Introduction

Once warranty claims start eating into margins, many contractors begin asking who's really profiting from their protection programs—and whether there's a better structure they could own themselves. The question isn't academic: when you're paying premiums to third-party warranty companies, those firms capture underwriting profits that otherwise could stay in your business. For contractors who've watched service agreement revenue disappear into another company's balance sheet, the search for alternatives becomes urgent.

Two paths often surface in this conversation: the 831(b) micro-captive and the PORC (Producer-Owned Reinsurance Company). Both offer ownership and control, but most contractors don't understand the critical differences in how each works, who benefits, and what risks each carries. An 831(b) captive is primarily a tax planning vehicle designed for uninsured risks. A PORC is a profit-capture structure built specifically to let contractors own the economics of their service agreement or warranty program.

Choosing the wrong one doesn't just cost money—it can expose your business to IRS scrutiny or leave profit-capture opportunities on the table entirely. Here's how to tell them apart.

TL;DR

- An 831(b) captive is taxed only on investment income, exempting underwriting profits. Setup requires offshore or domestic domicile selection, actuarial studies, and ongoing IRS compliance management.

- A PORC sits behind an A-rated fronting insurer, capturing underwriting profits on service contracts with a straightforward compliance structure and no IRC § 831(b) election required

- The 831(b) targets tax reduction on premium income; the PORC targets direct profit capture from warranty programs — different tools, different goals

- For contractors selling service agreements, the PORC model directly captures profits that third-party warranty companies currently keep

- IRS compliance risk is a key differentiator: 831(b) captives have repeatedly appeared on the IRS "Dirty Dozen" list — properly structured PORCs do not carry that same exposure

831(b) Captive vs PORC Reinsurance: At a Glance

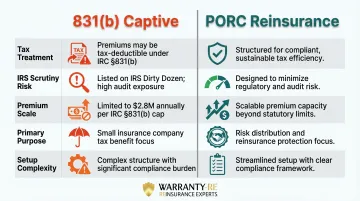

Tax Treatment

831(b) Captive: Underwriting profits are exempt from federal income tax; the company pays tax only on investment income, provided annual written premiums stay within the IRS threshold. The 2026 limit is $2.9 million.

PORC: Profits flow through the reinsurance company and are taxed as standard business income—the financial benefit comes from capturing underwriting profit, not from a special tax election.

IRS Scrutiny & Compliance Risk

831(b) Captive: Flagged on the IRS "Dirty Dozen" list of abusive tax shelters; subject to strict diversification rules, audit risk, and listed transaction reporting as of January 2025.

PORC: Not subject to the same IRS scrutiny when properly structured through a licensed fronting insurer; operates within standard insurance regulatory frameworks.

Premium / Revenue Scale

831(b) Captive: Annual written premiums must stay at or below $2.9 million (2026 limit) to qualify for the alternative tax treatment.

PORC: No premium cap; scales alongside the contractor's service agreement revenue without IRS election constraints.

Primary Purpose for Contractors

831(b) Captive: Best suited as a tax planning tool for businesses with specific uninsured or hard-to-insure risks; warranty and service contract profit capture is not its core design.

PORC: Designed specifically to let contractors own the economics of their service agreement or warranty program—replacing the third-party warranty company and capturing profits directly.

Setup & Ongoing Complexity

831(b) Captive: Requires actuarial justification, IRS election, and careful legal structuring; errors can result in denied deductions and penalties.

PORC: Requires forming a licensed reinsurance entity with an administrator and fronting insurer; setup is structured and straightforward with the right guidance.

What is an 831(b) Captive?

An 831(b) captive is a small insurance company that elects under Internal Revenue Code Section 831(b) to be taxed only on its investment income—meaning its underwriting income (premiums minus losses) is exempt from federal income tax, subject to staying within the annual premium limit. For 2026, that limit is $2.9 million.

That cap has evolved significantly since the provision was introduced in the Tax Reform Act of 1986 to encourage small business risk management. The PATH Act of 2015 updated the law, raising the premium cap from $1.2 million to $2.2 million (with annual inflation adjustments) and adding diversification requirements. Under the current rules, no single policyholder may represent more than 20% of annual premiums to satisfy the diversification test.

IRS Compliance Requirements

To qualify for 831(b) treatment, the captive must operate as a legitimate insurance company. This means:

- Demonstrating genuine risk shifting and risk distribution

- Charging actuarially sound premiums

- Maintaining proper licensing in its domicile

- Meeting diversification standards

The IRS has repeatedly challenged arrangements that fail these tests. Notice 2016-66 labeled certain micro-captives as "transactions of interest," requiring participants to file Form 8886 and material advisors to file Form 8918. In January 2025, final regulations formalized "Micro-Captive Listed Transactions" and "Micro-Captive Transactions of Interest," carrying disclosure and penalty regimes.

The IRS Scrutiny Landscape

831(b) captives have appeared on the IRS "Dirty Dozen" list of abusive tax schemes multiple times. Tax Court cases illustrate the enforcement pattern:

- Avrahami v. Commissioner (2017) — arrangement failed risk distribution; premiums not deductible

- Reserve Mechanical Corp. v. Commissioner (2018) — pooling deemed a sham; lack of risk distribution

- Syzygy Insurance Co. v. Commissioner (2019) — unreasonable premiums, late policies, lack of arm's-length dealings

- Keating v. Commissioner (2024) and Swift v. Commissioner (2024) — both IRS wins for lack of risk distribution

In June 2025, the IRS announced penalties against an organizer and seller of a micro-captive program under IRC § 6700 — a signal that enforcement is ongoing.

Legitimate Use Case for 831(b)

When structured correctly, an 831(b) captive can benefit businesses with genuine, hard-to-insure risks—cyber liability, supply chain disruption, reputational harm—that commercial markets won't cover affordably. The tax benefit is a secondary advantage, not the primary purpose. The 2025 final regulations distinguish abusive from non-abusive arrangements, signaling that some micro-captive structures may be legitimate when operated with proper risk transfer and business purpose.

Use Cases of an 831(b) Captive for Contractors

For a larger contracting firm with diverse, uninsurable operational risks—not warranty claims—an 831(b) captive might apply as a tax-efficient self-insurance vehicle alongside commercial coverage.

For contractors whose primary goal is to stop paying profits to third-party warranty administrators and capture those dollars themselves, an 831(b) captive is not purpose-built for that outcome. It introduces disproportionate compliance risk relative to the tax benefit gained.

What is PORC Reinsurance?

A PORC (Producer-Owned Reinsurance Company) is a reinsurance company owned by the contractor (or dealer) that sits in the financial structure behind a licensed, A-rated fronting insurer. The fronting insurer issues the service contract or warranty to the customer, and the PORC assumes the underwriting risk and profits through a reinsurance agreement.

How the Economics Work for Contractors

When a customer pays for a service agreement or warranty, those premiums flow through the fronting insurer into the contractor's own reinsurance company. After claims are paid, the remaining underwriting profit belongs to the contractor rather than a third-party warranty company.

According to Warranty Week's analysis of extended warranty economics, retailers often retain about 50% margin on the consumer price of extended warranties, leaving less than 50% of the retail price for risk and claims. To achieve a 10% profit, administrators target loss ratios near 65%, implying combined ratios around 90%. That means roughly 50% of a contract's retail price goes to administration and retailer margin. A PORC lets contractors recover that share directly.

The Admin Obligor Structure

The PORC is supported by an A-rated insurer, which provides regulatory legitimacy and customer protection. The contractor, meanwhile, controls claims adjudication, investment of reserves, and profit distribution. Full-service administrators like WarrantyRE handle legal formation, compliance, tax filings, and ongoing administration so contractors don't have to manage those details themselves.

The NAIC Service Contracts Model Act requires service contracts to be backed either by a reimbursement insurance policy from an authorized insurer or by the provider meeting substantial financial responsibility thresholds (such as $100 million net worth). A properly structured PORC satisfies this requirement through the fronting insurer's licensed policy.

The Compliance Profile

That regulatory clarity carries into how PORC programs are treated at the federal level. PORC reinsurance operates under standard state insurance regulation through the fronting insurer. It does not involve an IRS tax election and is not subject to the "Dirty Dozen" scrutiny that 831(b) captives face. The business purpose is direct profit ownership, not tax shelter.

Use Cases of PORC Reinsurance for Contractors

PORC is a strong fit for contractors who are currently handing premium dollars to a third-party administrator. That includes:

- HVAC contractors selling maintenance plans or equipment warranties

- Roofing and exterior contractors offering service agreements

- Plumbing and electrical contractors with recurring customer agreements

For each of these, PORC replaces the third party entirely, keeping underwriting profit inside the contractor's own company.

Unlike 831(b) captives, PORC programs have no premium cap. As the contractor grows their service agreement base, the reinsurance company scales with them and profit accumulates proportionally.

831(b) Captive vs PORC Reinsurance: Which Is Right for Your Contracting Business?

After comparing both structures, the decision comes down to what your business is actually trying to accomplish.

If the goal is to self-insure hard-to-place operational risks with a tax advantage, an 831(b) captive may be worth exploring with qualified legal and tax counsel. If the goal is to own the economics of your service agreement program and stop paying underwriting profits to third parties, PORC reinsurance is the more direct and purpose-built solution.

Address the IRS Risk Factor Directly

For contractors who may not have sophisticated tax and legal infrastructure, the compliance burden and audit exposure of an 831(b) captive can outweigh its benefits. IRS challenges, Tax Court losses for non-compliant arrangements, and ongoing regulatory activity around micro-captives provide important context. The January 2025 final regulations and June 2025 promoter penalties underscore the IRS's continued pursuit of abusive micro-captive structures.

Situational Guidance

In a PORC, the contractor is not primarily pursuing a tax break. They are becoming the warranty company — owning reserves, controlling claims, and earning underwriting profit that previously flowed to a third party. That shift in profit ownership is the entire point.

Choose an 831(b) captive if:

- You have legitimate uninsured business risks

- You have qualified legal/tax advisors managing compliance

- Your primary objective is tax efficiency on hard-to-insure risk

Choose PORC reinsurance if:

- You sell service agreements or warranties to your customers

- You want to capture underwriting profit directly from your existing customer base

- You want a scalable structure without IRS premium caps or abusive shelter risk

- Simplicity of administration matters as much as financial upside

These structures serve different purposes. Treating them as interchangeable is where contractors go wrong. WarrantyRE works exclusively with contractors to evaluate whether a PORC reinsurance program fits their warranty volume, customer base, and growth goals — before any commitment is made.

Conclusion

An 831(b) captive is a tax-focused insurance vehicle best suited for legitimate uninsured risk management with the right legal infrastructure. PORC reinsurance is a profit-ownership model purpose-built for contractors who want to capture the economics of their own service agreement or warranty program. They solve different problems — and confusing one for the other is an expensive mistake.

Here's the practical split:

- 831(b) captive: Built for tax efficiency and risk financing — not for owning your warranty economics

- PORC reinsurance: Built to capture underwriting profit, reduce callback costs, and convert installs into recurring revenue

If your goal is to stop funding third-party administrators with profits from your own customer relationships, PORC reinsurance is the structure designed to do exactly that. An 831(b) captive is not.

Frequently Asked Questions

What is an 831(b) captive?

An 831(b) captive is a small insurance company that elects under IRC Section 831(b) to pay tax only on its investment income, exempting underwriting profits from federal income tax. To qualify, annual written premiums must stay within the IRS inflation-adjusted threshold (currently $2.9 million for 2026), and the company must meet risk-shifting and risk-distribution requirements.

What is a producer-owned reinsurance company (PORC)?

A PORC is a reinsurance company owned by a producer (such as a contractor or dealer) that sits behind a licensed fronting insurer. The owner captures the underwriting profit from their service agreements or warranties rather than passing those profits to a third-party warranty company.

What is the difference between an insurance captive and a reinsurance captive?

An insurance captive directly issues insurance policies to the insured and assumes primary insurance risk, while a reinsurance captive (like a PORC) sits behind a fronting insurer that issues the policy to the end customer. The reinsurance captive assumes the risk and profit via a reinsurance agreement rather than through direct policy issuance.

What is the 831(b) limitation for 2026?

The IRS inflation-adjusted annual written premium threshold for 831(b) qualification in 2026 is $2.9 million. Exceeding this limit disqualifies the company from the alternative tax treatment on underwriting income.

What is the difference between captive insurance and traditional insurance?

Traditional insurance involves paying premiums to a third-party insurer that keeps any underwriting profit. Captive insurance allows the business to own the insurance company itself—retaining underwriting profits, controlling claims, and accumulating reserves—rather than funding an outside insurer's profitability.

Is captive insurance worth it?

For most contractors, the answer hinges on premium volume, risk profile, and how well the structure is set up and maintained. Contractors focused on warranty profit capture often find PORC reinsurance delivers more direct value with a cleaner compliance profile than an 831(b) micro-captive.