Introduction

A mid-sized HVAC contractor paying $60,000 a year in warranty premiums is, in most cases, funding someone else's profit. The 831(b) captive insurance company is an IRS-sanctioned structure designed to change that: your business owns the insurer, retains the premiums, and captures the underwriting profit that currently goes to a third-party carrier.

Setup costs vary widely. Depending on structure, domicile choice, and management approach, total first-year investment can range from under $30,000 for group captive participation to well over $250,000 for complex offshore structures. Misunderstanding this range is one of the main reasons businesses either overpay or set up incorrectly — creating compliance problems that cost far more to fix than to prevent.

This article breaks down the full pricing landscape: one-time formation costs, mandatory capital requirements, annual management fees, and domicile taxes. By the end, you'll know exactly what a properly structured captive should cost — and what red flags signal you're being overcharged or underserved.

TL;DR

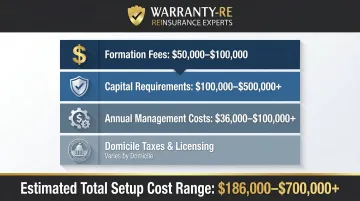

- One-time setup costs: $25,000–$100,000+ depending on captive type and complexity

- Capital requirements: $100,000–$500,000+ held in the entity as regulatory reserve, separate from formation fees

- Annual ongoing costs: $36,000–$100,000+ for management, compliance, and actuarial services

- 2026 IRS premium limit: $2.9 million annually under Section 831(b); underwriting income is tax-free

- Best fit for businesses with $500,000+ in annual insurable premiums

How Much Does It Cost to Set Up an 831(b) Captive Insurance Company?

There is no single fixed price for forming an 831(b) captive. Total investment depends on captive structure (single-parent vs. group vs. offshore), domicile choice, annual premium volume, and the level of professional management you engage.

Getting those variables wrong — underbudgeting capitalization, missing compliance fees, or mismatching structure to your risk profile — can trigger IRS scrutiny or leave you absorbing costs that wipe out the tax benefit.

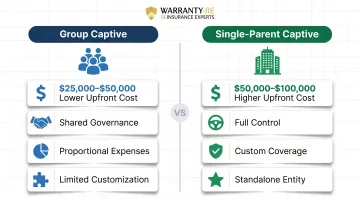

Basic / Group Captive Participation

Group captive participation is the entry-level option. Instead of forming a standalone entity, your business joins an existing group captive or cell captive structure. This approach offers lower upfront costs—typically starting around $25,000 to $50,000 for initial participation fees—and shared ongoing expenses distributed across multiple participants. You'll pay a proportional share of annual management and compliance costs, generally lower than running a single-parent structure.

Trade-off: Lower cost means less control. You'll share underwriting results and governance decisions with other participants, and your flexibility to customize coverage or exit the arrangement may be limited.

Best for: Businesses with lower premium volumes (under $500,000 annually) or those wanting exposure to captive mechanics before committing to a single-parent structure.

Single-Parent Micro-Captive (Standard 831(b) Setup)

The single-parent micro-captive is the most common structure for mid-market businesses. You form your own captive entity, make the 831(b) election, and insure risks specific to your operations—no shared governance or pooled results.

Typical upfront costs: $50,000–$100,000, covering:

- Feasibility study (required by most domiciles)

- Legal formation and governance documents

- Domicile licensing and actuarial review fees

- Initial actuarial opinion

These figures exclude ongoing management fees and required capitalization (discussed below). Industry sources, including captive management firms, note that formation costs at this level vary significantly based on domicile and complexity.