Introduction

Picture this: an Ohio roofing contractor wraps up a solid install after last spring's hailstorm season. The crew did good work, the customer was happy, and the warranty paperwork got signed. Eight months later, a callback arrives — and the contractor's one-page workmanship warranty offers no real financial backing to cover it.

This scenario plays out regularly across Ohio. Most roofing contractors don't stress-test their warranty structure until a claim lands, and by then the document's limits have already decided the cost.

Warranty program quality varies widely among Ohio roofing contractors. Some run financially sound workmanship warranties backed by real infrastructure — structures that protect the business and build customer trust. Others issue coverage they can't realistically honor two or three years down the road, which creates liability exposure and reputational risk when claims come in.

This guide covers the two main warranty types Ohio roofing contractors issue, what's typically excluded, how Ohio's climate drives claim frequency, and what separates a workmanship warranty program built to last from one that's essentially a liability waiting to surface.

TLDR

- Roofing warranties come in two forms: manufacturer warranties (covering materials) and workmanship warranties (covering installation quality) — and you need both to be fully protected.

- Manufacturer warranties last 25–50 years, but coverage shifts to prorated after the initial full-coverage period ends.

- Workmanship warranties vary widely by contractor — from 1 year to lifetime.

- Ohio's freeze-thaw cycles, ice dams, and hailstorms make warranty terms more consequential than in milder states.

- Voiding your warranty is easier than you'd think: DIY repairs, neglected gutters, and unlicensed work are common causes.

The Two Types of Roofing Warranties Ohio Homeowners Receive

Every roofing project should generate two separate warranties covering two entirely different failure scenarios. Confusing them, or assuming one covers the other, is where most homeowners get caught.

Manufacturer Warranties

Manufacturer warranties protect against defects in the roofing materials themselves: blistering, granule loss, cracking, or premature deterioration. Standard coverage ranges from 25 years to "lifetime" depending on the product tier.

That word "lifetime" deserves a closer look. GAF, Owens Corning, and CertainTeed all define "lifetime" as the duration of the original homeowner's ownership, not the physical life of the building. If you sell, that clock resets under transfer rules.

Full coverage doesn't last the entire warranty period, either. After an initial non-prorated window (typically 10 years on standard products, up to 50 years on enhanced tiers like GAF's Golden Pledge or Owens Corning's Platinum Protection) coverage shifts to a prorated basis, and the homeowner absorbs a growing share of costs over time.

Standard manufacturer warranties also cover materials only, not the labor to install replacement materials. That distinction matters when a covered claim generates a $4,000 labor bill the warranty won't touch.

Workmanship Warranties

Workmanship warranties come from the roofing contractor, not the manufacturer. They cover installation errors: improper flashing, inadequate underlayment, incorrect shingle alignment, poor ventilation setup. These are problems the materials had nothing to do with.

The length gap between contractors is significant:

- Low end: 1–2 years (common among smaller operators)

- Mid range: 5–10 years

- High end: 25 years or lifetime

That gap reflects a contractor's financial confidence in their own work. Longer warranties mean the contractor is on the hook longer, which changes the incentive structure. A 1-year coverage window doesn't necessarily mean bad work, but it doesn't back the claim of quality with any financial commitment, either.

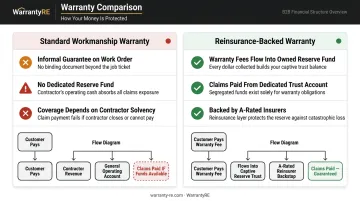

Some contractors formalize this commitment through contractor-owned reinsurance structures. WarrantyRE, for example, supports roofing contractors in establishing their own reinsurance companies, where warranty fees collected on every job flow into a legally owned reserve fund rather than going to a third-party provider.

Claims are paid from that pool, unused funds stay with the contractor, and the structure is backed by A-rated insurers. A 10-year workmanship promise backed by a funded reserve is categorically different from an informal guarantee typed on a work order.

What's Actually Covered — and What's Not

The fine print in roofing warranty documents tends to surface at the worst possible moment — usually when a claim is already in progress. For Ohio roofing contractors, knowing exactly where coverage stops is as important as knowing where it starts.

Coverage Homeowners Can Count On

Legitimate manufacturer warranty coverage includes:

- Manufacturing defects confirmed by inspection

- Materials replacement within the non-prorated window

- Labor coverage during that same window (for enhanced tiers through certified contractors)

Workmanship warranties typically cover installation-related leaks, flashing failures, and ventilation deficiencies traceable to the original installation — provided the contractor is still operating and honoring the warranty.

Common Warranty Exclusions in Ohio

Most manufacturer warranties explicitly exclude:

- Acts of nature: hail, tornadoes, flooding, winds above stated thresholds

- Normal wear and tear: age-related deterioration isn't a defect

- Ventilation problems: CertainTeed states that shingles installed on inadequately ventilated roof decks may see coverage reduced to 10 years with no SureStart protection

- Non-approved materials: GAF and Owens Corning both limit coverage to their own branded accessories

- Unauthorized repairs: damage resulting from non-certified work can limit or void claims

One exclusion catches Ohio homeowners off guard regularly: if a different contractor performs repairs after the original installation, it can compromise both the manufacturer and workmanship warranty. Contractor continuity matters more than most people realize.

Insurance vs. Warranty — Not the Same Thing

That exclusions list makes one thing clear: storm damage isn't a warranty issue — it's an insurance issue. The Ohio Department of Insurance is explicit: homeowner's insurance covers roof damage caused by events like windstorms or fire, but not damage from wear, maintenance neglect, or defects.

After a hailstorm or wind event, an Ohio homeowner may have a legitimate insurance claim — not a warranty claim. Pursuing the wrong channel delays resolution and can complicate both. Know which document applies to which problem before you pick up the phone.

Ohio's Climate and Why Warranty Terms Matter More Here

Ohio's weather creates specific, recurring stress on roofing systems that homeowners in milder states don't face at the same frequency.

Key weather risks for Ohio roofs:

- Freeze-thaw cycles stress flashing connections and force shingles to expand and contract repeatedly across a single winter

- Ice dams form when accumulated snow melts during the day and refreezes at the colder roof edge overnight — trapped water then backs up under shingles and into the structure (National Weather Service)

- Hailstorms are common in spring and summer; hail damage is typically treated as an insurance peril rather than a warranty defect

- High winds expose coverage gaps fast — GAF's base warranty covers up to 110 mph without special installation, while Owens Corning's Platinum Protection covers 130 mph for Duration-series shingles during the first 15 years

The non-prorated coverage window is especially valuable in Ohio's climate. A roof experiencing repeated thermal cycling may show accelerated wear compared to the same product in a southern state. If you're going to need a warranty, you're more likely to need it sooner — which is exactly when prorated coverage starts working against you.

That same urgency applies to how weather-related claims get categorized. Wind speed thresholds and hail minimums are written into manufacturer warranties, and Ohio homeowners should confirm what their specific product requires to qualify for a materials claim — versus what gets routed to their insurance carrier instead.

How to Evaluate a Workmanship Warranty Before Signing

The workmanship warranty is the most variable element on any contractor comparison. It's also the one area where a homeowner can most clearly see whether a contractor stands behind their work.

Questions to Ask Every Contractor

Before signing anything, get clear answers to these:

- How long is the workmanship warranty? Get the number in writing.

- What specific failures does it cover? Vague language is a red flag.

- Is it backed by the contractor directly or assigned to a third party? Third-party providers can exit the market.

- What happens to the warranty if your company closes? This question alone filters out a lot of weak guarantees.

- Is there a defined claims process? "Just call us" is not a claims process.

Contractor Longevity Risk

Many smaller Ohio contractors offer generous-sounding warranties without the financial infrastructure to honor them 7 or 10 years later. A 25-year workmanship warranty from a contractor with no documented financial backing is worth nothing if the company folds before a claim ever gets filed.

Contractors who have formalized their warranty obligations through a reinsurance structure hold warranty reserves in a trust account backed by A-rated insurers. When a claim arrives seven years after installation, that structure is what determines whether a homeowner actually gets paid — or gets ignored.

Certification and Enhanced Warranty Access

Manufacturer certification opens access to better warranty tiers. Only 2% of roofers in North America qualify as GAF Master Elite contractors, and contractors must hold that status to offer GAF's enhanced warranty programs. The top tiers across major manufacturers include:

- GAF Silver Pledge — 10-year workmanship coverage

- GAF Golden Pledge — 25–30-year workmanship with tear-off and disposal coverage

- Owens Corning Platinum Protection and CertainTeed SureStart PLUS — comparable tiers with similar credentialing requirements

If a contractor claims they can offer you a premium enhanced warranty, verify their certification status directly with the manufacturer.

Keeping Your Warranty Valid: Documentation and Maintenance

Documents to Retain After Installation

Homeowners should keep physical and digital copies of:

- Signed contract with warranty terms clearly stated

- Manufacturer warranty certificate with product details

- Proof of contractor certification status (GAF, Owens Corning, CertainTeed, etc.)

- Material receipts and product specifications

- Record of all post-installation inspections

These documents are what homeowners will need if a claim is ever disputed. Missing paperwork is one of the most common reasons valid claims get complicated.

Documentation alone isn't enough — ongoing maintenance is equally required.

Maintenance That Keeps Warranties Active

Most warranties include conditions homeowners must meet to keep coverage valid:

- Gutter maintenance: Clogged gutters cause water backup that can mimic leak damage — and provide grounds for claim denial

- Branch clearance: Overhanging limbs that cause physical damage fall outside standard warranty coverage

- Ventilation: Inadequate ventilation can reduce or eliminate CertainTeed coverage and is excluded by GAF

- Prompt repairs: Address minor damage quickly, and use certified contractors to do it

In Ohio, neglected maintenance is a leading cause of claim denial. Warranties cover defects and installation failures — not damage that routine upkeep would have prevented.

Warranty Transferability and Ohio Home Resale Value

Most manufacturer warranties allow a one-time transfer to a new homeowner, but the mechanics and deadlines vary by brand:

| Brand | Transfer Window | Fee |

|---|---|---|

| GAF | Within 1 year after property transfer | Not publicly specified |

| Owens Corning Platinum | Within 60 days of real estate transfer | $100 |

| CertainTeed SureStart PLUS | 15 years (3-Star) / 20 years (4-Star/5-Star) | Not publicly specified |

Workmanship warranties may or may not be transferable depending on the contractor's terms — confirm this in writing before listing the home.

Zillow reports that 15% of sellers repaired or replaced their roof before listing, and roof condition consistently ranks among buyers' top concerns during inspection. A transferable, documented warranty gives buyers confidence in a major system — smoothing negotiations and reducing last-minute price cuts. Keep all warranty documentation in your home file and be prepared to transfer it formally as part of the sale process.

Frequently Asked Questions

Is a roof warranty worth it?

Yes. Material defects and installation failures can generate repair costs well above any price difference between warrantied and non-warrantied installations — especially in Ohio's climate. Material warranties and workmanship warranties each cover failure modes the other doesn't — you need both.

How long do roofing companies warranty roofs?

Workmanship warranties typically range from 1 to 25+ years depending on the contractor, while manufacturer material warranties run from 25 years to "lifetime" (tied to original homeowner ownership). Longer workmanship warranties signal that a contractor stands behind their work — and has the financial structure to back it up.

What voids a roofing warranty in Ohio?

The most common triggers are DIY or unlicensed repairs, neglected gutters causing water backup, use of non-approved materials during subsequent work, and inadequate attic ventilation. Any of these can give a manufacturer or contractor grounds to deny a claim.

Can I transfer my roof warranty when I sell my home in Ohio?

Most manufacturer warranties allow one transfer to the new owner, but deadlines range from 60 days (Owens Corning) to 1 year (GAF). Workmanship warranty transferability varies by contractor. Confirm terms in writing before closing and gather all documentation to hand off with the home.

What is the difference between a manufacturer warranty and a workmanship warranty?

Manufacturer warranties cover defects in the roofing materials. Workmanship warranties cover problems caused by how those materials were installed. Both are necessary. Poor installation ruins good materials, and flawless installation can't salvage a defective product.

Does homeowner's insurance cover what my roofing warranty doesn't?

Homeowner's insurance covers sudden, accidental damage from covered perils like storms or hail. Warranties cover defects and installation failures. They're complementary, not interchangeable. After a hail event in Ohio, you're likely filing an insurance claim — not a warranty claim.