Introduction

Most contractors and dealers who set up their own warranty reinsurance company focus on the premium collection side — and rightfully so. But collecting premiums is only half the equation. The other half is controlling what you pay out.

That's where loss ratio comes in. It's the single number that tells you whether your reinsurance company is generating real underwriting profit or paying it all back in claims.

Get it right and your reinsurance structure does exactly what it was designed to do: keep money in your company instead of in a third-party provider's pocket. Let it drift and the profits you built this structure to capture start disappearing.

This guide is written for contractors and dealer principals who have established — or are seriously considering — a contractor-owned warranty reinsurance program. Whether you're an HVAC contractor, a roofer, a plumber, or an auto dealer, the mechanics are the same.

This guide covers:

- What loss ratio means and how to calculate it

- What a healthy range looks like for warranty programs

- What drives it in the wrong direction

- How to actively steer it back

TL;DR

- Loss ratio = claims paid ÷ premiums earned, expressed as a percentage — the lower the number, the more profit your reinsurance company retains

- For warranty and service contract programs, a loss ratio in the 40%–60% range is generally considered healthy, though your target depends on program maturity and volume

- High loss ratios erode the underwriting profits your reinsurance company was built to capture

- A ratio that's too low may signal overly restrictive claims handling

- Loss ratio is something you can actively manage through pricing discipline, claims adjudication, and consistent monitoring

What Is a Loss Ratio in Reinsurance?

Loss ratio is the percentage of your earned premiums that gets paid back out in claims and related costs. For every dollar of premium your reinsurance company takes in, it tells you how many cents went back out the door.

The formula:

Loss Ratio = (Incurred Losses + Loss Adjustment Expenses) ÷ Earned Premiums × 100

Each component matters:

- Incurred losses — actual warranty claims paid out, whether repair costs, replacement parts, or service labor

- Loss adjustment expenses (LAE) — the costs of processing and adjudicating claims, including adjuster fees and coverage-determination costs. Per NAIC SSAP 55, LAE breaks into Defense and Cost Containment (DCC) and Adjusting and Other (AO) categories

- Earned premiums — the portion of warranty premiums corresponding to coverage already provided. Premiums aren't fully "earned" when collected; they're recognized as income proportionally over the coverage period

How This Applies to a Contractor-Owned Structure

In traditional insurance, the carrier absorbs the claims risk and keeps the underwriting profit. In a contractor-owned reinsurance structure (the model WarrantyRE administers), you are the reinsurance company. Warranty fees flow into your reinsurance account. Claims come out of it.

The loss ratio directly measures how much of that premium pool you keep. That's the whole point of the structure: the profits your reinsurance company generates — the dollars remaining after claims — belong to you, not a third-party warranty provider.

Loss Ratio vs. Combined Ratio

Knowing your loss ratio is essential, but it only tells part of the story. Loss ratio doesn't capture the full profitability picture on its own. Combined ratio adds operating and administrative expenses:

Combined Ratio = Loss Ratio + Expense Ratio

According to AM Best, a combined ratio below 100% indicates underwriting profit; above 100% means the program is losing money overall even if loss ratio alone looks acceptable. For a reinsurance program owner, tracking loss ratio is the essential first step — but don't ignore the expense side.

What the Numbers Mean in Practice

| Loss Ratio | What It Signals |

|---|---|

| Below 60% | Strong underwriting profit retained |

| 60%–80% | Moderate — margin depends on expense load |

| 80%–100% | Thin profit or breakeven; monitor closely |

| Above 100% | Claims exceed premium income — unsustainable |

The goal is not to push loss ratio to zero. A suspiciously low ratio can indicate overly restrictive claims handling, which damages customer trust and ultimately hurts the business your reinsurance program is designed to protect.

What Is an Acceptable Loss Ratio for Warranty Reinsurance?

There's no single universal benchmark for warranty reinsurance — and any source claiming otherwise deserves skepticism. What we do have is useful industry context.

P&C Industry Context

The broader property and casualty insurance industry posted a net loss ratio of 71.2% in 2024, down from 76.3% in 2023, with a combined ratio of 96.9%. Professional reinsurance specifically ran a 69.4% net loss ratio in 2024. These figures reflect large, diversified books of business — not small-captive warranty programs — but they provide useful context for benchmarking.

For warranty and service contract programs, a loss ratio in the 40%–60% range is generally considered healthy. This range lets program owners retain meaningful underwriting profit while still honoring customer commitments. The right number depends on:

- Premium volume (smaller books have more volatility)

- Program maturity (newer programs often run higher early)

- Product mix (labor-only warranties behave differently than parts-and-labor contracts)

- Geographic risk (weather-exposed markets affect HVAC claim frequency)

What About the 80% Rule?

The 80% rule comes from the Affordable Care Act, which requires health insurers to spend at least 80% of premiums on medical care (85% for large group plans). This is a regulatory requirement for health insurance — it has no bearing on warranty or service contract reinsurance programs. Don't confuse a health insurance regulatory floor with a target for your warranty program.

Why Too Low Can Also Be a Problem

The concern isn't only with high loss ratios. A loss ratio trending toward 20% or 30% deserves equal scrutiny. If claims are being denied at an unusually high rate, customer satisfaction drops. Retention suffers. The brand reputation that justified your warranty program takes a hit. The goal is a sustainable, profitable range — not a zero-claims fantasy.

New Programs vs. Mature Programs

Newer programs typically run higher loss ratios in the early quarters. This is normal. Your initial book of warranty contracts takes time to season — loss emergence patterns stabilize over time as the covered equipment ages through its warranty period. Quarter-over-quarter trends matter more than any single data point.

What Drives Your Loss Ratio Up (and Down)?

Understanding what moves loss ratio gives you actual control over it. There are four primary drivers.

Claims Frequency and Severity

These are the two fundamental levers. The Casualty Actuarial Society defines frequency as claims per exposure and severity as losses per claim.

For warranty programs, frequency is shaped by:

- Equipment age and quality at the time of warranty sale

- Quality of installation or workmanship

- Geographic factors (extreme temperatures drive HVAC failures)

- Coverage term and mileage limits for automotive VSC programs

Severity is influenced by:

- Labor rates in your service area

- Parts availability and cost

- Deductible structure

- Technology changes that increase repair complexity

The practical implication: who you sell warranties to, and on what type of equipment, determines your claims profile before a single claim is filed.

Pricing and Underwriting Discipline

How your warranty products are priced determines how much premium your reinsurance company collects per contract. If warranty fees are set too low relative to actual risk — a common mistake when contractors price warranties to compete rather than to cover expected costs — your loss ratio will run high regardless of how well you manage claims.

Pricing must reflect realistic claims expectations for each product category. A labor warranty on a new HVAC system carries a different risk profile than one on an aging unit. Price them the same, and one of those is mispriced.

Claims Adjudication and Management

A contractor-owned structure has a real advantage here. You have direct visibility and influence over how claims are reviewed.

Structured, consistent claims adjudication — clear documentation requirements, defined approval criteria, and prompt resolution of legitimate claims — serves two purposes. It prevents overpayment on improper or inflated claims, and it maintains customer trust by handling valid claims efficiently.

WarrantyRE handles claims adjudication as part of its full-service administration, managing every claim from first call to final resolution. Program owners don't have to build a claims department from scratch or develop adjudication protocols independently. That structure comes ready on day one.

External and Catastrophic Factors

Unusually harsh winters or summers drive HVAC claims. A vehicle recall can spike claims across a dealer's warranty portfolio. These are real but temporary factors. The key is distinguishing a trend from an outlier. That distinction is only possible when you're tracking results period by period — and acting on what you see before a short-term spike becomes a long-term problem.

How to Monitor Your Reinsurance Loss Ratio

Monitoring loss ratio isn't passive. It requires consistent data, a regular cadence, and knowing what to look for.

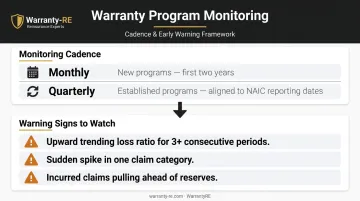

Monitoring Cadence

- Monthly — recommended for programs in their first two years

- Quarterly — minimum for established programs (aligns with NAIC statutory reporting dates: May 15, August 15, November 15)

For each period, pull three numbers: claims paid, IBNR reserves (incurred but not reported), and earned premiums. Calculate rolling loss ratios across three to four periods to see the trend, not just the snapshot.

What WarrantyRE's Performance Reports Provide

Contractors and dealers working with WarrantyRE receive performance reports and analysis as part of their program administration. Those reports include the key figures needed for loss ratio tracking, already organized and ready to act on. WarrantyRE also meets with program owners quarterly to review financial trends and the overall direction of their reinsurance company.

Warning Signs to Watch

Act when you see:

- Loss ratio trending upward for three or more consecutive periods — direction matters more than any single data point

- A sudden spike concentrated in one claim category, which points to a product, geography, or customer-type issue

- Incurred claims pulling ahead of reserves, which can signal underreserving and a costly correction down the road

Catching these early gives you room to adjust pricing, tighten product terms, or revisit claims procedures before profitability is seriously affected.

Strategies to Improve Your Loss Ratio

When loss ratio runs above a healthy range, there are three places to apply pressure — and one approach to avoid.

Review Product Terms and Pricing Alignment

Start by asking whether your warranty product terms accurately reflect the risk you're actually underwriting. Coverage that's too broad for the premium collected will always generate a high loss ratio.

Adjustments to consider:

- Deductible levels (higher deductibles reduce claim frequency)

- Coverage exclusions (pre-existing conditions, lack of maintenance)

- Contract pricing aligned to equipment age, type, or service category

Make these changes thoughtfully. Reactive coverage reductions that catch customers off guard tend to damage trust and drive cancellations — which compounds your profitability problem rather than solving it.

Strengthen Claims Adjudication

Consistent, documented claims review is one of the most direct loss ratio management tools available. This means:

- Clear documentation requirements for all submitted claims

- Defined approval criteria applied consistently

- Prompt resolution to avoid disputes and rework

- Regular review of denied-claim patterns to catch procedural gaps

For WarrantyRE clients, this process is built into the administration — claims adjudication is a core part of what the program delivers, not an afterthought.

Invest in Quality at the Point of Sale

The risk profile of the customer and equipment being covered has a direct impact on your loss ratio. Warranties sold on well-maintained systems, newer equipment, or vehicles with solid service histories will generate fewer claims than warranties sold indiscriminately.

Managing that risk starts upstream — before the contract is signed. The most effective tools at this stage include:

- Customer education on what the warranty covers and requires

- Quality installation standards that reduce early failure rates

- Disciplined warranty sales practices tied to equipment condition

Frequently Asked Questions

What is an acceptable loss ratio in insurance?

It depends on the line. P&C lines typically run 40%–70% per NAIC data. For warranty and service contract reinsurance programs, 40%–60% is a healthy target — though program maturity, volume, and product mix all affect what's realistic for your specific program.

What is the 80% rule in insurance?

The 80% rule comes from the Affordable Care Act and requires health insurers to spend at least 80% of premiums on medical care (85% for large group markets). This rule applies exclusively to health insurance and has no regulatory bearing on warranty or service contract reinsurance programs.

What is the difference between loss ratio and combined ratio?

Loss ratio measures only claims costs relative to earned premiums. Combined ratio adds operating and administrative expenses to give a complete picture of total underwriting profitability. A combined ratio below 100% signals that the program is generating overall underwriting profit.

How does a high loss ratio affect my reinsurance company's profits?

A reinsurance company profits from the dollars remaining after claims. A high loss ratio directly cuts into — or eliminates — those profits, and sustained elevation strains program reserves and threatens long-term viability.

How often should I review my reinsurance program's loss ratio?

At minimum, quarterly. For programs in their first year or two, monthly tracking is better. Regular monitoring lets you catch trends early and adjust pricing, claims handling, or product terms before a small issue grows into a larger one.

Can I improve my loss ratio without raising warranty prices?

Yes — pricing is one lever among several. Better claims adjudication, tighter coverage terms, quality installation practices, and more selective warranty sales can all move the ratio without touching what customers pay.