Contractor insurance and warranty reinsurance are structurally different financial tools with entirely different purposes. One is a required business expense that transfers risk to a third party. The other is a profit-generating structure you own. Confusing the two — or worse, not knowing the second one exists — means you're funding someone else's underwriting profit every year.

This article breaks down exactly how these two structures differ, what each one actually does, and how growing contractors can decide which they need (spoiler: it's usually both).

TL;DR

- Contractor insurance (GL, workers' comp, commercial auto, E&O) covers liability — premiums paid out, no financial return when claims stay low

- Warranty reinsurance is a separate legal entity you own; warranty premiums accumulate as profit inside your company, not a third party's

- Contractor insurance is mandatory; warranty reinsurance is optional but converts warranty sales into a recurring profit center

- The two serve entirely different functions — most growing contractors need both

- Contractors selling warranties at volume without a reinsurance program are funding someone else's underwriting profit every year

Warranty Reinsurance vs. Contractor Insurance: Quick Comparison

| Dimension | Contractor Insurance | Warranty Reinsurance |

|---|---|---|

| Purpose | Protect against third-party liability | Profit from warranty risk you already assume |

| Who Profits | Third-party insurer | You (the contractor) |

| Setup Required | Purchase from existing carrier | Form a separate legal entity |

| Catastrophic Loss Protection | Yes — core function | Yes — backed by A-rated insurer |

| Profit Potential | None — sunk cost | Yes — unused premiums become underwriting profit |

| Best Fit | All contractors (legally required) | Contractors selling warranties at volume |

Contractor insurance is a cost center. Warranty reinsurance is a profit center. Money paid into contractor insurance leaves your business permanently. Warranty reinsurance, by contrast, flows into an entity you own — building reserves, equity, and investment income that stay inside your financial ecosystem.

These aren't competing products. A contractor can and typically should carry both simultaneously, because they serve unrelated functions.

What Is Warranty Reinsurance for Contractors?

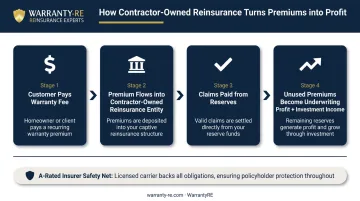

In the contractor context, warranty reinsurance means forming your own administrator-obligor reinsurance company. You collect warranty premiums from customers, and your reinsurance entity assumes the financial obligation to pay claims, backed by an A-rated insurer as a catastrophic loss safety net. You own this entity. Not a third-party provider.

Every warranty fee built into a job proposal flows into your reinsurance account rather than disappearing into an outside warranty company. When a claim occurs, it's paid from those reserves. When claims don't use the full reserve, the remaining funds belong to you.

The Administrator-Obligor Model Explained

Your reinsurance entity plays two roles simultaneously:

- As Administrator: Manages claims, compliance filings, financial reporting, and regulatory requirements

- As Obligor: Holds financial responsibility for paying covered warranty claims

Compare this to a typical third-party warranty arrangement: the external company controls both roles and keeps the profit. With an administrator-obligor structure, you control both roles and capture the profit.

The profit mechanism is simple: premiums collected from customers that exceed claims paid accumulate as underwriting profit inside your own reinsurance entity. Once balance sheet cash exceeds 125% of unearned premiums, excess reserves can be invested more aggressively at the direction of company ownership, adding an investment income layer on top of underwriting profit.

WarrantyRE handles the administrative complexity: claims adjudication from first call to final resolution, monthly financial statements, compliance filings, tax returns, licensing, and regulatory renewals. The contractor's job is to run their core business and sell warranties — the reinsurance infrastructure runs in the background.

That operational separation extends to the tax structure as well.

Tax Advantages and Business Asset Value

Under IRC Section 831(b), qualifying reinsurance companies with annual net written premiums under $2,900,000 (the 2026 threshold, per IRS Rev. Proc. 2025-32) may elect to be taxed only on investment income, effectively excluding premium income from taxable income. The operating contracting business that pays those premiums receives an ordinary tax deduction.

One important note: the IRS has increased scrutiny of micro-captive arrangements in recent years, with 2025 final regulations identifying certain arrangements as listed transactions. Qualified professional guidance — tax, legal, and compliance — is not optional here.

WarrantyRE works with specialized CPAs and legal counsel to ensure programs operate within IRS compliance standards.

Beyond tax efficiency, a well-structured reinsurance program is a sellable business asset. According to ClearlyAcquired's M&A data, HVAC businesses with more than 60% recurring revenue often achieve 7x to 9x EBITDA at exit, compared to standard multiples for non-recurring businesses.

A reinsurance program that generates documented recurring revenue and reserve assets strengthens that exit story considerably.

What Is Contractor Insurance?

Contractor insurance is a category of risk-transfer products that protect contractors from third-party claims, employee injuries, vehicle accidents, and professional errors. The core policies relevant to home service contractors:

- Commercial General Liability (CGL): Covers third-party bodily injury and property damage claims

- Workers' Compensation: Covers employee injuries on the job — required by law in nearly every state once employee thresholds are met

- Commercial Auto: Covers business vehicles and drivers

- Errors & Omissions (E&O): Covers claims arising from professional mistakes or omissions

Premium benchmarks vary significantly by trade, employees, payroll, location, and claims history. For general context: The Hartford reports small business general liability averages around $810/year for a $1M policy, workers' compensation averages $1,032/year, and HVAC businesses average $1,687/year for a Business Owner Policy. These figures are not trade-specific GL + workers' comp package totals, and actual costs depend heavily on your specific profile.

What Contractor Insurance Does NOT Cover

This is where the costly misconception lives. Contractor insurance does not cover warranty obligations to customers.

A CGL policy covers third-party bodily injury and property damage. It does not cover a customer's claim that their HVAC system stopped working 18 months after installation under a labor warranty. Standard contractor insurance doesn't touch that obligation.

Contractors who assume their GL policy backs their warranty promises are carrying unfunded liability. Covering that gap requires a separate structure — either a third-party warranty arrangement or a contractor-owned reinsurance program.

Key Differences: Warranty Reinsurance vs. Contractor Insurance

1. Purpose

Contractor insurance protects against losses caused by your work: accidents, injuries, lawsuits, errors. Warranty reinsurance takes a different approach entirely — it exists so you profit from the warranty risk you already assume when selling customers on your workmanship.

2. Where the Money Goes

With contractor insurance, premiums leave permanently. With warranty reinsurance, premiums flow into an entity you own — building equity, reserves, and investment income that compound inside a structure you control.

3. What Triggers a Payout

- Contractor insurance pays when something goes wrong: injury, lawsuit, property damage

- Warranty reinsurance pays on customer warranty claims — but low-claim years mean unused premiums become your profit, not a loss

4. Setup and Structure

Contractor insurance requires minimal setup — purchase from a carrier, maintain coverage. Warranty reinsurance requires forming a separate legal entity, meeting regulatory compliance standards, and implementing an administrative structure. That structure is what produces a formal, A-rated-insurer-backed warranty product — one that builds customer trust and helps close more high-ticket jobs.

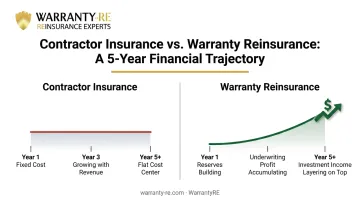

5. Financial Trajectory Over Time

| Year 1 | Year 3 | Year 5+ | |

|---|---|---|---|

| Contractor Insurance | Fixed cost | Growing with revenue | Flat cost center |

| Warranty Reinsurance | Reserves building | Underwriting profit accumulating | Investment income layering on top |

Contractor insurance is a flat cost that grows with headcount and revenue. Warranty reinsurance builds a reserve asset that compounds — by year five, most programs are generating underwriting profit and investment income simultaneously.

Which Structure Does Your Contracting Business Actually Need?

Most growing contractors need both — for entirely different reasons.

Contractor insurance is non-negotiable. It's legally required, contractually mandated by most commercial clients, and protects personal and business assets. There's no strategic decision here — you need it.

Warranty reinsurance is a strategic choice that becomes increasingly compelling as warranty volume grows.

General guidance on timing:

- Early-stage or lower-volume contractors selling fewer than 200 warranties per year may not yet justify the full structure — a third-party arrangement may be appropriate temporarily

- Contractors consistently selling 500+ warranties or service agreements annually should evaluate reinsurance seriously; at that volume, the math shifts clearly in their favor

- Volume isn't the only factor — WarrantyRE addresses a common misconception directly: "The largest misconception is you must be very large in volume or that it costs a lot of money to get started. Neither are true."

What You Leave on the Table Without Reinsurance

Every warranty sold through a third-party provider generates underwriting profit for that provider — not you. WarrantyRE frames it plainly: if your warranty company weren't making a profit off your business, would they keep doing business with you?

That profit belongs to whoever holds the risk. Right now, if you're using a third-party provider, they hold it. A reinsurance program routes those underwriting profits back to the contractor.

That's exactly what WarrantyRE is built to do. Since 1994, WarrantyRE has helped 400+ clients across the US establish and manage their own administrator-obligor reinsurance programs, handling legal formation, compliance, claims administration, and financial reporting so contractors capture the profit without managing the infrastructure themselves.

If you're ready to explore whether a reinsurance program fits your business, WarrantyRE offers a business analysis to evaluate profitability potential and guide program setup.

Frequently Asked Questions

Is reinsurance better than insurance?

They serve different purposes and are not substitutes. Contractor insurance transfers risk to protect against liability; warranty reinsurance is a profit structure the contractor owns. The better question is whether your warranty volume justifies building a reinsurance program alongside your required insurance policies.

What kind of insurance should my contractor have?

Core coverages for home service contractors include Commercial General Liability, Workers' Compensation (required in nearly all states), Commercial Auto for business vehicles, and Errors & Omissions for professional services. Specific requirements vary by state, trade, and contract obligations.

How much does a $1,000,000 liability insurance policy cost?

Cost varies significantly by trade, payroll, employees, state, and claims history. The Hartford reports small business GL averages around $810/year for a $1M policy, but trade-specific premiums — especially for roofing or electrical — run higher. Get trade-specific quotes from multiple carriers rather than relying on industry averages.

Can a contractor carry both warranty reinsurance and contractor insurance?

Yes, and most growing contractors should. They serve completely different purposes: contractor insurance protects against liability, while warranty reinsurance is a profit-building structure for the warranties you sell customers. Having both means you are covered against claims and keeping the underwriting profit — rather than sending it to a third-party provider.

What does warranty reinsurance cover that contractor insurance does not?

Warranty reinsurance covers the contractor's financial obligation to pay customer warranty claims on installed equipment or labor. Standard GL policies cover third-party bodily injury, property damage, and similar liability events — not product or labor warranty fulfillment. These are entirely separate obligations.

How do contractors set up a warranty reinsurance program?

The process involves forming a separate administrator-obligor reinsurance entity, meeting state regulatory requirements, establishing A-rated insurer backing, and setting up a claims administration structure. Specialists like WarrantyRE handle legal formation, compliance, and ongoing administration so contractors can focus on selling warranties rather than managing program infrastructure.