But tax strategy for HVAC companies isn't just about filing correctly at year-end. It's about proactive planning that keeps more revenue in your business year-round, reducing what you owe before April arrives rather than reacting to the bill afterward.

TL;DR

- HVAC businesses can deduct tools, equipment (via Section 179), vehicles, insurance, and labor — reducing taxable income substantially

- S-corp election cuts self-employment taxes once net profit clears $50,000–$60,000 per year

- SEP IRAs and Solo 401(k)s lower your tax bill now while building personal wealth for later

- Missing quarterly estimated payments triggers IRS penalties — consistent bookkeeping keeps you ahead of them

- Contractor-owned reinsurance companies capture warranty profits and open tax planning options that standard deductions can't touch

Why HVAC Businesses Face a Unique Tax Burden

The financial complexity of HVAC operations sets the industry apart from most trades. You're managing distinct revenue streams—installs, service calls, maintenance agreements—each with different profit margins and tax treatment. That complexity compounds fast:

- High equipment and parts costs that fluctuate with supplier pricing

- Seasonal cash flow swings that leave you flush in summer and tight in winter

- A workforce split between W-2 employees and 1099 subcontractors, each taxed differently

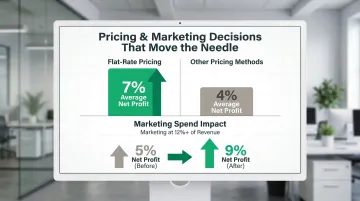

Industry data from ACCA's Contractor of the Future study shows that contractors using flat-rate pricing report about 7% average net profit versus 4% using other pricing methods. Those who increase marketing spend to at least 12% of revenue see net profit rise from 5% to 9%. These margins mean that tax planning decisions directly impact whether you're building wealth or just staying busy.

Without a deliberate strategy, HVAC owners commonly underpay estimated taxes during slow months and face large lump-sum bills in spring. The IRS compounds this pain with underpayment penalties—charged at 7% per year, compounded daily—that can add thousands to an already tight spring balance. A proactive tax plan is how you stop that cycle before it starts.

Essential Tax Deductions HVAC Owners Shouldn't Miss

Deductions reduce your taxable income, not the taxes you owe dollar-for-dollar. The difference between a $100,000 taxable income and an $80,000 taxable income can save you $4,000–$7,000 depending on your bracket. But deductions only work when you have proper documentation. A deduction backed by receipts and logs holds up during an audit. A claimed expense without proof becomes an audit risk.

Tools, Equipment, and Section 179

HVAC tools and equipment—diagnostic gauges, refrigerant recovery units, hand tools, ladders, tablets, safety gear—are deductible as ordinary business expenses. Under Section 179, qualifying equipment purchased and placed in service within the same tax year can be fully expensed upfront rather than depreciated over multiple years. For tax years beginning in 2025, the maximum Section 179 deduction is $2,500,000, with the deduction phasing out when total qualifying property exceeds $3,130,000.

Key distinctions:

- Repairs are deductible immediately (fixing a broken compressor, replacing worn belts)

- Capital improvements must be depreciated over time (upgrading an entire HVAC system, major building renovations)

- Bonus depreciation offers an additional option for large purchases, though it's phasing down: 40% in 2025, 20% in 2026, and 0% in 2027

If you buy a $15,000 diagnostic machine in November and place it in service before December 31, you can expense the full $15,000 on that year's return rather than spreading it across five years.

Vehicle Expenses

Service vehicles represent one of your largest deductible categories—if you track them correctly. The IRS allows two methods:

Standard mileage rate: For 2025, the business use rate is $0.70 per mile. Multiply your business miles by $0.70 and deduct the total.

Actual expense method: Deduct fuel, maintenance, insurance, repairs, and depreciation based on the percentage of business use.

Both methods require contemporaneous mileage logs showing date, business miles, destination, and business purpose for each trip. Missing logs are a common audit trigger. Vehicles used 100% for business can be fully deducted. Mixed-use vehicles require tracking the business percentage and applying it to total costs.

For trucks and vans with a gross vehicle weight rating (GVWR) above 6,000 lbs but below 14,000 lbs, Section 179 expensing is capped at $31,300 for 2025—separate from the overall $2,500,000 limit.

Labor, Subcontractors, and Insurance

These operating costs are fully deductible and represent significant dollars for most HVAC businesses:

- Employee wages are fully deductible as a business expense

- Subcontractor fees are fully deductible, but you must file Form 1099-NEC for payments of $600 or more to nonemployees, due January 31

- Liability, vehicle, workers' comp, and property insurance premiums are 100% deductible

Audit warning: Misclassifying employees as independent contractors is a known IRS and Department of Labor enforcement priority. The IRS evaluates behavioral control, financial control, and the relationship between the parties.

If you control when, where, and how someone works, they're likely an employee, not a contractor. File Form SS-8 if you need the IRS to make a formal determination.

Additional deductions:

- Home office expenses for owners managing the business from a dedicated home workspace

- Marketing and advertising costs—branded trucks, digital ads, flyers, website development

All require consistent documentation throughout the year, not scrambling at tax time.

Advanced Tax Strategies to Reduce Your Overall Liability

Deductions reduce the income you're taxed on. Advanced strategies reduce how much taxable income is generated in the first place—the difference between reacting to a tax bill and engineering a lower one.

S-Corporation Election

Electing S-corp status allows you to split income between a reasonable salary (subject to the 15.3% self-employment tax) and owner distributions (not subject to SE tax). For profitable HVAC owners, this split creates meaningful savings.

Analysis from SDO CPA shows that S-corp election typically starts making sense around $50,000–$60,000 in net business income, with clearer advantages at $100,000+. Sample savings:

- $75,000 net income: ~$2,948 annual savings

- $100,000 net income: ~$5,355 annual savings

- $150,000 net income: ~$10,485 annual savings

To qualify, you'll need to:

- Pay yourself a "reasonable salary" based on industry standards

- Run payroll with proper withholding

- Maintain clean books and records

- File a separate S-corp tax return (Form 1120-S)

Compliance costs typically run $2,000–$4,500 annually, so the election makes sense only when tax savings exceed those costs. Get a tax professional review before electing—doing this wrong creates more expense than savings.

Retirement Plans as a Tax Reduction Tool

Every dollar contributed to a qualified retirement plan comes directly off your taxable income. Two plans work well for HVAC business owners:

SEP IRA

- Contribute up to 25% of compensation (effectively 20% of net self-employment income for sole proprietors)

- 2025 cap: $70,000

- Can be established and funded by your tax return due date, including extensions

Solo 401(k)

- Combines employee deferrals ($23,500 for 2025, plus $7,500 catch-up if 50+) and employer contributions

- 2025 combined maximum: $70,000 ($77,500 with catch-up)

- Must be established by year-end; employer contributions can follow by the return due date with extensions

If you're a profitable HVAC owner facing a $15,000 tax bill, contributing $30,000 to a Solo 401(k) could reduce your tax liability by $7,000–$10,000 while funding your retirement.

The $2,500 De Minimis Safe Harbor Rule

The IRS de minimis safe harbor rule allows businesses without an applicable financial statement to immediately expense tangible items costing $2,500 or less per item or invoice. For businesses with an applicable financial statement, the threshold is $5,000.

This means small tools, tablets, diagnostic equipment, and parts under $2,500 get written off in full the year you buy them—no formal Section 179 election or depreciation schedule required. For an HVAC business buying dozens of hand tools, gauges, and safety equipment each year, this rule cuts through a lot of paperwork.

Hiring Family Members

Paying your children to work in the business does two things at once: it deducts wages as a business expense and shifts income out of your higher tax bracket. Wages to a child under age 18 are not subject to Social Security and Medicare (FICA) taxes in a sole proprietorship or partnership where each partner is a parent.

Wages to a child under 21 are also exempt from FUTA.

For 2025, the standard deduction for a dependent is the greater of $1,350 or earned income plus $450, up to the standard deduction for single filers ($15,750). This means a child earning $15,750 or less may owe zero federal income tax, while the business owner deducts the full amount.

One hard rule: the work must be legitimate, age-appropriate, and documented. Paying your 12-year-old $15,000 to "consult" won't survive an audit. Paying them a reasonable wage to answer phones, organize inventory, or maintain the website will.

Year-Round Tax Planning Habits That Keep More Money in Your Pocket

Quarterly estimated tax payments are not optional for most HVAC business owners—they're required. The IRS expects you to pay taxes throughout the year as you earn income, not in one lump sum in April.

Due dates: April 15, June 15, September 15, and January 15 of the following year.

Safe harbor rules to avoid underpayment penalties:

- Pay at least 90% of your current year's tax liability, or

- Pay 100% of your prior year's tax liability (110% if your prior-year adjusted gross income exceeded $150,000)

If you owe less than $1,000 after credits and withholding, no penalty applies. Miss these thresholds, and the IRS charges 7% annual interest, compounded daily.

Why bookkeeping matters:

Clean, categorized bookkeeping throughout the year makes every strategy in this article work. Without consistent records:

- Deductions get missed

- Audits become harder to defend

- Cash flow decisions are made blind

- Estimated payments are guesses, not calculations

Meet with a tax professional or CPA mid-year—not just in April—to review income and adjust estimated payments. Before year-end, that review is also when you make strategic calls: timing a major equipment purchase, maximizing retirement contributions, or catching an underpayment before it compounds into a penalty.

The Overlooked Strategy: Owning Your Own Warranty Reinsurance Company

Most HVAC contractors sell warranties backed by third-party providers, sending all the premium revenue out of their business. But contractor-owned reinsurance programs allow owners to establish their own administrator-obligor reinsurance company that captures those premiums, controls claims reserves, and keeps underwriting profits inside a structure the owner controls.

Here's how it works at the job level:

- You complete an installation — furnace, AC unit, heat pump, mini split — and include a labor warranty in your proposal pricing

- That warranty fee is built into the job price, not itemized as an add-on

- Instead of forwarding that fee to a third-party warranty company, it flows into your own reinsurance account

- You retain 100% of the underwriting profits from those premiums in a tax-advantaged structure

WarrantyRE has been helping HVAC contractors and home service businesses establish these programs for over 30 years.

Within a properly structured reinsurance company, contributions to your account come with significant tax advantages under IRS Code 831(b). Property and casualty insurance companies with less than $2,900,000 in annual net premiums may elect to be taxed only on investment income — not on premium income itself. That distinction alone creates tax planning opportunities well beyond standard deductions.

Premium reserves can be invested conservatively in government bonds, with all investment income belonging to your reinsurance company. Once reserves exceed 125% of unearned premiums, excess funds may be invested more aggressively at your direction. The business owner gains control over how and when profits are recognized — and over time, accumulated reserves can support retirement planning, reinvestment, or business continuity goals that a standard deduction strategy never reaches.

WarrantyRE provides full-service administration so you don't carry the operational load:

- Claims adjudication and compliance management

- Tax return preparation, bookkeeping, and all legal filings

- Onboarding, training, and performance reporting

You own 100% of the company and retain all profits, while WarrantyRE handles the back-office complexity.

If your installation volume is strong and your tax bill reflects it, a contractor-owned reinsurance structure can redirect a meaningful share of warranty revenue out of ordinary income — permanently, not just for the current filing year.

Frequently Asked Questions

What expenses are 100% deductible for HVAC businesses?

Immediately and fully deductible expenses include:

- Tools under the $2,500 de minimis threshold

- Consumable supplies and marketing costs

- Insurance premiums and software subscriptions

- Employee wages and subcontractor payments (with proper 1099-NEC documentation)

Receipts, invoices, and logs are required documentation for all of the above.

What can HVAC business owners write off?

Common write-off categories include:

- Equipment and tools (Section 179 or depreciation)

- Vehicles (mileage or actual expenses)

- Labor costs, insurance, and advertising

- Home office, professional development, and retirement contributions

One important note: write-offs reduce taxable income, not taxes owed dollar-for-dollar.

What is the $2,500 expense rule?

The IRS de minimis safe harbor rule allows businesses without an applicable financial statement to immediately expense items costing $2,500 or less per invoice. This means small equipment and tools don't need to be capitalized and depreciated—you write them off fully in the year purchased.

What is the most overlooked tax deduction for HVAC business owners?

Retirement plan contributions (SEP IRA or Solo 401(k)) are frequently overlooked because owners don't realize how much taxable income they can legally offset—up to $70,000 annually. Structural decisions like S-corp election and reinsurance ownership are even more overlooked because they require advance planning, not just documentation.

How can HVAC business owners avoid the 22% tax bracket?

Bracket management comes from reducing taxable income through retirement contributions, maximizing deductions, and timing large equipment purchases before year-end. Business structures like S-corps or reinsurance entities can shift or defer income further. A tax professional can model these scenarios based on your projected revenue.

How does the new $6,000 tax deduction work?

No current federal provision creates a universal "$6,000 tax deduction" for HVAC contractors. The likely sources of confusion are the 2025 IRA contribution limit of $7,000 or the Energy Efficient Home Improvement Credit (25C)—a homeowner credit with a $3,200 cap, not a contractor deduction. Verify any "$6,000 deduction" claim with a tax professional before acting on it.