Introduction

Every time an electrical contractor sells a labor warranty, money changes hands — but most contractors never see the profit from that transaction. They collect the warranty premium, hand it to a third-party provider, and the underwriting profit that could be theirs walks out the door. A warranty reinsurance program fundamentally changes that equation, letting contractors own the backend of their warranty business and capture the margins they've been leaving on the table.

The cost of setting up and running a reinsurance program varies based on structure, warranty volume, and administrative support. Most contractors focus on the setup fee — and miss the bigger number: capitalization. Once they account for both, though, many find the ROI case is stronger than the sticker price suggests.

Here's what the full investment actually looks like — and how to decide if it's the right move for your electrical business.

TL;DR

- Setup costs range from $50,000–$100,000+ covering formation, legal, and licensing fees

- Capitalization requirements start at $10,000–$250,000+ depending on your chosen domicile

- Annual warranty premium volume determines both program economics and reserve requirements

- Captive operating costs run 15–35% of premium, compared to 40%+ for commercial insurers — that gap is profit you keep

- The real question is how much you're currently handing to third-party providers versus how much you could retain; WarrantyRE's administrator obligor structure makes this viable even for mid-size electrical contractors

What Is an Electrical Warranty Reinsurance Program?

In the standard warranty model, an electrical contractor sells a labor warranty to a customer, collects the premium, and sends it to a third-party administrator. If claims stay low, the administrator keeps the underwriting profit. The contractor gets nothing but the margin on the sale — and the liability exposure.

A reinsurance program flips that structure. The contractor owns or participates in a reinsurance entity that captures underwriting profits instead. Warranty premiums flow into the contractor's company, claims are paid from that pool, and any surplus remains with the contractor as profit. It's a formal insurance structure, governed by the same regulations that apply to traditional policies.

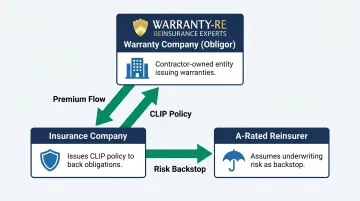

The Administrator Obligor Model

The most accessible structure for contractors is the administrator obligor (AO) model. Three entities participate:

- The Warranty Company (Obligor) — your owned reinsurance entity

- The Insurance Company — issues a Contractual Liability Insurance Policy (CLIP) to your entity

- The Reinsurer — assumes underwriting risk and liability, backed by an A-rated carrier

Your reinsurance company collects premiums and retains underwriting profit. If your entity can't pay claims, the A-rated carrier steps in — limiting your personal exposure to formation costs plus accumulated earnings while giving customers the security of a regulated insurance product.

WarrantyRE uses this model for electrical contractors. You own the reinsurance company, retain 100% of profits, and WarrantyRE handles claims, compliance, tax filings, and reserve management, all supported by A-rated insurance carriers.

This Is Not General Liability Insurance

That distinction matters when evaluating costs and structure. General liability policies cover bodily injury and property damage claims from third parties. A reinsurance program is a risk-financing structure where you assume underwriting risk on your own warranty obligations. You're not buying coverage from someone else — you're building a tax-advantaged company that profits from the warranties you already sell.

How Much Does an Electrical Warranty Reinsurance Program Cost?

There's no flat fee for a reinsurance program. Costs depend on structure (captive vs. cell vs. AO), warranty volume, and admin support level. The two most common budgeting mistakes:

- Assuming profits will cover everything without accounting for upfront capitalization and formation fees

- Overestimating costs by conflating reinsurance setup with traditional insurance premiums

The pricing below breaks down by volume tier — and the differences are significant.

Cost by Program Tier

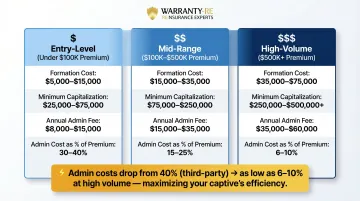

Entry-Level Program (Under $100K Annual Warranty Premium)

Smaller electrical contractors — those selling warranties on service calls, fixture installs, and occasional panel upgrades — typically start here. The most common structure is a sponsored captive or cell participation, such as a Vermont sponsored captive or protected cell company, where you share administrative infrastructure with other contractors to reduce overhead.

| Cost Category | Typical Range |

|---|---|

| Formation costs | $15,000–$50,000 (feasibility study often skipped; formation and licensing bundled) |

| Minimum capitalization | $10,000–$100,000 (Anguilla and Vermont sponsored captives offer the lowest entry points) |

| Ongoing admin fees | $5,000–$20,000/year (structured as 15–25% of premium or per-contract fee) |

Included: Basic claims administration, compliance filings, financial reporting, state licensing coordination

Separate: Tax preparation ($2,000–$5,000/year), initial capitalization, state-specific filing fees

Mid-Range Program ($100K–$500K Annual Warranty Premium)

Established contractors performing panel upgrades, EV charger installations, whole-home rewiring, and service agreements fit this tier. Common structures include the administrator obligor model (such as WarrantyRE) or a pure captive in a low-cost domicile like Vermont, Delaware, or Turks and Caicos.

| Cost Category | Typical Range |

|---|---|

| Formation costs | $50,000–$75,000 (includes feasibility study, legal formation, licensing, compliance setup) |

| Minimum capitalization | $100,000–$250,000 (Vermont pure captive requires $250,000; AO structures may start lower) |

| Ongoing admin fees | $36,000–$60,000/year for full-service administration |

Included: Claims adjudication, monthly financials, annual tax return coordination, compliance monitoring, staff training, reserve investment oversight

Separate: Initial capital (your equity in the company), actuarial services if required, lender-specific form filings

Established/High-Volume Program ($500K+ Annual Warranty Premium)

Large electrical contractors with commercial projects, multi-unit residential work, and active service agreement programs generate enough premium to justify a pure captive in a favorable domicile, with tax optimization available through an 831(b) election for programs under the $2.45M premium threshold.

| Cost Category | Typical Range |

|---|---|

| Formation costs | $75,000–$100,000+ (comprehensive feasibility study, multi-state compliance, tax structuring) |

| Minimum capitalization | $250,000–$500,000+ (regulatory requirements vary by domicile) |

| Ongoing admin fees | $60,000–$100,000+/year |

At $1M in premium, you're paying 6–10% in admin costs — compared to 40% with a third-party provider. The per-unit economics improve sharply at this volume.

Included: Dedicated account management, quarterly business reviews, proactive tax planning, performance analytics, customized reporting, strategic reserve investment management

Separate: Actuarial services for complex risk modeling, multi-state licensing fees, legal counsel for M&A or ownership changes

What These Ranges Cover (and What They Don't)

Included in most programs:

- Company formation and legal entity setup

- Claims administration and adjudication

- Regulatory compliance and state filings

- Monthly financial statements and annual reporting

- Tax return preparation (Form 1120PC)

- Reserve account management

Typically separate:

- Initial capitalization (this is your equity, not a fee)

- State-specific form filings for lender programs

- Actuarial feasibility studies (mid-to-large programs)

- Investment advisory fees if you exceed 125% reserve threshold and invest aggressively

Key Factors That Affect the Cost of an Electrical Warranty Reinsurance Program

Pricing isn't arbitrary. It's driven by business-specific variables and structural decisions — knowing which ones apply to you prevents budget surprises before you commit.

Volume of Warranties Sold

The number of warranties you sell each year determines both premium revenue flowing into your reinsurance entity and the scale of reserves required. Higher volume lowers per-unit admin costs but increases capitalization needs.

Example: An electrical contractor selling 500 warranties per year at $200 each generates $100,000 in annual premium. With fixed admin costs of $40,000/year, the contractor pays 40% in overhead. At 1,000 warranties ($200,000 premium), the same $40,000 admin cost drops to 20% — doubling profitability per contract.

Reserve requirements scale similarly. If claims run at 1% of sales (industry average for HVAC manufacturer warranties is 0.93%), you need reserves to cover expected claims plus an IBNR buffer. Higher volume requires larger capitalization but also generates more underwriting profit.

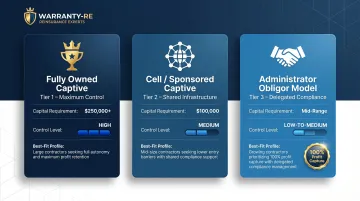

Program Structure and Ownership Model

Three main structures exist, each with a distinct cost and control trade-off:

- Fully owned captive (Vermont pure captive, Delaware captive): Highest formation cost ($250,000 minimum capital in Vermont), maximum profit capture. You own 100% of surplus and control all investment decisions once reserves exceed 125% of unearned premium.

- Cell participation or sponsored captive (Vermont sponsored captive, PCC structure): Lower entry barrier ($100,000 capital), shared infrastructure. You participate within a larger structure, sharing compliance costs but giving up some operational autonomy.

- Administrator obligor model (WarrantyRE, AmTrust-backed structures): Mid-range capital requirement ($50,000–$250,000), delegated compliance. You own the entity and capture 100% of underwriting profit; the administrator handles operational complexity.

Claims History and Risk Profile of Electrical Work

Electrical warranty programs must account for the risk profile of work being warranted. Panel upgrades, whole-home rewiring, and EV charger installations carry different claim frequencies than simple fixture replacements.

Higher expected claims rates require larger reserves, which increase capitalization costs. HVAC manufacturer warranty claims average 0.93% of sales over 20 years with a standard deviation of just 0.16% — highly predictable risk. Contractor labor warranties may vary based on workmanship quality, warranty term length, and service complexity.

If your historical claims run at 2% of warranty sales, you'll need roughly double the reserves of a contractor with 1% claims — directly impacting your capitalization requirement and reserve funding timeline.

Level of Administrative Support

You can choose how much operational burden you want to carry:

- Self-managed: Annual cost runs $10,000–$20,000/year. You handle claims calls, compliance filings, tax coordination, and reserve management — high operational burden with real compliance risk if errors occur.

- Full-service administration (like WarrantyRE): Annual cost runs $36,000–$100,000+ depending on volume. The administrator handles claims adjudication, regulatory filings, monthly financials, tax returns, bookkeeping, staff training, and performance reporting. Full-service programs often pay for themselves by preventing compliance errors, optimizing reserve investments, and freeing you to focus on billable work.

State Regulatory Requirements

State insurance regulations, filing requirements, and reserve minimums vary widely. Some states impose higher capitalization thresholds or complex compliance environments.

The NAIC Service Contracts Model Act establishes three financial security mechanisms (reimbursement insurance, funded reserves, or $100M net worth), but state adoption varies. NCOIL confirms that regulatory frameworks for service contracts differ substantially state by state — some require strict financial backing and licensing, others are more permissive.

Working with an experienced administrator like WarrantyRE helps you navigate these variables without overpaying for unnecessary compliance or underestimating state-specific costs.

Full Cost Breakdown: One-Time vs. Ongoing Expenses

Most electrical contractors are surprised to find that the largest "cost" — reserve capitalization — is actually money that stays theirs. The table below separates what you spend from what you fund.

| Cost Component | One-Time / Recurring | Description |

|---|---|---|

| Company formation and legal setup | One-time | Entity formation, legal documentation, state filings, and initial compliance setup. |

| Initial capitalization / reserve funding | One-time (with ongoing contributions) | Upfront capital held in reserve to cover potential claims — invested, retained as equity, not spent. |

| Ongoing administration fees | Recurring | Claims adjudication, compliance monitoring, state filings, reporting, and program analysis. |

| Tax preparation and financial reporting | Recurring (annual) | Separate tax returns (Form 1120PC), bookkeeping, and financial statements for the reinsurance entity. |

| Training and onboarding for contractor staff | One-time (with periodic updates) | Staff training on presenting and documenting warranty products correctly at point of install. |

Here's what those ranges look like in practice:

- Formation costs: Formation runs $50,000–$100,000+, including a $15,000–$25,000 feasibility study, $10,000+ in legal formation, and $5,000–$15,000 in licensing. WarrantyRE bundles formation costs into onboarding.

- Reserve capitalization: Minimum thresholds range from $10,000 (Anguilla) to $250,000 (Vermont pure captive). Reserve levels typically scale to 20–125% of net written premium. This capital sits in a reserve account under your company's name, can be invested for additional return, and counts as your equity — not an expense.

- Administration fees: Expect 15–35% of written premium annually, or $36,000–$100,000+ for fully managed programs. Full-service administrators bundle claims, compliance, and reporting into a single fee structure.

- Tax and financial reporting: Typically included in full-service packages. The 831(b) tax election can partially offset this cost for qualifying programs.

- Staff training: Proper onboarding at launch means technicians document warranty sales correctly from day one — reducing claim disputes and coverage gaps down the line. WarrantyRE includes onboarding and ongoing support as part of program administration.

What Most Electrical Contractors Miss When Budgeting for a Reinsurance Program

Focusing Only on Setup Fee Without Accounting for Capitalization

Many contractors see the $50,000-$100,000 formation cost and assume that's the total investment. They don't realize reserve funding is separate — and typically larger. If you need $250,000 in initial capital to meet domicile requirements and cover expected claims, that's a $350,000+ total commitment upfront.

Critical distinction: Capitalization is not a fee. It's your equity in the company. That money doesn't disappear — it's working for you, earning investment income, and building surplus you can eventually withdraw once reserves exceed 125% of unearned premium.

Ignoring the Cost of NOT Having a Reinsurance Program

Every year you sell warranties through a third-party provider, the underwriting profit that would belong to you in a reinsurance structure is gone permanently.

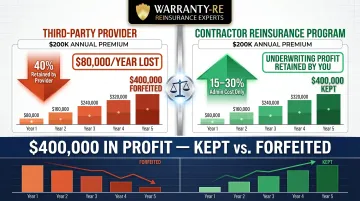

Frontdoor (American Home Shield) reported a 55% gross profit margin on $2.09 billion in revenue — meaning they keep 55 cents of every warranty dollar. Commercial insurers allocate roughly 40% of premiums to expenses and profits, while captive insurers operate at 15-30% expense ratios. That 10-25 percentage point differential is underwriting profit you could capture.

If you sell $200,000 in warranties annually and a third-party provider retains 40%, you're forfeiting $80,000/year. Over five years, that's $400,000 in lost profit — far more than the cost of establishing your own program.

Underestimating the Compliance and Administrative Burden of a Self-Managed Program

Contractors who attempt to run a reinsurance structure without expert administration often face compliance failures, claims disputes, or tax errors that cost far more than professional program management.

Specific risks include:

- IRS 831(b) audits triggered by improper administration — resulting in back taxes, penalties, and loss of the tax-advantaged structure

- Missed state filings that jeopardize your license to sell warranties in that jurisdiction

- Poorly adjudicated claims that expose you to regulatory action or litigation

Full-service administrators handle this complexity. WarrantyRE manages all legal forms, filings, tax returns, claims adjudication, compliance monitoring, and financial reporting. That lets contractors focus on running their electrical business instead of navigating reinsurance compliance.

Conclusion

The cost of an electrical warranty reinsurance program depends on structure, warranty sales volume, and administrative support level. There's no one-size number, but understanding the full cost stack — formation ($50,000-$100,000+), capitalization ($10,000-$250,000+), and ongoing administration (15-35% of premium) — allows for accurate budgeting.

The right measure isn't cost alone but net financial outcome. Contractors who build a reinsurance program stop sending underwriting profits to third parties and start building equity in their own warranty company. The "cost" of the program is offset — sometimes substantially — by the profits it captures and the tax advantages it provides.

For electrical contractors already selling warranties and outsourcing the backend, those underwriting profits are going to a third party every month. A reinsurance program redirects that income back to your own company. The real cost question isn't whether the program has expenses — it's what continuing without one is costing you.

Frequently Asked Questions

How much does reinsurance cost?

Reinsurance costs vary by structure and volume. For a contractor-owned warranty reinsurance program, costs include formation fees ($50,000-$100,000), minimum capitalization ($10,000-$250,000 depending on domicile), and ongoing administration (15-35% of premium annually). Full-service programs like WarrantyRE bundle claims, compliance, and reporting into annual fees scaled to warranty volume.

What is a reinsurance fee?

A reinsurance fee (or ceding fee) is the cost charged for transferring risk from the primary insurance layer to the reinsurance entity. In a contractor reinsurance program, this is typically structured as a percentage of warranty premium collected and covers administration, claims management, compliance, and risk oversight services.

What is ILF insurance pricing?

ILF (Increased Limits Factor) is an actuarial method insurers use to adjust premiums when coverage limits rise above a base level — developed by ISO as multiplicative factors applied to basic-limit rates. It applies to traditional liability insurance, not contractor warranty reinsurance programs. Warranty reinsurance pricing is driven by warranty volume and claims history, not coverage limit adjustments.

How long does it take to see a return on an electrical warranty reinsurance program?

Breakeven timing depends on warranty sales volume and program costs. Contractors with consistent install activity typically begin retaining net positive underwriting profit within 1-3 years. Contractors who were previously forfeiting large margins to third-party providers tend to reach payback faster.

How much is a $1 million insurance policy for electricians?

A $1 million general liability policy for electricians (covering bodily injury and property damage claims) typically costs $57-$78 per month, or roughly $684-$936 annually. This is standard business insurance, separate from a warranty reinsurance program, which captures profit from customer-facing labor warranties rather than protecting the contractor from third-party liability claims.

Can a small electrical contractor afford a warranty reinsurance program?

Program viability depends on warranty sales volume, not company size. Smaller contractors may find entry-level structures (cell participation, sponsored captives starting at $10,000-$100,000 capital) more appropriate than fully owned captives. The right administrator will assess whether your current volume justifies setup costs before recommending a program. As WarrantyRE puts it: "the largest misconception is you must be very large in volume — neither is true."