market conditions at the time of renewal.

What documents are typically needed for reinsurance renewal?

The core materials typically include current and historical loss runs, premium volume reports, claims adjudication summaries, a copy of the existing treaty, and any updated program or underwriting information requested by the reinsurer.