Introduction

Most roofing contractors offering warranties are already funding someone else's profit. Every labor warranty you sell generates premium income — and that money flows straight to third-party warranty companies while you absorb all the risk.

A roofing warranty reinsurance program changes that. You establish your own administrator-obligor reinsurance entity, underwritten by A-rated insurers, to back the warranties you sell to customers. This structure lets you capture 100% of premium income and control the claims process while staying fully compliant.

This article breaks down what a roofing warranty reinsurance program costs to set up and operate. You'll learn what drives costs up or down, what's included at different program levels, and how to evaluate whether the investment makes financial sense for your roofing business.

TL;DR

- Setup and admin costs vary based on warranty volume and program structure—no flat price applies

- Smaller contractors have lower absolute costs; high-volume contractors see greater profit capture

- Net cost is setup/admin expenses minus the underwriting profits you recapture from third parties

- Warranty premiums you already collect from customers fund most of the program

How Much Does a Roofing Warranty Reinsurance Program Cost?

There is no fixed price for a roofing warranty reinsurance program. Costs vary based on your business size, warranty sales volume, program structure, and the level of administrative support included.

The biggest mistake contractors make: assuming reinsurance is either unaffordable without running the numbers, or choosing a cheap bare-bones structure that lacks compliance backing and exposes the business to regulatory or claims risk. Both approaches cost more in the long run—either in lost profit opportunity or expensive compliance failures.

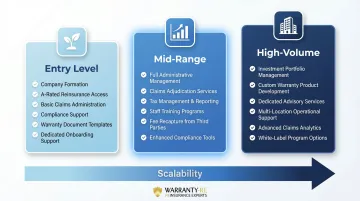

Program Cost at the Entry Level (Small to Growing Contractor)

Entry-level programs suit roofing contractors who are newer to structured warranties or selling a modest volume per year. You can test the model and build reserve capital without requiring high upfront volume. Services at this tier typically include:

- Basic company formation and regulatory filings

- Access to a reinsurance structure backed by A-rated insurers

- Initial compliance documentation and state licensing coordination

- Basic claims administration and customer service

- Monthly financial reporting

- Premium reserves funded from warranty sales revenue

The program is designed to be customer-funded from day one. You build warranty fees into your job pricing. On a $10,000 roof replacement with a 5- or 10-year labor warranty, that fee flows into your reinsurance account—not to an outside company. Your reserves grow over time, covering claims as they arise.

Program Cost at the Mid-Range Level (Established Contractor with Consistent Warranty Volume)

This tier fits established roofing contractors with consistent install volume who are currently paying a third-party warranty provider and want to recapture that profit margin. The administrative burden is fully managed on your behalf, while you retain 100% ownership of underwriting profits. Services include:

- Full company setup including legal entity formation

- Ongoing claims adjudication and resolution management

- Compliance filings and regulatory renewals

- Performance reporting and financial analysis

- Tax return management and accounting coordination

- Staff training and warranty sales support

Most contractors at this tier are already offering labor warranties to win jobs—they're simply redirecting warranty fees from third-party providers into their own reinsurance structure. Unused reserves accumulate as a financial asset on your balance sheet, and the program's administrative costs are offset by the premiums you were already spending elsewhere.

Program Cost at the High-Volume Level (Large or Multi-Location Contractor)

Designed for large or multi-location roofing contractors with significant recurring warranty sales, this tier delivers maximum profit capture through a fully managed program. Everything in the mid-range tier is included, plus:

- Advanced financial reporting and reserve investment management

- Customized warranty product development tailored to your market

- Dedicated account management and strategic advisory

- Tax planning coordination through a captive structure

- Multi-location program integration and consolidated reporting

Once accumulated reserves exceed 125% of unearned premiums, those funds can be invested more aggressively—generating additional investment returns on top of underwriting profits.

| Tier | Best For | Key Add-Ons |

|---|---|---|

| Entry Level | Contractors new to structured warranties | Company formation, A-rated reinsurance access, basic claims admin |

| Mid-Range | Established contractors recapturing third-party fees | Full admin, claims adjudication, tax management, staff training |

| High-Volume | Large or multi-location operations | Investment management, custom warranty products, dedicated advisory |

Pricing structure: Most programs are priced as a percentage of warranty premium volume, a monthly administrative fee plus reserve contribution, or a combination of both. Your final cost depends on warranty volume, claim history, and support level. Contact WarrantyRE directly for a pricing analysis tailored to your business size and goals.

Key Factors That Affect the Cost of a Roofing Warranty Reinsurance Program

The cost of a reinsurance program is shaped by business-specific, operational, and structural factors. Understanding these helps you evaluate quotes accurately and avoid underfunding or over-structuring your program.

Warranty Sales Volume

The number of warranties you sell per year directly determines both the size of the premium pool entering your reinsurance structure and the administrative load required to manage it.

How volume affects cost:

- Higher annual volume increases absolute program cost — but also increases your profit capture proportionally

- Lower volume means lower cost, though returns take longer to build

- Your total premium pool sets the pace for reserve accumulation and investment income potential

Industry context: The US roofing contractor market includes over 108,000 businesses generating $92.2 billion in annual revenue. The median roofing company generates between $500,000 and $4.9 million per year. Your warranty attachment rate (percentage of jobs including a labor warranty upsell) and average warranty fee determine your annual premium pool and, consequently, your program cost structure.

Program Structure: Administrator-Obligor vs. Other Models

The structure you choose has significant cost and control implications.

Administrator-Obligor Structure: Your contractor-owned company serves as the obligor (the entity responsible for fulfilling warranty obligations), with an administrator handling claims and compliance. This structure offers maximum profit control—you retain 100% of underwriting profits—and regulatory compliance backed by A-rated carriers. However, it involves more upfront setup and ongoing administrative coordination.

Cell Captive Model: You participate in a protected cell within a larger licensed insurance entity. Your assets and liabilities remain legally segregated from other participants. This structure requires lower capital contributions and reduced administrative costs, but offers less direct control than owning your obligor entity outright.

The administrator-obligor model costs more upfront. Roofing contractors who treat warranty income as a long-term revenue line — not a one-time add-on — consistently choose it for the profit control and compliance infrastructure it provides.

Level of Administrative Support

Programs offering full-service administration—including claims adjudication, compliance filings, bookkeeping, tax returns, and staff training—cost more in ongoing fees than bare-bones setups.

What full-service administration includes:

- Complete claims management from first customer call to final payout

- All regulatory compliance and state licensing renewals

- Monthly financial statements and performance analysis

- Annual tax return coordination with insurance tax specialists

- Ongoing staff training on warranty sales and processing

The cost-benefit reality: The fee gap between full-service and bare-bones programs narrows fast when you factor in the cost of errors. A single compliance failure or improperly denied claim can cost more to resolve than a full year of admin fees — making quality administration one of the better investments in the program.

Claims History and Reserve Requirements

Reinsurance programs require funded reserves to pay claims. The required reserve level depends on your historical claims rate, warranty types (labor-only vs. material + labor), and warranty term lengths.

What drives reserve requirements:

- Higher historical claims rates require more aggressive reserve funding

- Longer warranty terms (10 years vs. 5 years) increase reserve needs

- Complexity of coverage (full roof system vs. labor-only) affects reserve sizing

Industry data from extended service contract programs shows that approximately 36% of total warranty premium is typically allocated to loss reserves (pure premium for claims), with the remainder covering administrative costs and profit. Contractors with lower historical claim rates can accumulate surplus reserves faster, generating meaningful investment income on surplus reserves.

Company Formation and Jurisdiction Costs

Forming your reinsurance entity involves legal filing fees, state licensing considerations, and ongoing renewal costs that vary by business structure and jurisdiction.

One-time formation costs:

- Legal entity formation and corporate filings

- Initial regulatory compliance documentation

- State licensing application fees (where applicable)

- Trust agreement setup and carrier integration

Periodic renewal costs:

- Annual state license renewals (if applicable)

- Annual tax filings for the reinsurance entity

- Periodic compliance updates and reporting

These costs are separate from ongoing admin fees. Utah, Vermont, and South Carolina are common domiciles for captive structures, each with different fee schedules. For reference, Utah charges $7,450 for pure captive application and initial license, with $7,500 annual renewals. Administrator-obligor structures, however, often avoid these insurance-specific fees entirely — which is one more reason contractors doing volume choose that model.

Full Cost Breakdown: Setup vs. Ongoing Program Expenses

The total cost of a roofing warranty reinsurance program includes both one-time formation costs and ongoing operational expenses. Most costs can be funded by premium income the program generates.

Company Formation and Initial Setup

Setup is a one-time cost covering legal entity formation, regulatory filings, initial compliance documentation, and integration with an A-rated carrier as the backing insurer.

Specific line items include corporate formation fees, initial trust agreement setup, carrier underwriting integration, and first-year licensing where applicable. These vary by jurisdiction and program structure.

Ongoing Program Administration

This recurring cost (monthly or annual) covers claims adjudication, performance reporting, compliance renewals, bookkeeping, and tax return management.

In a full-service program, this is a disclosed, transparent fee — not a variable or hidden charge. It typically represents a percentage of premium volume or a fixed monthly rate based on program size. This fee covers:

- All claims processing and customer service

- Monthly financial statements and reserve tracking

- Regulatory compliance management and renewals

- Tax return coordination with insurance tax specialists

- Staff training and warranty program optimization

Claims Reserve Funding

This recurring cost is tied directly to warranty premium volume — a portion of each warranty premium sold is allocated to a reserve fund to cover future claims.

Unlike paying a third-party warranty company (where that money is gone), reserves in your reinsurance structure belong to your company and can be invested for additional return. Initially, reserves are invested in conservative government bonds earning short-term rates.

Once reserves exceed 125% of unearned premiums, excess funds may be invested more aggressively at your direction.

Staff Training and Onboarding

Training is a one-time (and periodic) cost covering initial onboarding of sales and administrative staff on how to present, sell, and process warranties through the reinsurance program. WarrantyRE includes this in the setup package.

Your team will learn to:

- Position labor warranties as value-adds during the sales process

- Integrate warranty fees into job pricing without friction

- Process warranty registrations accurately from day one

Periodic Renewals and Compliance Filings

Periodic costs include state licensing renewals (where applicable), annual tax filings for the reinsurance entity, and any required regulatory updates.

In a managed program, the administrator handles these — confirm whether they're included versus billed separately. Most full-service programs, including WarrantyRE's, bundle compliance management into the base admin fee.

What You Actually Get Back: Understanding the ROI of a Reinsurance Program

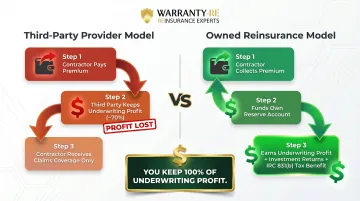

The core financial shift: when a roofing contractor pays a third-party warranty provider, underwriting profit (premiums minus claims) stays with that provider. When the contractor owns the reinsurance structure, that profit flows back to their own company.

Here's what that looks like in practice: if you pay $50,000 annually to a third-party warranty provider and your historical claim rate is 30% of premiums, roughly $35,000 in underwriting profit stays with that provider. Under a reinsurance program you own, that $35,000 accumulates in your company — minus administrative costs — year after year.

Additional financial benefits:

- Generates investment returns on accumulated reserves — starting with conservative government bonds, then more aggressively once reserves exceed regulatory thresholds

- Qualifies for IRC 831(b) tax election if annual premiums stay under $2.85 million, meaning underwriting income is effectively exempt from federal taxation

- Builds an accumulating asset on your balance sheet from unused reserves

There's also a structural alignment third-party providers can't offer. Unlike warranty companies that profit by minimizing claim payouts, administrator-only programs earn fees only when your reinsurance company performs well. When your company is profitable, the administrator keeps earning — so both sides are working toward the same outcome: fewer claims, stronger reserves, and more money staying in your business.

What Most Roofing Contractors Miss When Evaluating Program Cost

Focusing on Setup Cost in Isolation

Many contractors see initial formation and admin fees and compare them to the "zero cost" of staying with a third-party warranty provider. This ignores the premium profit being lost every year.

Consider the actual math: if you're paying $40,000 annually to a third-party warranty company and they're keeping $28,000 in underwriting profit (at a 30% claim rate), you're losing $28,000 per year. Over five years, that's $140,000 in foregone profit — easily dwarfing any realistic setup cost.

The setup fee isn't the real cost. Staying with a third-party provider is.

Underestimating the Value of Full-Service Administration

Contractors who minimize cost by choosing bare-bones or self-administered programs often encounter compliance failures, improper claims handling, or tax errors that cost far more to fix than the admin fee they saved.

Cutting corners on administration creates specific, costly risks:

- Improper 831(b) tax treatment can trigger IRS audits and penalties

- Inadequate reserve funding can leave you personally liable for claims

- Poor claims handling damages customer relationships you've worked years to build

- State licensing violations can shut down your program entirely

An administrator's carrier relationships and compliance infrastructure don't show up on a cost comparison spreadsheet — but their absence shows up fast when something goes wrong.

Ignoring the Long-Term Compounding Effect

Beyond avoiding liability, a well-administered program builds a financial asset that grows year over year. Reserves accumulate, earn investment returns, and compound — making the program worth more the longer it runs.

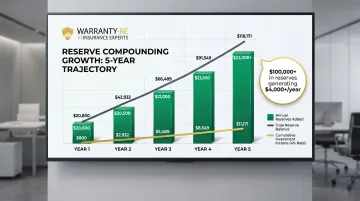

Here's how it works in practice: Year one, you accumulate $20,000 in unused reserves earning 4% in government bonds ($800 income). Year two, you add $22,000 more to the existing $20,800, now earning returns on $42,800. By year five, you've accumulated over $100,000 in reserves generating $4,000+ annually in investment income.

Contractors who delay starting miss years of compounding reserve growth. Industry data shows US captive insurers added $4.6 billion to year-end surplus over 2019-2024 while returning $2.0 billion in dividends—demonstrating the long-term wealth-building potential of owned reinsurance structures.

Frequently Asked Questions

How much does it cost to insure a roofing company?

General liability and workers compensation insurance (covering business operations, accidents, and employee injuries) costs roofing contractors an average of $267/month for GL and $254/month for workers comp. A warranty reinsurance program is different—it covers the cost of honoring labor warranties sold to customers. These serve different purposes and have different cost structures.

What is included in the setup cost of a roofing warranty reinsurance program?

Setup costs typically cover:

- Entity formation and regulatory filings

- Initial compliance documentation and trust agreement setup

- Integration with a backing A-rated insurer

- Staff training, onboarding support, and first-year compliance management

Full-service providers bundle all of these into a single setup package with no separate line items.

Can a small roofing contractor afford a reinsurance program?

Yes. Costs scale with warranty volume, so smaller contractors pay proportionally less. Since the program is largely funded by warranty premiums already collected from customers, you build warranty fees into job pricing and accumulate reserves over time—no high volume required to start.

How does a reinsurance program compare in cost to paying a third-party warranty provider?

Your net cost is lower because you recapture underwriting profits that previously stayed with the third party. If you're paying $30,000 annually to a warranty company and keeping only $9,000 in claims coverage (a 30% loss ratio), you're losing $21,000 per year. A reinsurance program can recover that gap—and turn it into profit.

What are the ongoing administrative costs of running a roofing warranty reinsurance program?

Recurring fees cover:

- Claims adjudication and compliance filings

- Bookkeeping, performance reporting, and tax return coordination

In a full-service program, all fees are disclosed upfront. Costs scale with warranty volume—either as a percentage of premiums or a fixed monthly rate based on program size.